We still prefer bonds despite the frustratingly flat YTD performance (aggregate bond ETF), and despite our longer-term skepticism. The flow of soft economic data continues to make a recession a high probability. Recent revisions to labor data and the banking stress have raised confidence in the cautious view. In our 2023 Outlook, we highlighted a July 2023 recession onset based on 2yr10yr yield curve inversion. Using the 3month to 10yr yield curve inversion shows we are still in the early going at month seven.

Furthermore, megacap stock valuations and their concentration in indices make for poor risk rewards. We do not believe “this time is different” when it comes to forward indicators of recession translating into actual recession and downside for stocks. AI, which should have positive impacts over the long term (beyond just chipmakers), is unlikely to offset broad economic weakness in the short term. The current megacap price action reminds us of the dotcom boom in 1999 or Chinese stocks like Chalco in 2007. As Dispatch #1 explained, extending the debt ceiling should lead to reduced liquidity, and we will not be chasing any debt-ceiling relief rally. To stress test our views we evaluate bullish arguments for continued risk-asset strength.

To our American readers, enjoy Memorial Day and the unofficial start of summer!

Dispatch #5 of 2023 completed on May 26th evaluates the following subjects.

- Why we continue to prefer bonds

- Update on yield curve inversion and recession timing

- Leading recession indicator update

- What bullish data have we seen

Why we still prefer bonds

It’s simple enough to say that we believe a recession is coming. The banking stress of the past few months has increased the probability of a deeper recession as bank credit, the lifeblood of economic activity, contracts faster than we thought it would in January. Small business is the lifeblood of the economy, and these companies are facing tighter credit conditions as this WSJ story details. The large YTD performance divergence between megacap dominated NASDAQ 100 index and the small cap Russell 2000 index could be the stock marketing sniffing out a slowing. You just wouldn’t know it by watching large cap indices.

YTD 2023 performance divergence of NASDAQ 100 ETF vs. small cap Russell 2000 ETF

For bonds, we find a roughly 5% yield at the short end to be attractive compared to the potential returns from high-value stocks that are not discounting an economic slowdown. It also provides optionality to invest into riskier assets as opportunity emerges. For stocks, the Wall Street herd is projecting positive earnings growth in 2023 and punchy 12% growth in 2024. These are not projections based on an economic contract. During a recession earnings fall substantially. The RockDen 2023 Outlook showed the range of earnings declines in recessionary years. There has not been a single recession where earnings did not decrease.

Bonds have risks too

To be clear, there are risks to owning longer-term bonds. There’s a notable spread between the current Fed Funds Rate of 5.25% and, for example, the ~3.8% 10yr yield. If inflation were to remain higher, there could be considerable pain if the 10yr yield moves closer to Fed Funds. This risk has partially played out in the current quarter as bonds have sold off. On the flip side, a sharp recession will require the Fed to cut rates, in which case, locking in a ~3.8% yield could prove attractive. In this latter scenario, long-term bonds will rally, which is the primary reason to hold longer term bonds. To mitigate some of the risks we have a barbell exposure of short-term and intermediate bonds. If rates rise following a debt ceiling extension, we may look to increase duration.

To be clear, we are cautious on bonds over the long term as we see risks of financial repression with the heavily indebted US government and the economy unable to handle today’s high rates. With this view, we are not wedded to our current preference for bonds. We see us trading out of bonds when the risk reward improves for riskier assets like equities, commodities or private assets.

Yield Curve Inversion and Recession Timing

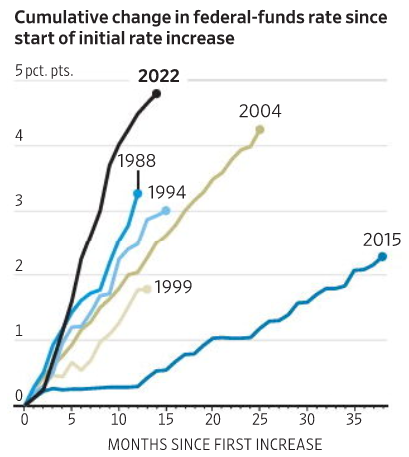

The Fed has hiked rates at the fastest pace in recent decades.

Source: WSJ

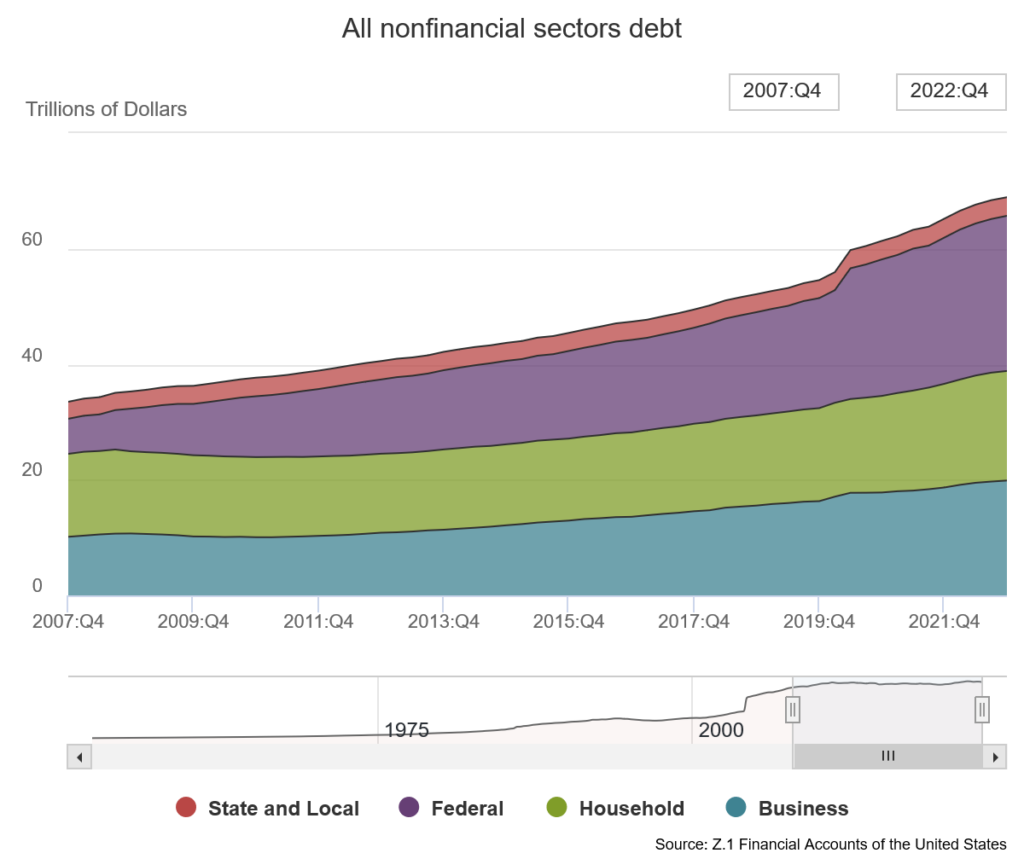

The higher rates in a highly indebted economy should lead to slower activity, which does take time. The US now has ~ 300% total debt to GDP. Many are familiar with the high government debt to GDP, but few think about the additional consumer and corporate debt that must be repaid by the same GDP. This chart from the Federal Reserve excludes the Fed’s $5.6bn Treasury holdings in 4Q22, which we’ve added back to get the 300% number.

Source: Federal Reserve

The inversion of the yield curve anticipates the probability of an economic slowdown as debt service soaks up more cashflow and higher return expectations slow investments. Section 4 looks at why this time might be different and why higher rates may not slow activity

Timing the recession

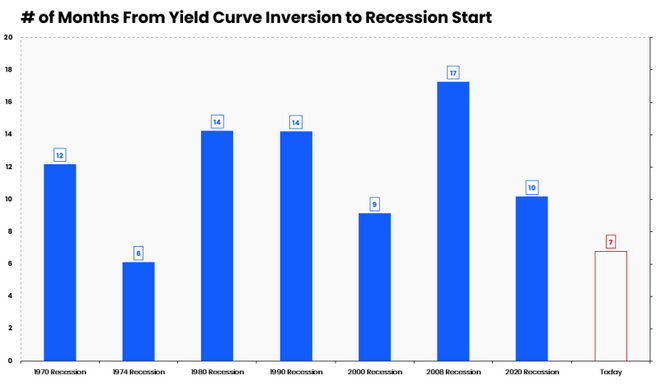

In our 2023 Market Outlook, we highlighted work by DoubleLine’s Jeffrey Gundlach that suggested an average of 66 weeks from 2yr10yr curve inversion to recession onset. The 2s10s curve inverted in March 2022, so he pointed to a July 2023 recession onset based on historical trends.

We augment DoubleLine’s view with work by EPB Macro & Cheng Wei Chin, who looks at the 3month20year curve inversion to guide recession timing. There’s a wide variation in timing from curve inversion and start of recession, as the chart below shows.

Source: EPB Macro

We are at month 7 since inversion, which is at the lower end of the historical range. Given the unprecedented monetary and fiscal stimulus during Covid, a longer onset could be an argument. This tailwind is balanced by the steeper rate hikes and greater leverage.

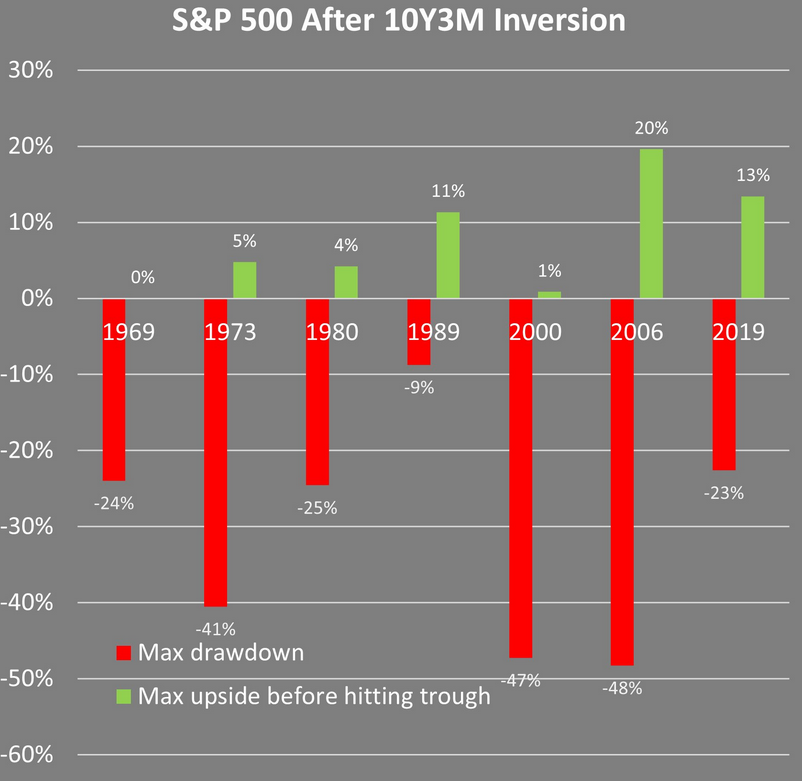

Stocks have often rallied post inversion, but have fallen subsequently.

Source: Cheng Wei Chin

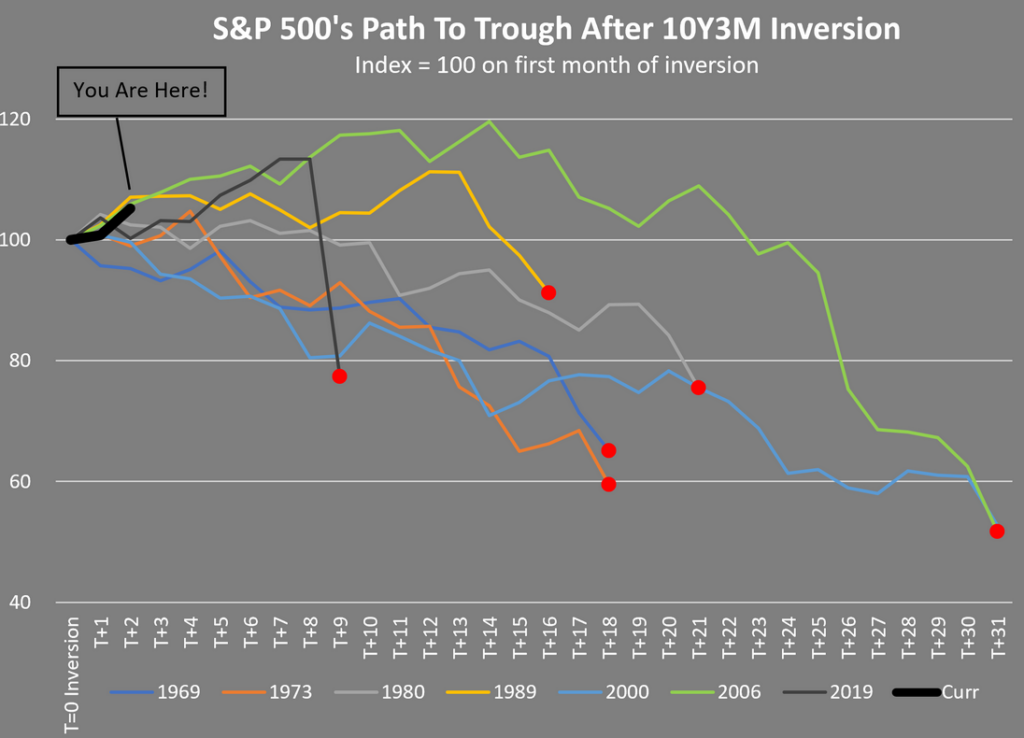

Here’s the same data shown differently. S&P 500 indexed to zero at first curve inversion. What jumps out is that we are very early in the journey post curve inversion.

Source: Cheng Wei Chin

Recession leading indicator update

Employment data revisions are decidedly negative

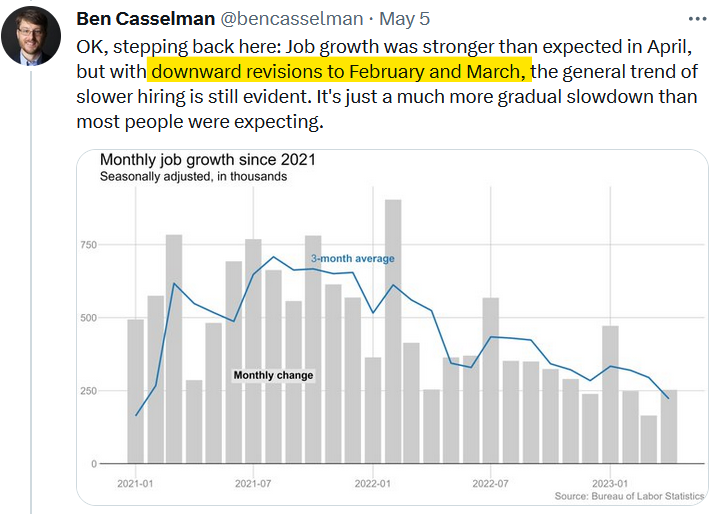

The Bureau of Labor Statistics (BLS) revised initial data for up to 12 months. The market typically reacts to the monthly data, which can then be revised materially in the months following. We are seeing labor market revision paint a worsening picture, even as incoming headline monthly data remain firm, often due to the BLS’ seasonal adjustments.

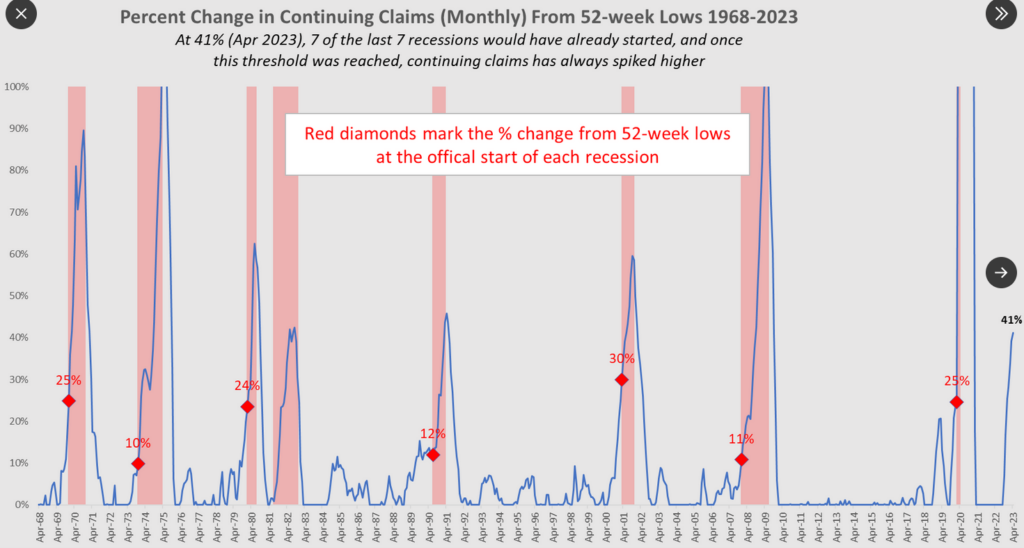

The rise of continuing unemployment claims is at a level that has previously signaled a recession. This captures the revised data, whereas the casual observer only hear the monthly headline figure, which is initially reported strong but subsequently revised lower.

Source: Cheng Wei Chin

An example of revisions, captured in the above data but is typically only noticed by wonks, is in the details in the April employment report. In the report, the BLS revised February and March employment figures lower, which were initially seen as strong.

Just this week the BLS released the 4Q22 Quarterly Census of Employment and Wages report that showed average weekly wages fell 2.3% YoY. Hardly anyone has picked up on this report that goes against the 4.2% wage gain reported for 2022 based on the monthly jobs report. Bloomberg wrote about this divergence, which also led to $135bn cut in 4Q GDP. It is tough to trust the data quality in BLS reports given incremental adjustments and lower response rates post Covid.

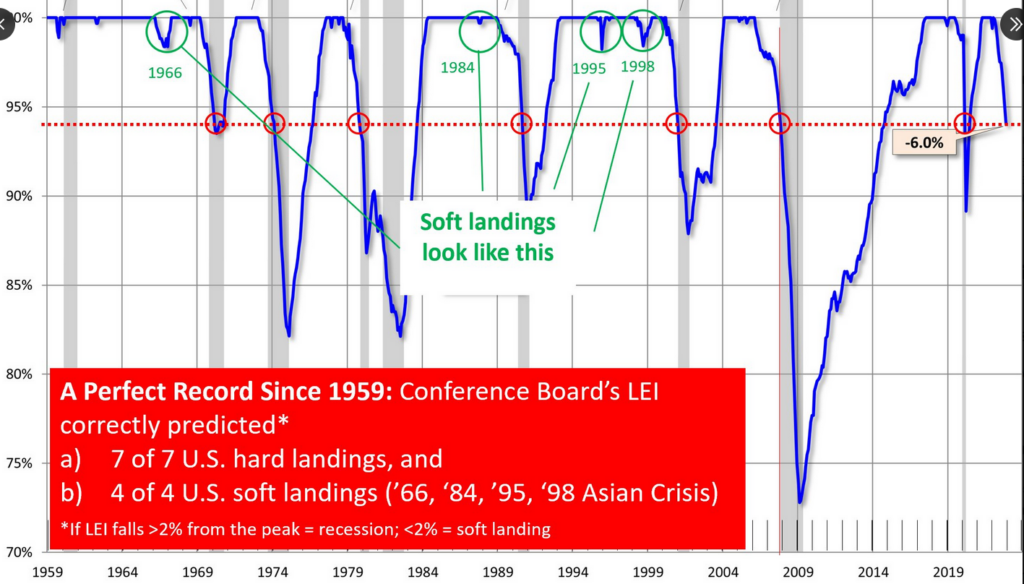

Leading Indicators (LEI)are well beyond soft landing territory

At the current LEI rate of change, a recession has followed 100% of the time since the 1950s. Unless you believe this time is different, there’s no soft landing on the horizon.

Source: Cheng Wei Chin

What positive signs or arguments have we seen

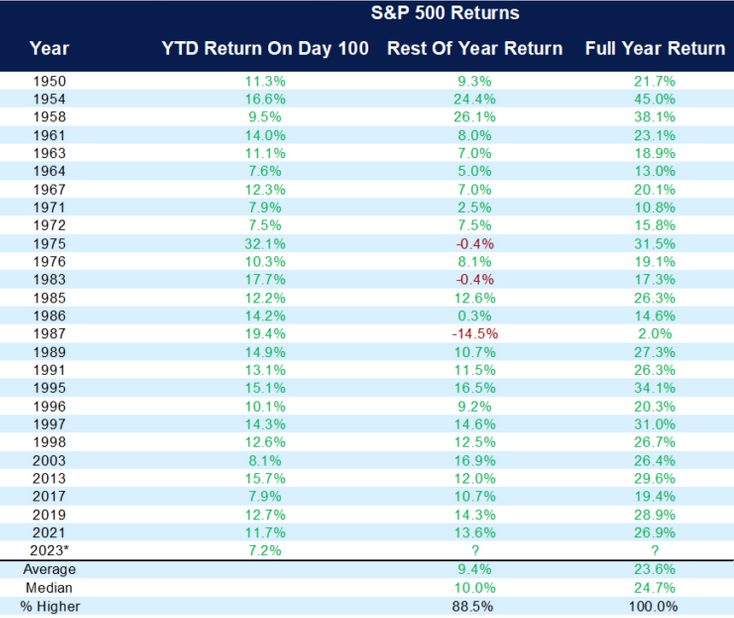

Positive technical arguments abound. Carson Group’s Ryan Detrick has been bullish and right this year. His latest thoughts highlight positive estimate revisions and strong technical support. Another frequent Carson Group bullish comment goes along the lines of “if the market is up on day 100 (they’ve used January as well), then it has often had even better returns for the full year”. The table below is from the Carson Group story.

Source: Carson Group

All the green on this chart makes for a rather striking image. The problem with this particular theory is that markets trend directionally so we get very similar statistical conclusions whether we look at gains in January, February or first 100 days followed by full year gains. The question for 2023 is if this trending market can be sustained in the face of increasing evidence of a slowing economy. We fall squarely into the “no” camp.

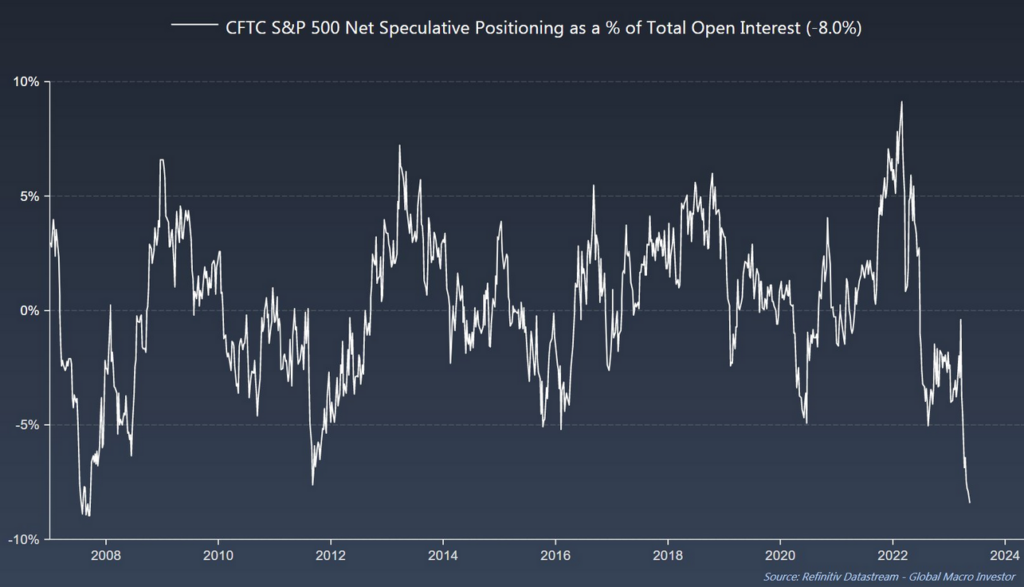

Another popular bullish technical argument is the record short position in S&P 500 futures by speculators, usually interpreted as hedge funds. The problem with this interpretation is that as banks have shrunk their market-making operations, more hedge funds have stepped into market-making activity. This activity is misreported as “speculative”, even when the short position is offsets by long positions elsewhere.

Source: Raoul Pal

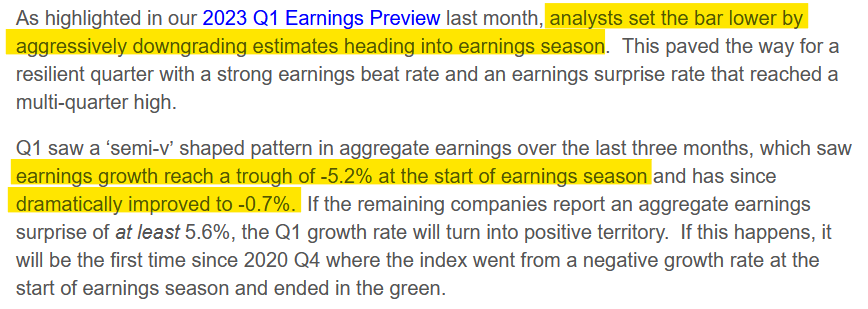

1Q earnings have come in better

Switching to fundamental factors. 1Q23 earnings have indeed come in better, beating earnings that were cut ahead of results. Financial data company Factset says 78% of S&P 500 companies have reported positive earnings surprises and 76% have reported positive revenue surprises. However, companies are beating lowered expectations. Comments from Refinitiv’s 1Q 1Q23 Earnings Review are shown below with our highlights. At the same time, more companies (58) have issued negative 2Q guidance compared to positive (41) guidance, according to Factset.

Source: Refinitiv

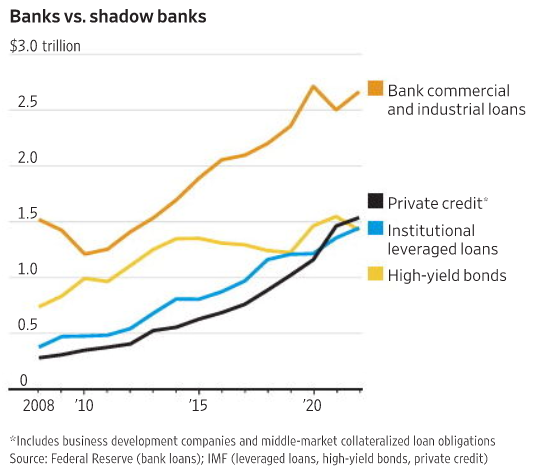

Is the economy less rate-sensitive now despite higher debt levels?

On the macro front, one argument claims that the economy is less sensitive to bank credit tightening because of the growth in private credit. “Private credit” and “leveraged loans” in the chart below are new areas of lending outside of banks, often referred to as shadow banks. Private credit, though, is floating rate, and we are already seeing a pickup in defaults in the space.

The overall private credit sector is now 2x larger than the high yield bond market, and it has grown at a rapid pace since the global financial crisis. It’s an industry that has not seen an economic cycle to stress test underwriting standards, covenants, and use of leverage in some funds. We have avoided the attractive headline yields available in private funds at this very late stage in the economic cycle.

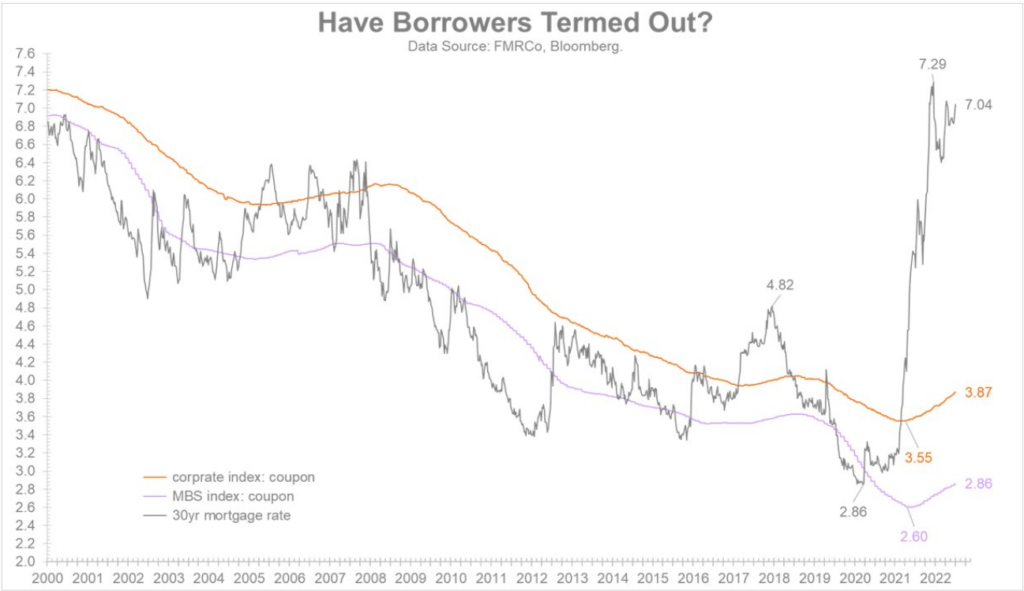

Another argument goes that companies and consumers are less sensitive to rate hikes because they have already locked in (aka, termed out) low fixed rates. We know this is very true for consumers where most of the debt is fixed-rate mortgage borrowing. Only larger companies with access to bond markets can term out debt by issuing fixed-rate bonds, including junk bonds.

Source: Jurrien Timmer

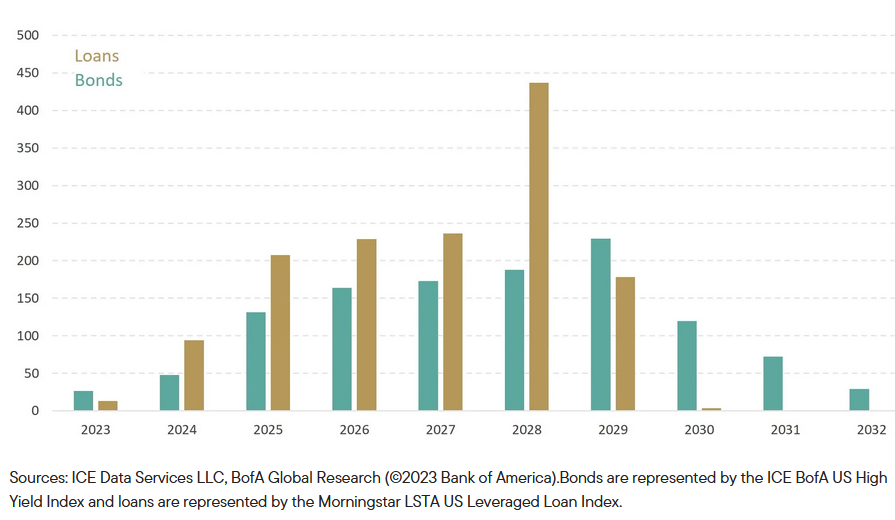

The risks for even fixed rate issuers will arise as more bonds start maturing from 2025 onwards. These will need to be refinanced at higher rates (if we are right, not as high as rates today). The maturity chart below does not include middle market private credit, which is as large as junk bonds.

Source: Franklin Templeton

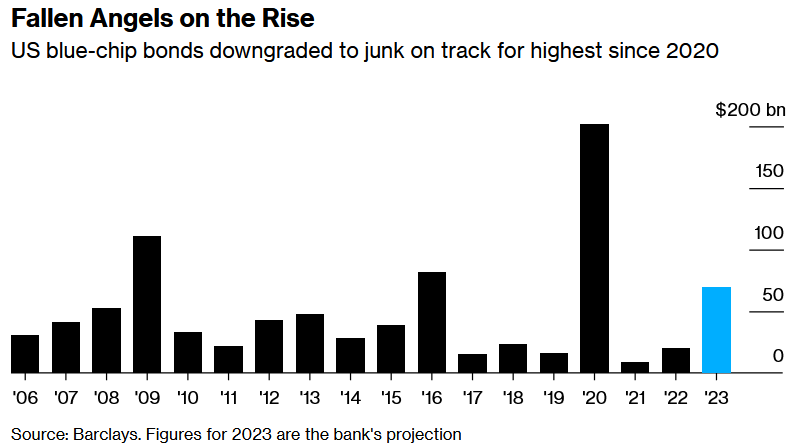

Ratings downgrades are picking up

It’s worth noting that there’s already an acceleration of downgrades of investment grade bonds to junk. The blue 2023 bar is a FY estimate based on a 1Q downgrades of $11.8bn.

Source: Bloomberg

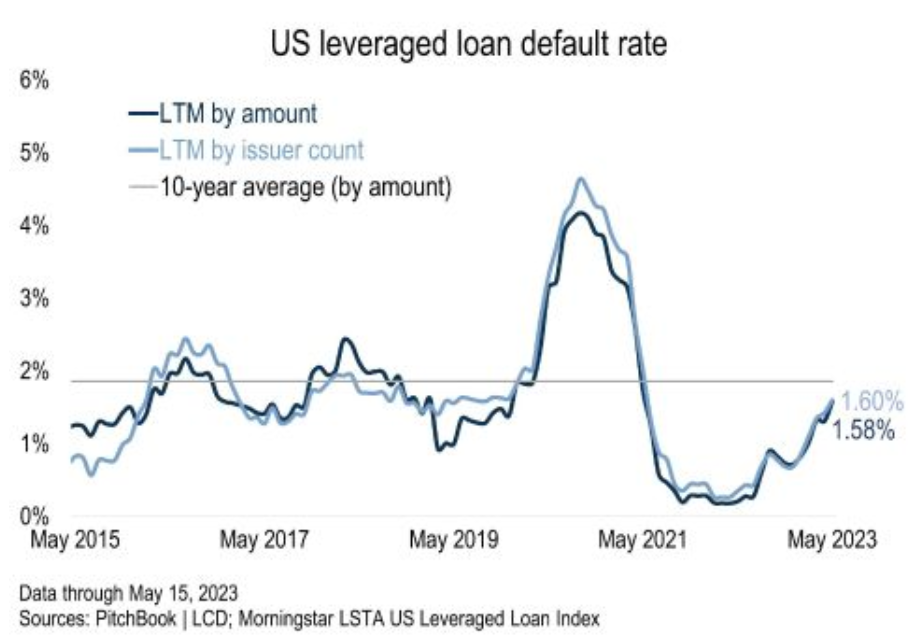

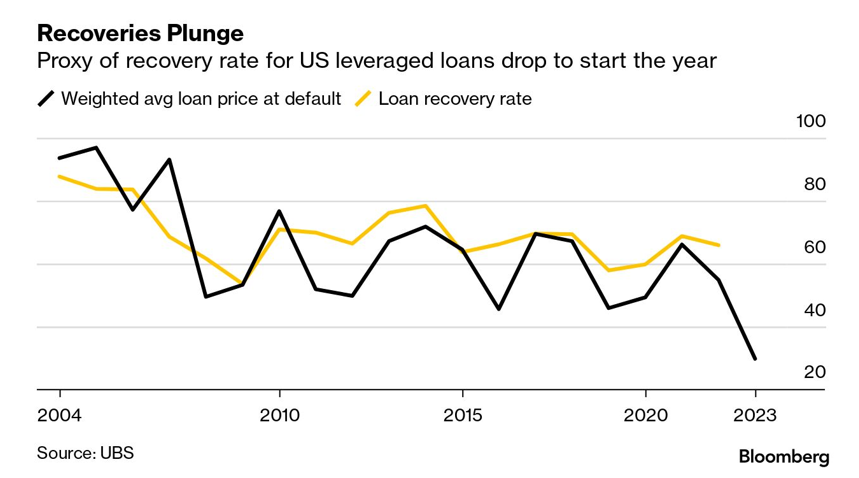

And, a pick up in leverage loan defaults, although the absolute levels remain below 10-year average.

Source: PitchBook

The recovery trend of defaulted loans is not encouraging, but that should not be a surprise given weak covenants and rising exposure to technology companies that have fewer hard assets to liquidate.

Source: Bloomberg

Enjoy the long weekend in memory of our veterans.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |