The current debt ceiling morass should add liquidity into the economy and markets in the short term. The added liquidity, along with Fed pivot enthusiasm, is clearly supporting higher asset prices currently. This is ironic as not resolving the debt ceiling in a timely manner increases market risk, and it highlights the unsustainable debt picture of the United States. Technical momentum, positioning and lowered earnings expectations have also supported markets. However, our highest probability view remains that equity markets are incorrectly pricing a soft landing, as articulated our 2023 outlook. Recent earnings downgrades and the current rally has raised valuations approximately 20% to an unattractive 22x trailing PE multiple. Adding earnings risk to this elevated starting position, plus shrinking liquidity post debt ceiling extension, could make for a volatile cocktail in the coming months. We expect Congress to extend the debt ceiling ahead of a default, but see a contentious and to-the-brink path.

Dispatch #1 of 2023 completed on February 2nd evaluates the following topics:

- Debt ceiling machinations

- Improving market internals

- Bank of Japan governor change is a risk

Debt ceiling & liquidity machinations

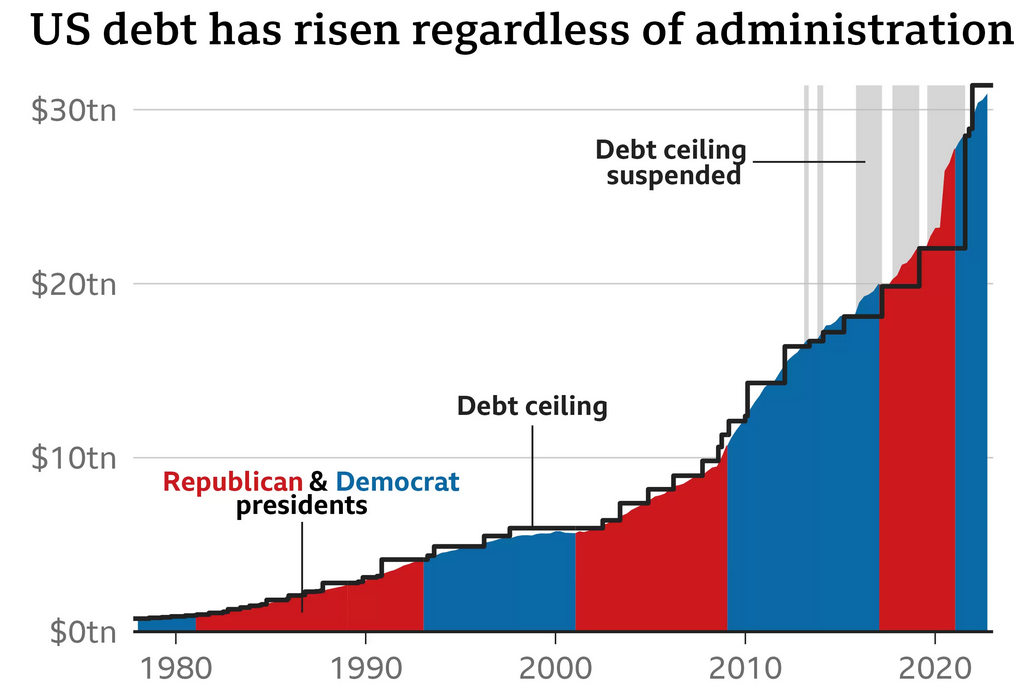

The US Congress sets the amount of debt the country can issue. We reached the currently approved US$31.38 trillion debt limit in mid-January. The Treasury Department can only issue new debt instruments to refinance existing debt. Since the US spends hundreds of billions of US$ more than it collects in taxes, we will need to raise the debt ceiling by late summer to not default on the outstanding debt, pay Social Security, Medicare and salaries. The Bipartisan Policy Center shows the debt ceiling through the years.

Here’s how the ceiling has progressed, with a large jump during Covid. Debt to GDP is now over 120%, one of the highest historical levels.

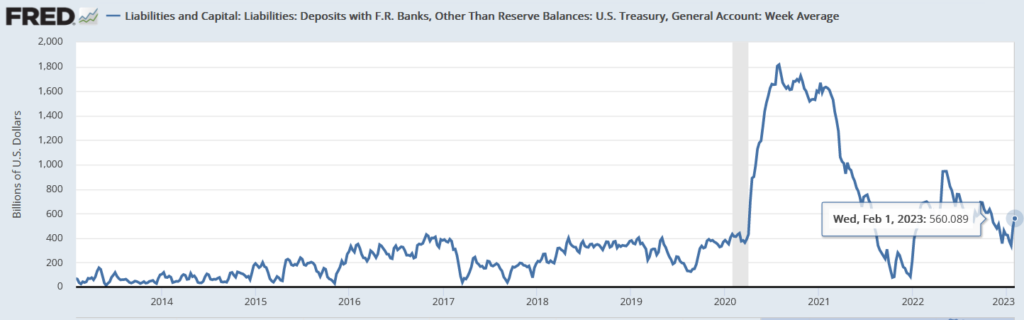

While Congress bickers over the debt ceiling, the US can use its checking account (called the Treasury General Account – TGA) for expenses. The Treasury also has also started implementing “extraordinary measures”, but our discussion will focus on the TGA alone.

There’s $560bn available in the TGA

The government spending money puts US$s into the economy, while there’s no new bond issuances sucking US$ out of the system. This mechanism should temporarily offset the $60bn a month of liquidity being withdrawn by Fed QT (quantitative tightening). In the puzzling world of finance and politics, the dangerous journey towards the cliff’s edge of the country running out of cash and defaulting provides a liquidity boost to markets. Go figure!

Improving market internals and bearish sentiment

(This section was originally written in mid-January, 2023, and the market moves are playing out. Possibly played out)

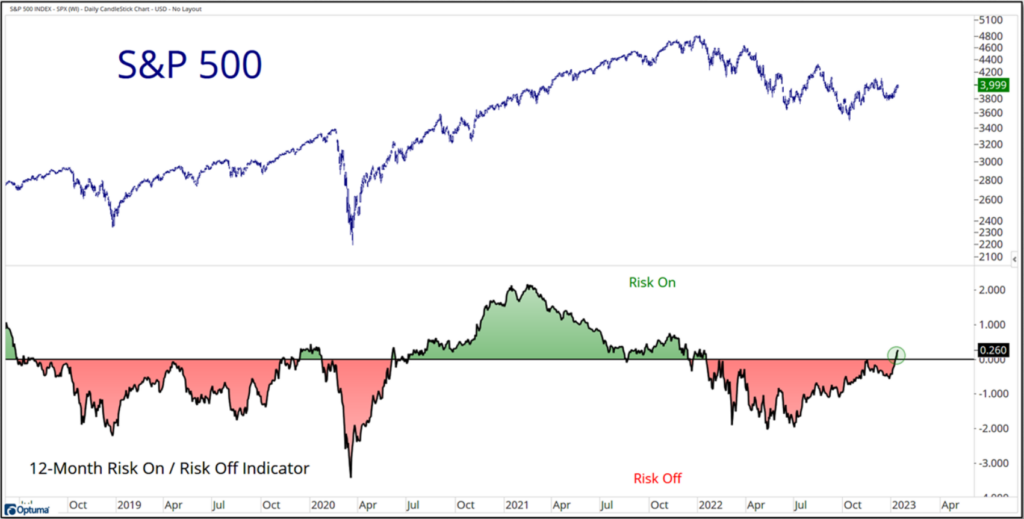

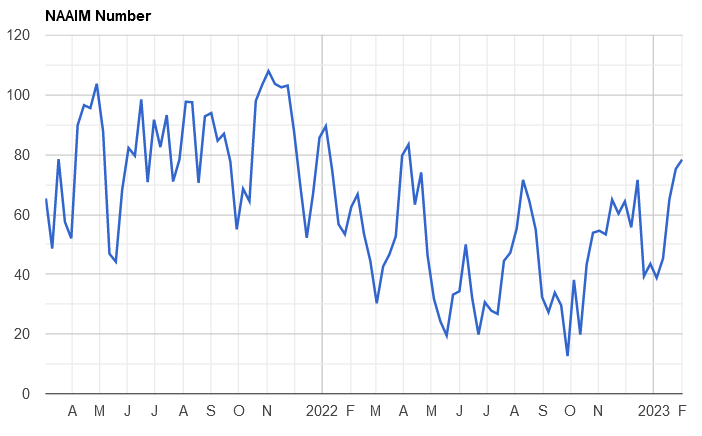

Even as we believe that valuations are not attractivevand earnings could fall, we are aware of improving signals elsewhere, particularly on the technical front. The chart below is a good example of the technical analysis that has showed a strong breakout of stocks.

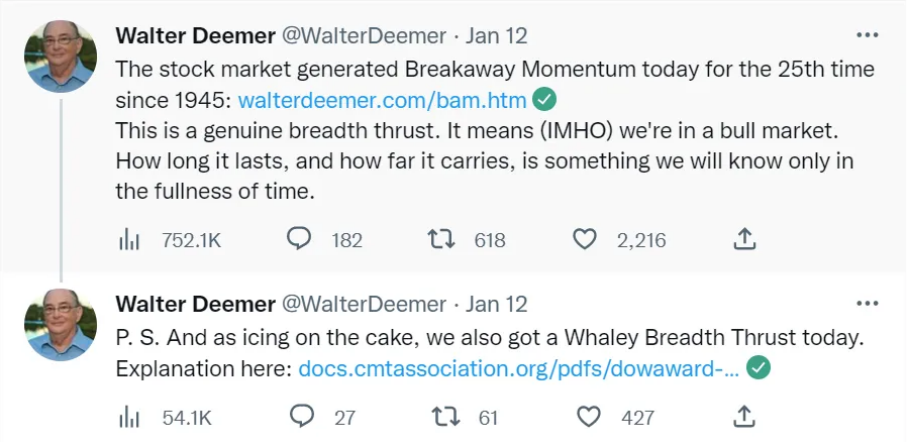

Technical analysis guru Walter Deemer had this observation.

Source: Walter Deemer

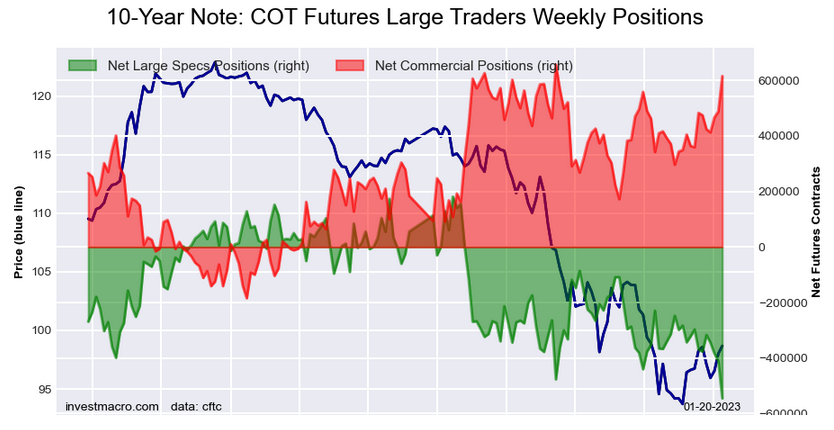

In the bond market, shorts had increased (chart from Jan 22nd), which may explain the explosive move lower in bonds yields (Bond prices up = yields down this week).

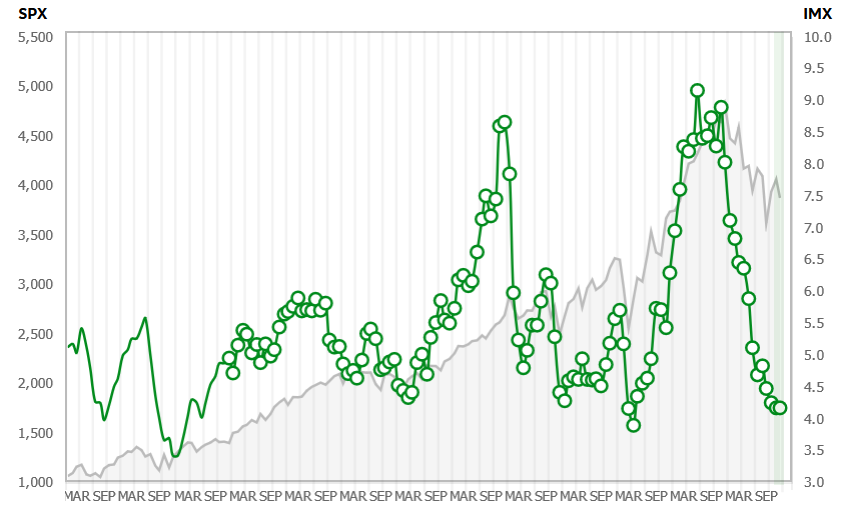

Some retail sentiment indicators are also has lows. Here’s TD Ameritrade’s Investor Movement Index

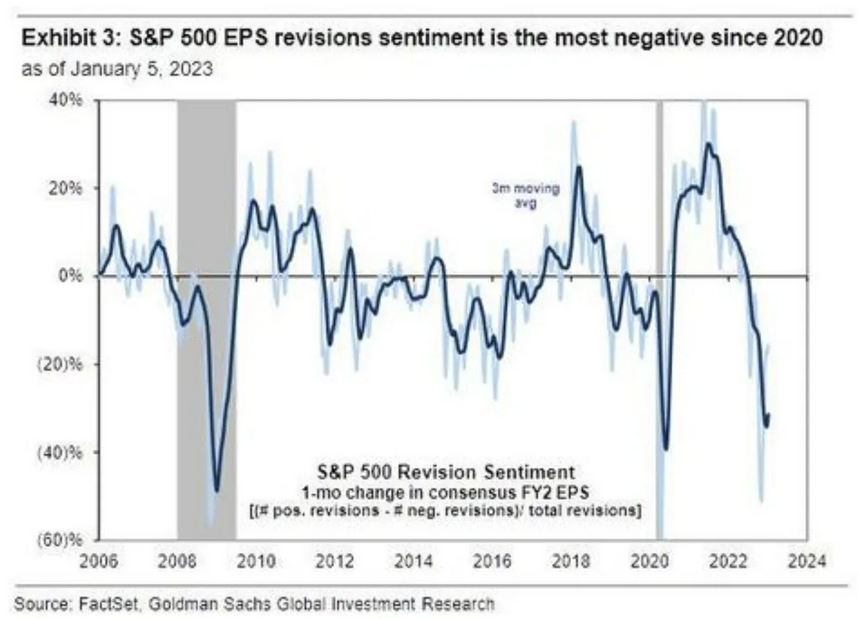

Short-term earnings revisions have turned lower as this Goldman chart shows.

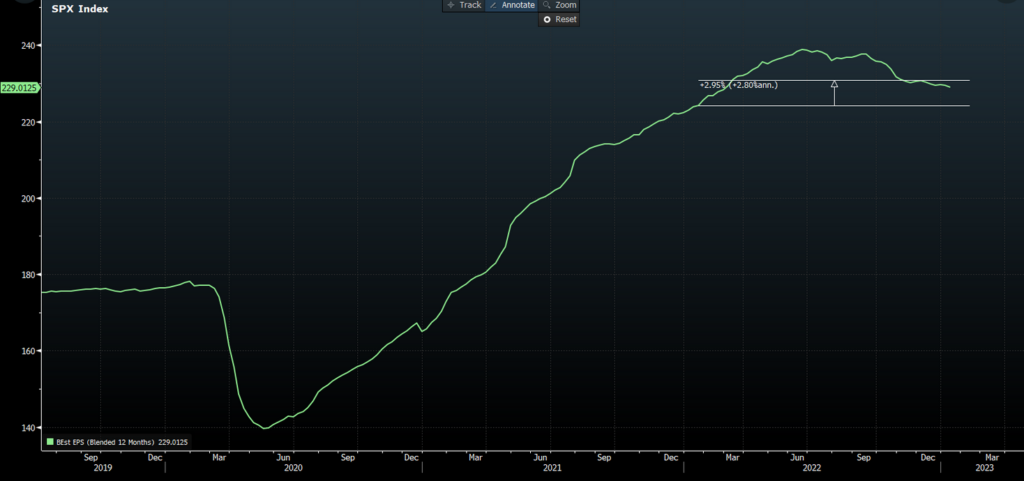

In the short term, lowered estimates could well lead to positive reactions to the December quarter results reports. However, the short-term metric of 1-month change does not change that earnings are elevated from a longer-term perspective, as shown below

Institutional investors are no longer overly bearish

Furthermore, mutual fund managers have quickly raised their exposure from cautious/bearish October levels.

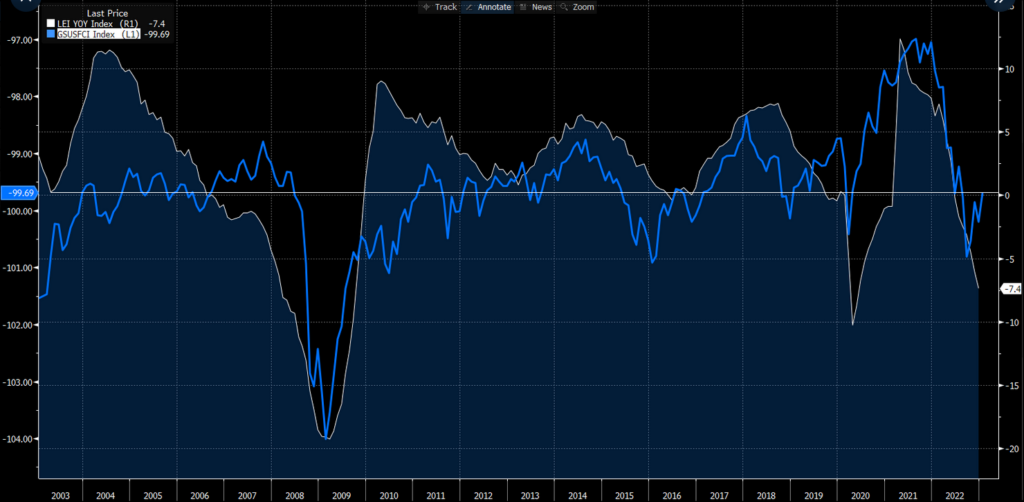

Financial conditions, the main transmission mechanism for Fed policy, have loosened considerably, even as Fed Funds Rate (one input into financial conditions) has risen. Markets are clearly ignoring the risks that the Fed may see the need to raise rates further if, for example, property prices resume upward momentum as mortgage rates fall alongside Treasury yields.

Leading indicators drop but Goldman Sachs financial conditions ease (inverted in blue)

Yes, the drop in inflation, without a corresponding jobs weakness, has raised the probability of a soft landing. Surprisingly, it is robust construction job demand that is supporting the employment market. These tweet thread by economists Steve Miran and Dom White dive into the puzzling strength in construction jobs despite slowing home sales and rising housing inventory. It’s an areas to watch closely.

Despite the improving outlook, our highest probability view remains of a US slowdown from mid-year, which leads to earnings downgrades that pressure valuations/price.

Bank of Japan (BoJ) leadership change and yield curve control (YCC)

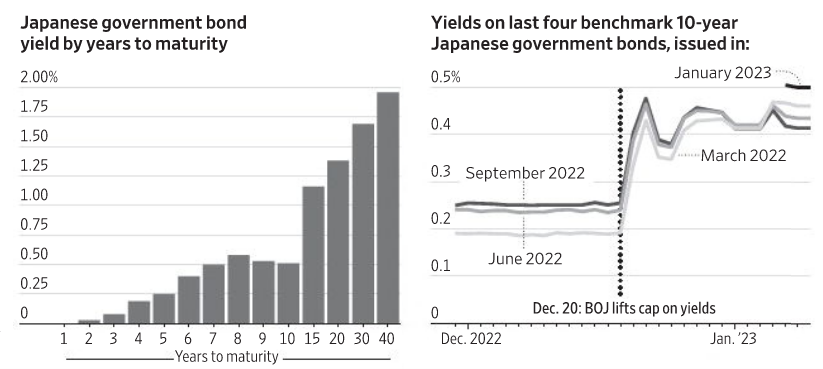

Yield curve control is a monetary policy action where Central Banks buys as many bonds as needed to keep the interest rate at a fixed level. Japan’s YCC experiment started as a strategy to exit deflation that had plagued the country since the 1980 bust. Until recently the BoJ YCC policy was to keep the 10-year bond yield at 0.25%. This NY Fed article from 2020 provides more historical details on the policy.

In December 2022, the BoJ raise their YCC target rate from 0.25% to 0.50%. The charts from the WSJ show how the unlimited purchases of 10-year Japanese government bonds impacts the curve (see kink in the middle) and also shows how the changes on Dec 20th impacted the curve.

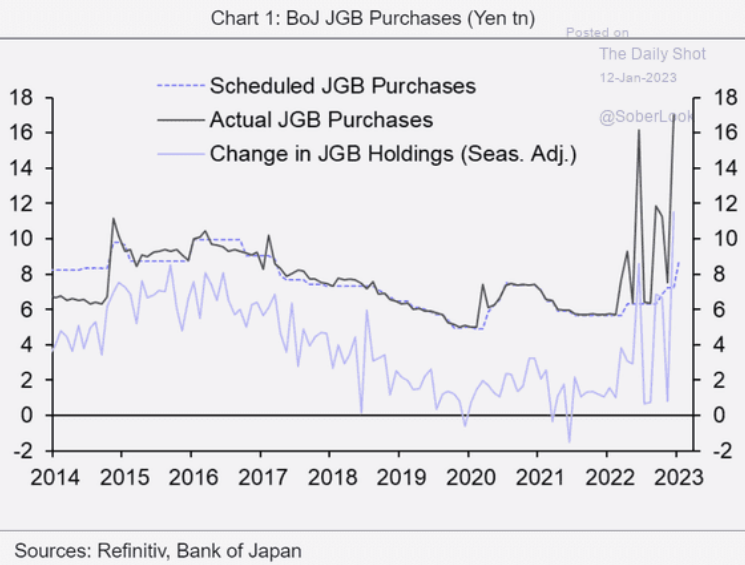

Following the December tweak, the BoJ’s purchases of bonds is accelerating, which was very likely not the aim.

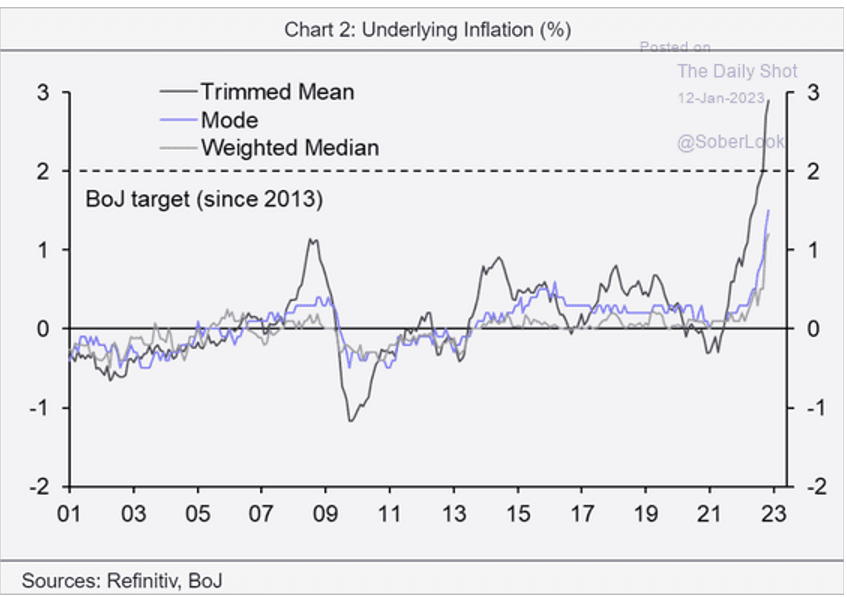

Although inflation has accelerated, BoJ Governor Kurada, continues to state that the inflation is merely supply led.

Ignoring what might be causing inflation, many citizens are unhappy about rising costs (inflation) when their savings don’t provide any interest income. The rising unhappiness of voters is what could ultimately pivot Japan from current policies.

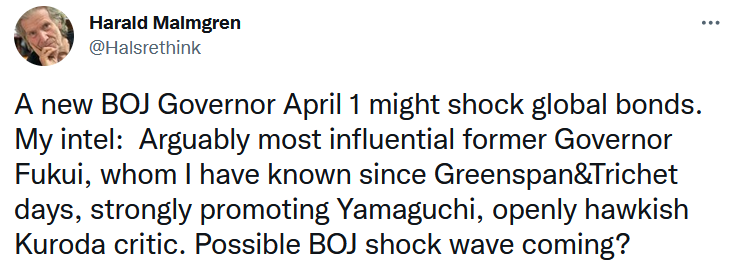

A BoJ leadership change could make a policy transitions smoother. Governor Kurada is set to retire at the end of March 2023 and the new head of the BoJ may have a different view on how to run monetary policy. This tweet from geopolitical veteran Harald Malmgren is thought provoking.

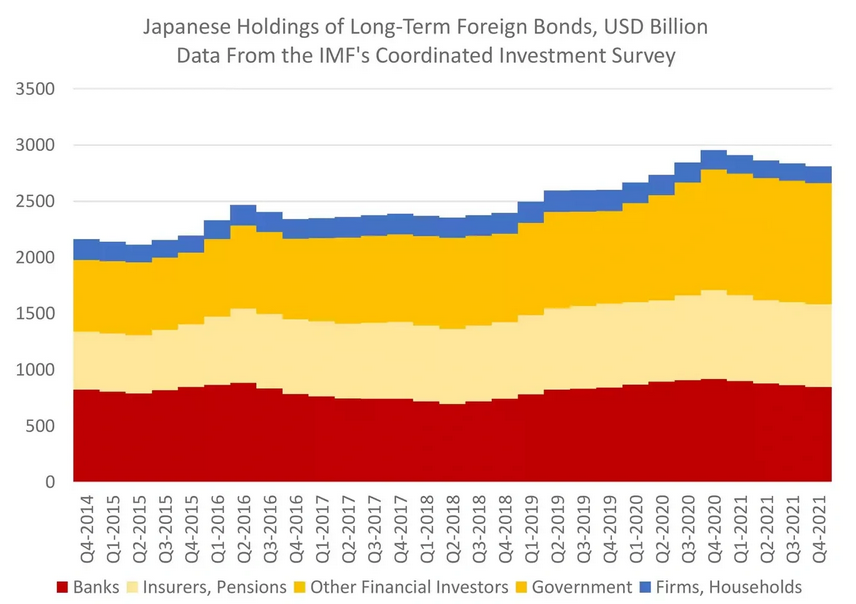

For more detailed insights into the importance of Japanese investment flows into overseas bond markets, we highly recommend this article from Brad Setser of the Council on Foreign Relations.

Financial flows from Japan like to slow sharply

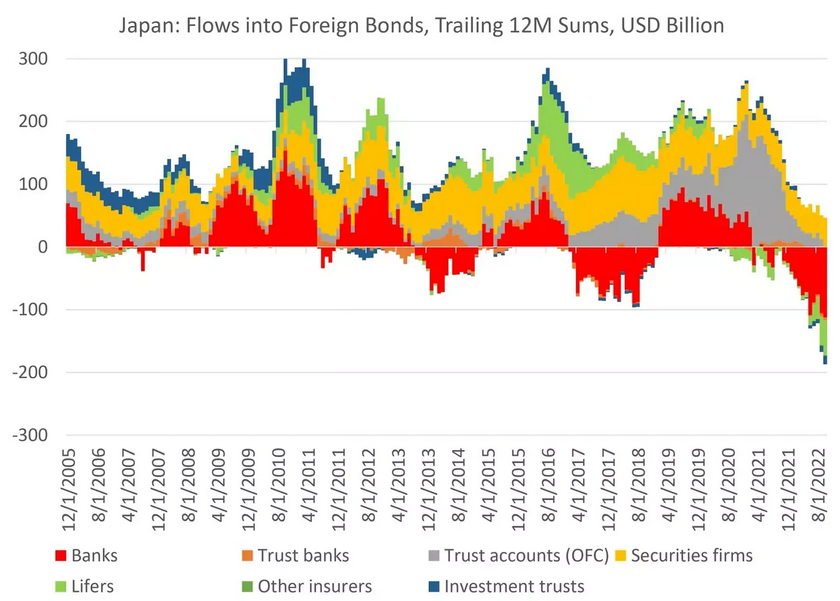

The flows have already turned negative

Sharp changes to capital flows from Japan should have a notable impact to global financial markets. The current JGB curve shows easing YCC should move the 10-year rate higher. If Japanese savers receive a higher interest rate, they are less likely to look overseas for high yields. At the same time, removing YCC could quickly make Japan’s mountain of debt unsustainable. It’s between a rock and a hard place for BoJ policy. This Reuters story highlights the growing opposition to YCC within the BoJ.

Any sharp changes to financial flows from Japan is likely to have a significant impact on global assets prices. As a result, we are careful with duration exposure in client portfolios, follow the bond rally from October, ahead of the coming BoJ leadership change.

We hope everyone is enjoying the strong rally to start 2023. We look forward to updating our readers on our evolving thoughts on global macro economics and its implications on asset markets.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |