The 2023 market outlook is murkier than a year ago and client portfolios are conservatively positioned. One year ago, equity valuations were near the 2000 bubble peak and Fed Funds rate was at zero. Avoiding expensive tech stocks and long-duration bonds was an obvious choice to us. For 2023, our highest conviction views are that stocks remain expensive and earnings risks are material. Wall street is projecting earnings growth of 5% and 10% in 2023 and 2024, respectively. Such a trajectory would be unprecedented during an economic slowdown.

The risks to our view our twofold. First is that the Fed engineers a soft landing, which lowers the risk of earnings cuts. Second, the still abundant liquidity ($2 trillion in reverse repo balances) chases a Fed interest rate pivot, leading to short-term rally. We will focus on making sure our economic expectations are accurate and worry less about a liquidity-driven rally.

We have a strong preference for bonds given the cautious outlook on the economy and earnings. US Treasuries offer ~ 4% yield and a recession could lead high single-digit total returns as bond prices rally on expectations of Fed rate cuts. We are less favorable to corporate bonds, especially lower quality bonds, as spreads are not factoring an economic slowdown. Within stocks, preference remains for value over tech, which remains overvalued and overowned.

Dispatch #22 on December 16th, 2022, breaks down the 2023 outlook following segments

- Stock valuations

- Earnings downside

- Positioning remains a long-term risk

- Recessionary signals

- Robust consumer

- Big picture uncertainties

The 2023 market outlook is murkier than last year

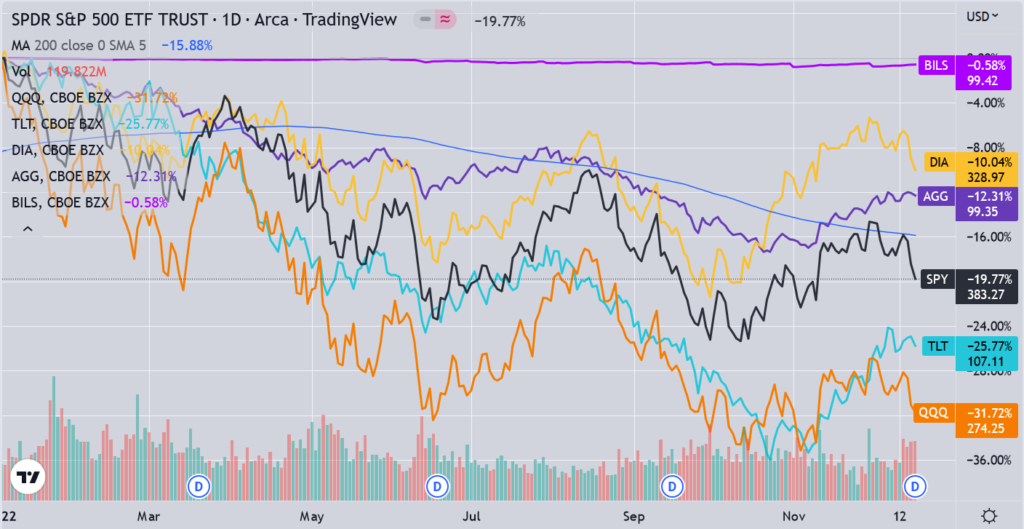

Conditions one year ago made it obvious to avoid expensive tech stocks and long-duration bonds. As the chart below shows tech (QQQ – NASADQ 100 ETF) and long-term Treasuries (TLT – 20-yr plus Treasury ETF) have done the worst YT2022. The drop in both stocks and bonds would have been particularly painful for retiree with a traditional 60% (stocks):40% (bonds) portfolio.

In contrast, short-term Treasury Bills (BILS) and the Dow Jones Industrial Average (DIA) with better valuations have performed far better. We still don’t like tech, but see the value in long-term Treasuries as recession risk increases in 2023.

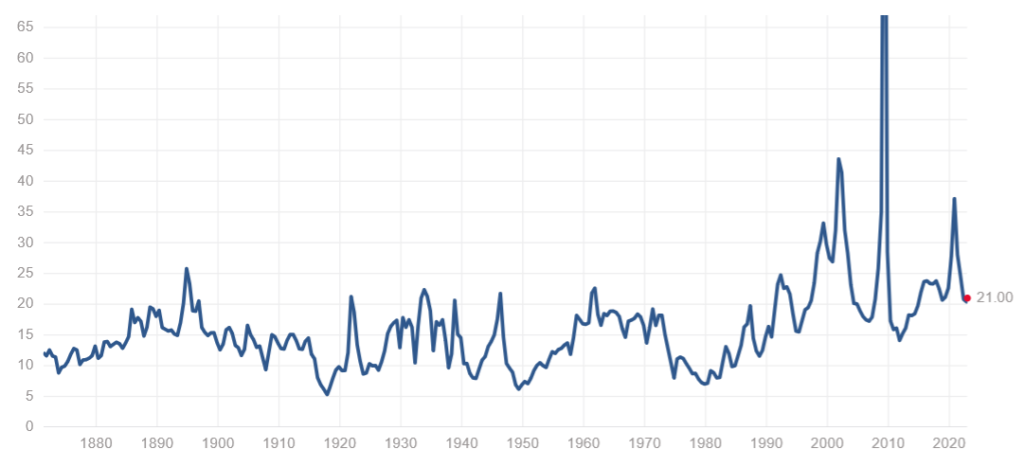

Equity valuations are unattractive even as they’ve eased from bubble territory

Trailing 12-month PE is elevated and there is substantial downside to historical mean of 16x and median of 14.9x.

S&P 500 Trailing 12-month PE

Source: multpl

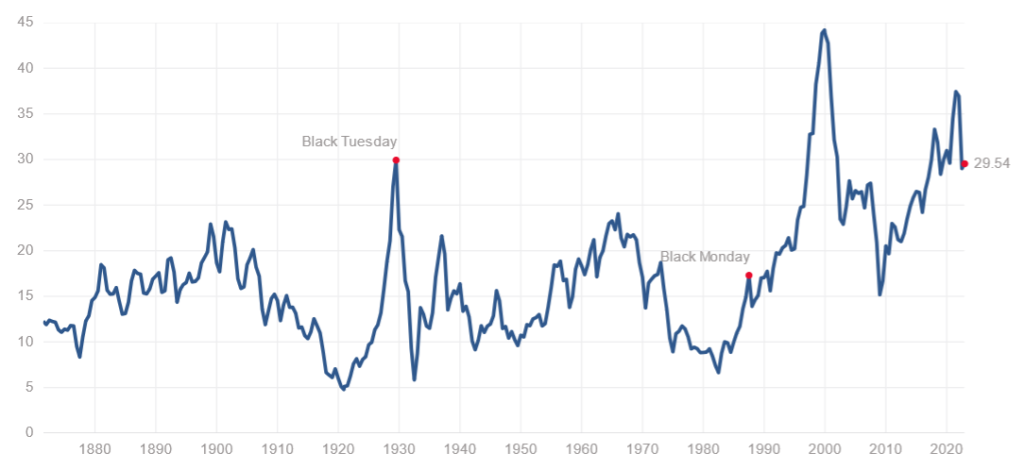

The CAPE (cyclically adjust PE) ratio provides a better longer-term valuation picture, and it is just as elevated. The historical mean is 17x and median 15.9x.

Given the much greater market share concentration and lobbying power of companies today, we believe the CAPE ratio should skew higher than the historical averages.

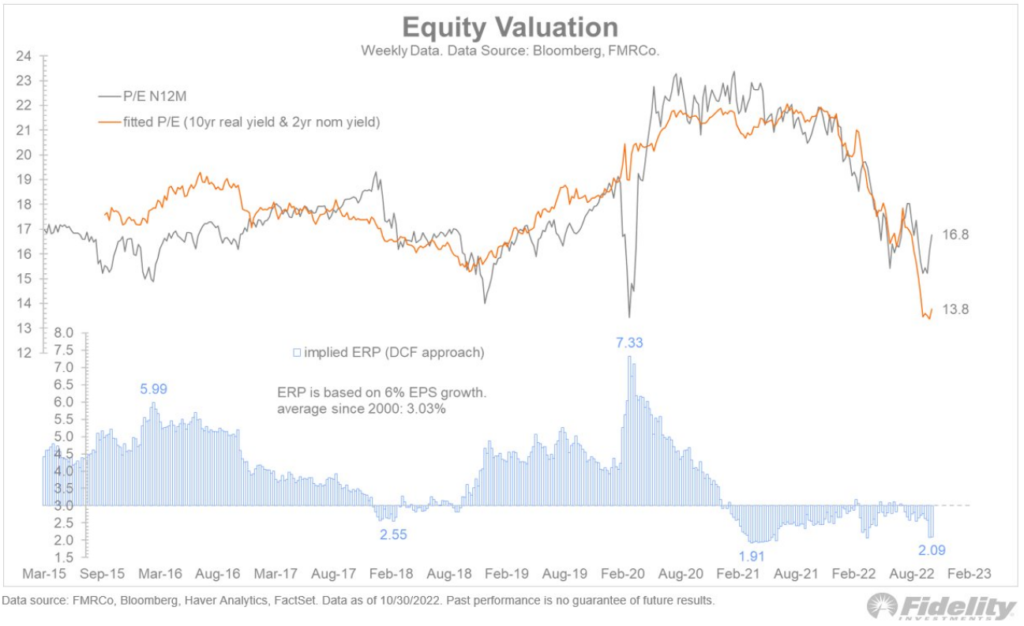

From an equity risk perspective, the valuation today is worse than one year ago. The idea here is that we want a higher return from stocks over the prevailing risk-free rate offered by government bonds. One year ago, short-term interest rates were at zero. Today they are at 4.5%. The chart below shows (the blue bars) how the expected excess return offered by stocks over bonds, aka equity risk premium, is lower now than 12 months ago. I higher equity premium is more attractive.

Yes, the S&P 500 is down ~20% from one year ago, but relatively to bond yields, the valuation is less attractive today.

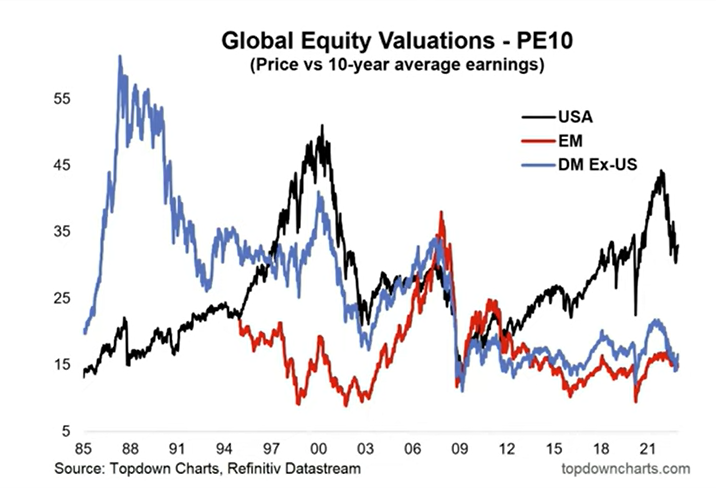

2023 market outlook could be better overseas

We are also closely watching non-US markets that are far more attractively valued. Despite better value overseas for most of the last decade, US stocks have significantly outperformed international markets. With a recession looming in the US, the performance divergence could reverse, especially for emerging markets. We are watching the US$ as a catalyst to allocate more to non-US markets. China reopening remains a key wild card for both the global economy and international markets.

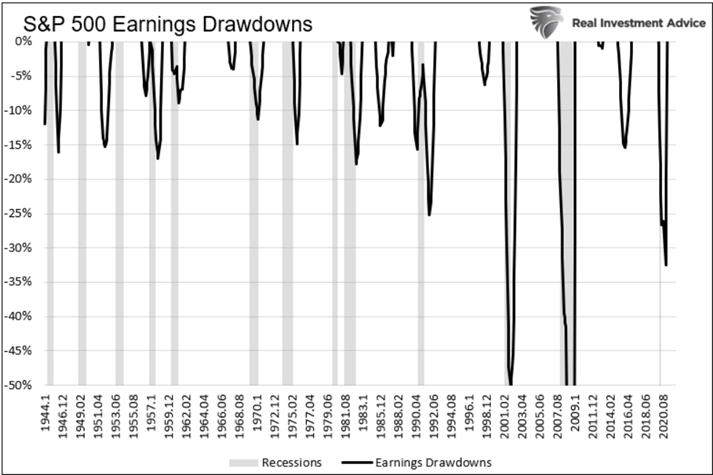

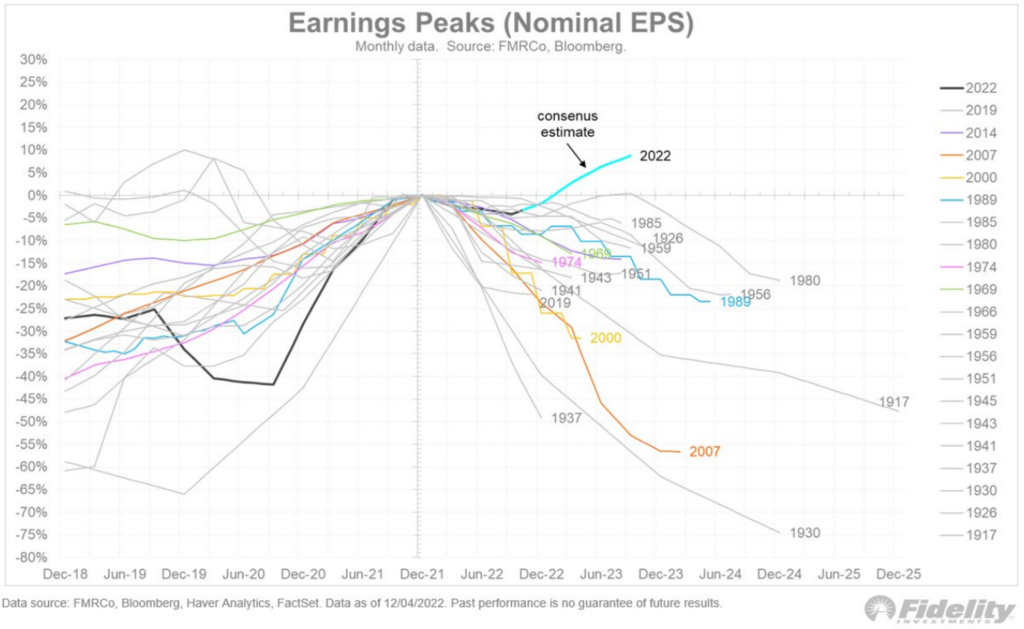

Earnings downside is likely

In Dispatch #18 we showed that the energy sector was an outsized source of 2022 earnings growth, which is unlikely to sustain. Dispatch #19 evaluated how earnings are finally starting to ease, but have yet to turn negative. Past economic slowdowns have led to earnings declining as the chart below shows.

If current earnings projections hold, they would be without precedent into an economic slowdown, which we believe is highly likely. More on the latter below.

Positioning remains a risk-longer term

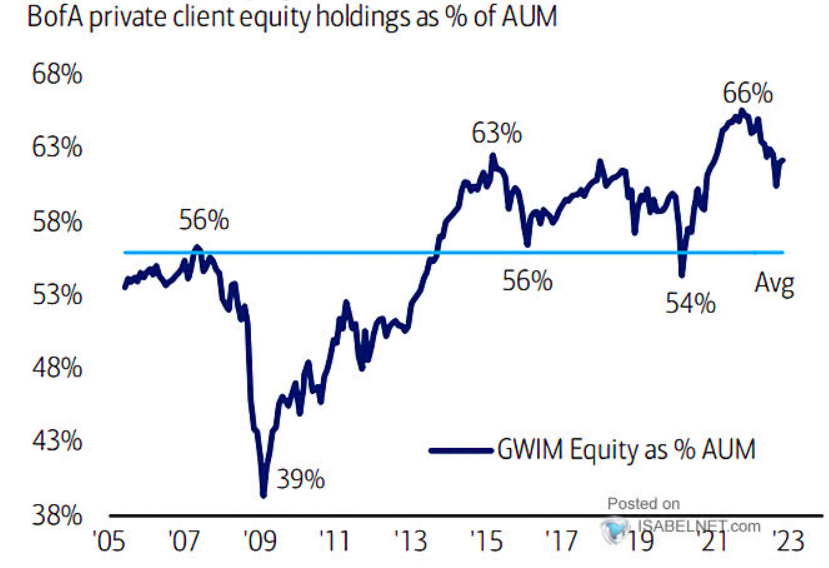

The market narrative has you believe that investors are lightly positioned in stocks based on this widely exchanged BofA institutional investors survey.

Yes, this institutional underweight can lead to short-term rallies, but are unlikely to offset overweight positions among non-institutional segments. What is discussed less often or circulated is that high net worth accounts remain overweight stocks.

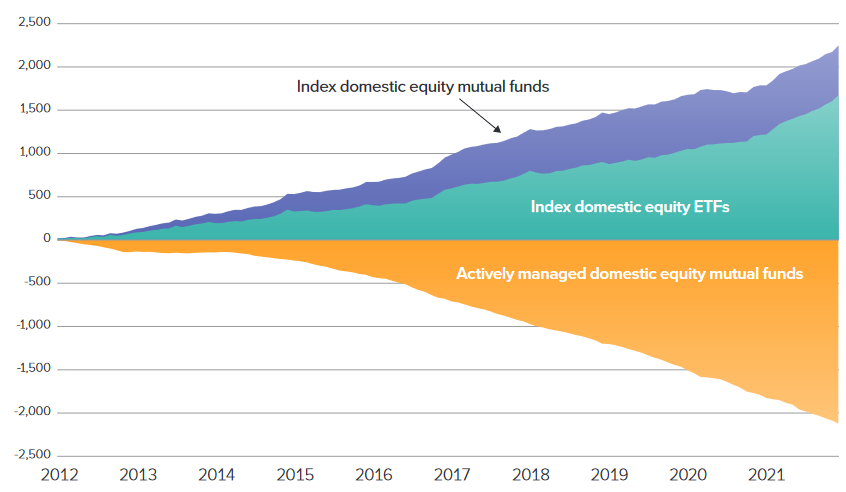

This matters because the relative importance of the active fund managers and hedge funds in the institutional survey has diminished. Active funds have lost significant market share to passive ETFs and index funds as shown below. Furthermore, equity mutuals funds have strict limits of how much cash they can hold, which is around the 5% range. Therefore, even if a fund manager is cautious, their adjustments are restricted by fund mandates.

Cumulative flows into domestic equity mutual funds, index funds and ETFs ($ bn)

Source: Investment Company Institute 2021 factbook

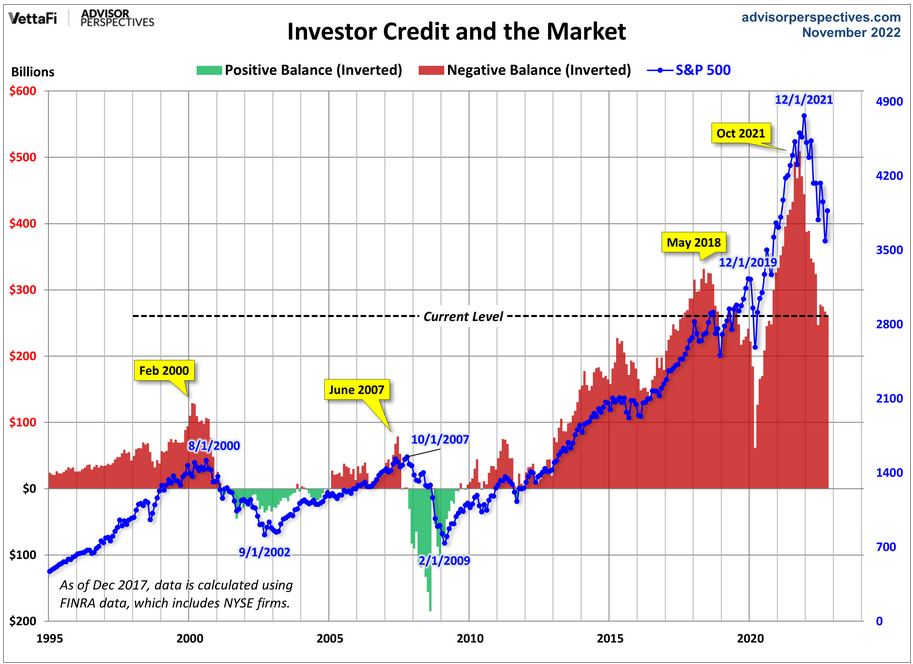

Margin loan balances also show that we are nowhere near levels reached during prior bear market bottoms.

Recessionary signals

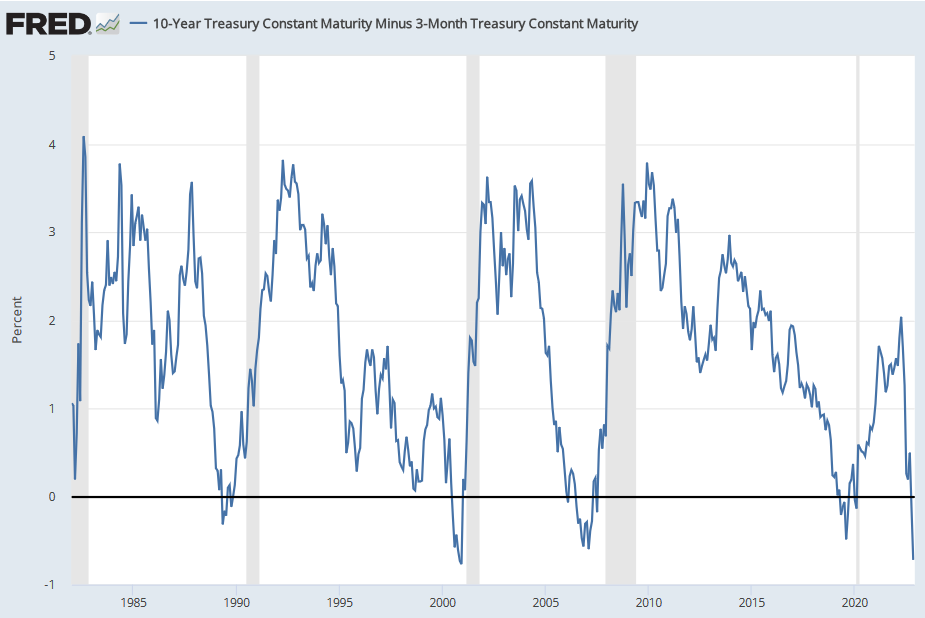

The 3-Month to 10-year Treasury curve inversion has led to a recession 100% of the time.

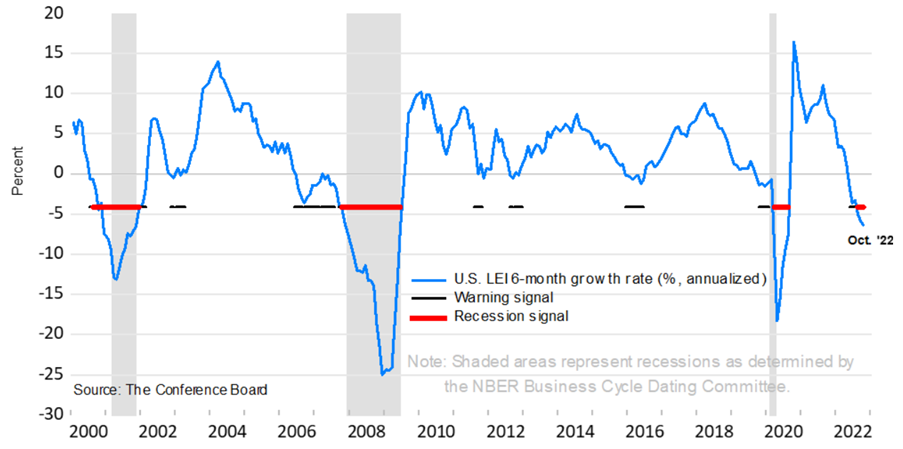

Leading Indicators has a similar strong track record

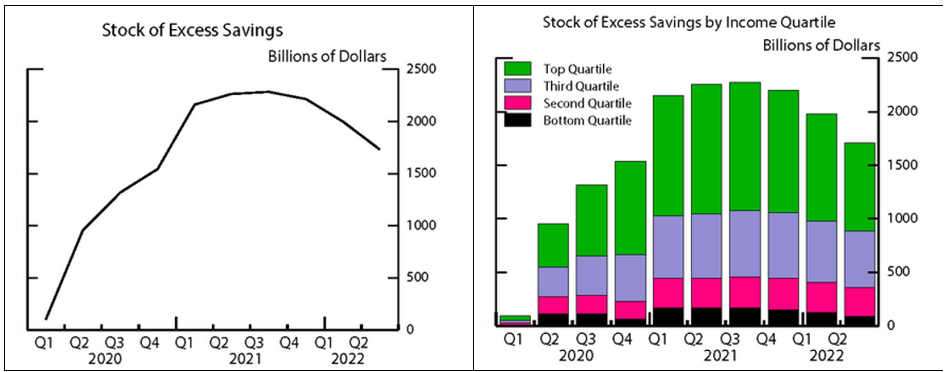

Consumption remains a key economic strength

The offset to the macro variables highlighted above is strong consumption, which has been helped by excess savings built up over Covid. These savings are heavily skewed to the top 50% of income households.

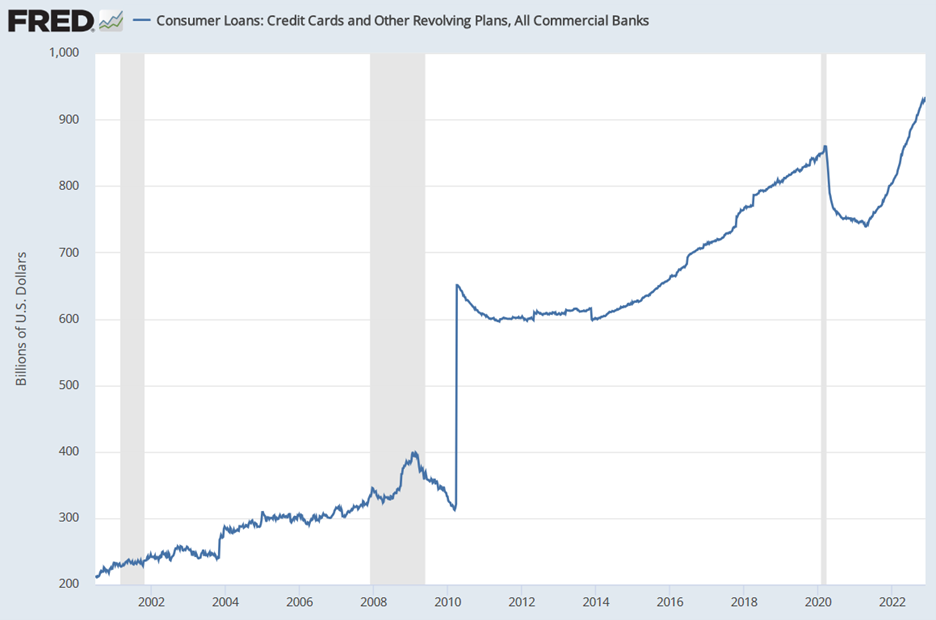

Some households have returned to credit cards to maintain consumption as the chart below illustrates.

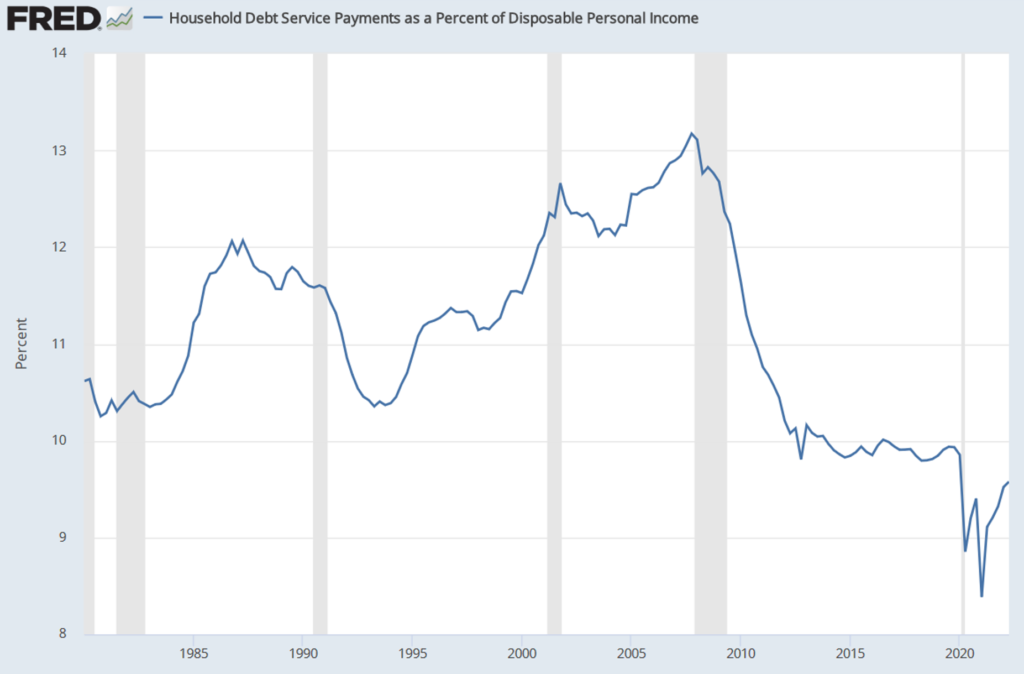

Almost entirely fixed-rate mortgages, unlike in the mid-2000s, have improved debt service.

2023 market outlook has big picture uncertainties

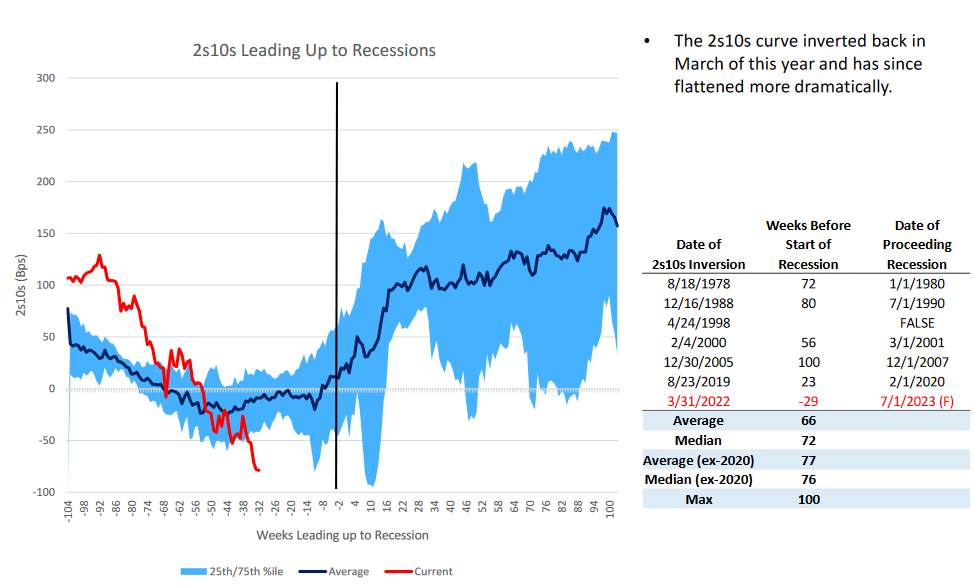

Higher rates take time to slow economy: ~66 weeks from initial curve inversion

Since the late 1970s, it has taken 66 weeks from curve inversion to recession onset. The robust consumer probably pushes recession risk further away.

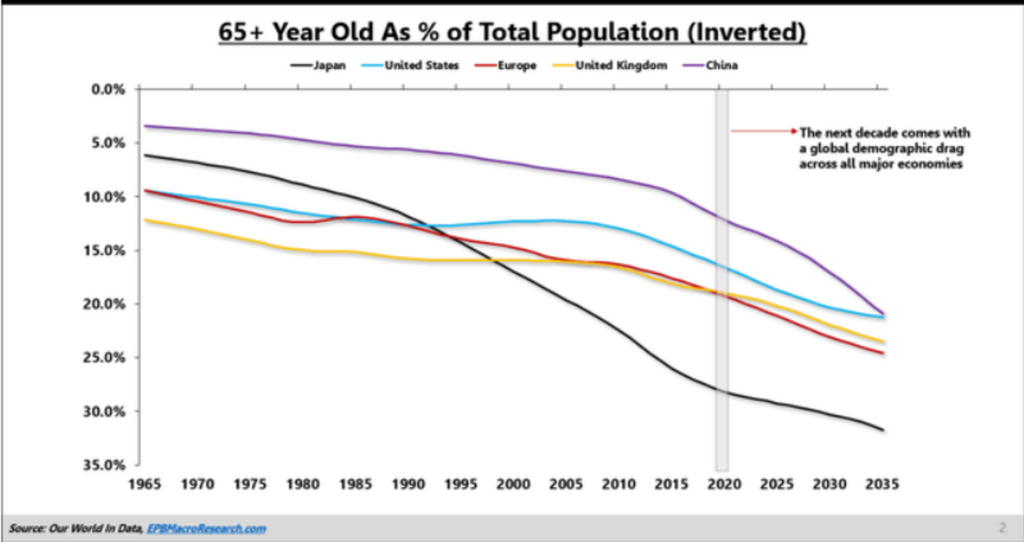

One of the keys to the soft landing vs. recession debate is the trajectory of inflation. Most macro analysts’ mental model is of Japan-style structural deflation as population ages.

Source: EPB Macro

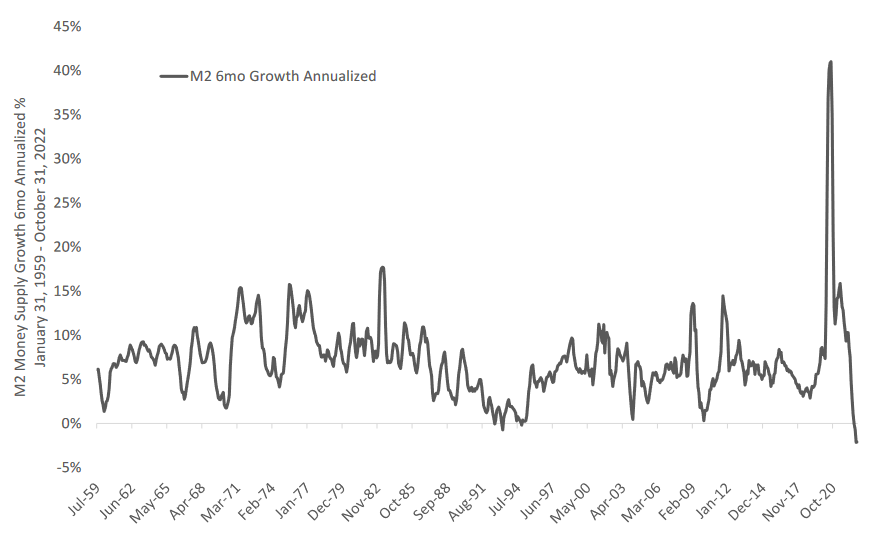

We are open to the idea that the US experience might be different. Could a steadier service consumption from retirees and a shrinking workforce lead to higher inflation? While we are open to that structural possibility, we believe the sharp downturn in liquidity will slow inflation in the coming quarters.

We may not hit the Fed’s 2% target in 2023, but we should see meaningful progress as the economy cools.

In conclusion, we see a highly uncertain 2023 and prefer to preserve retiree capital rather than assume liquidity will carry the day. Inflation will be slow to return to the Fed’s 2% target, which will require rates staying higher, which can create unexpected problems in an economy where the government and corporate sector is heavily indebted. The UK pension LDI crisis and the gating of the Blackstone and Starwood REITs are have exposed our addiction to leverage and liquidity.

Our longer-term structural thesis is that debt will not grow at the same pace as post GFC era without Fed QE. This either means slower growth or QE in a higher inflationary environment that may require unorthodox measures from the Fed. Precious metal and digital assets are likely to react favorable to the latter outcome.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |