The China economic slowdown is well documented, and foreign investors have been notable net sellers of the country. This post looks at the economy’s overreliance on investments, the need to stimulate consumption and tactical near-term positives. As fundamental analysts that have followed China since the 1990s, The Dispatch can’t get excited about doubling down on investment spending to correct the structural imbalances. China has overinvested in many areas of the economy (residential housing is the highest profile) and a sustainable growth solution requires stimulating consumption. Most of the policies announced over the past months are attempts to reignite investments. These policies could provide a cyclical boost but are unlikely to tackle the problem. A substantial policy shift to stimulate consumption will be a signal for more durable, multi-year economic growth. All that said, weak sentiment and low valuations could underpin tactical upside short term. For example, China’s weight in global stock indices is now less than Apple’s!

A little economic backdrop

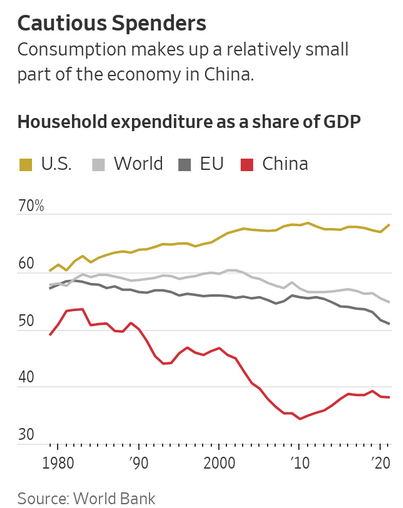

China’s growth model is based on cycling high savings into investments. In a closed economy like China’s, the high savings (>30% today and above 20% for 3 decades) must be invested domestically. This has driven an investment boom over the past 30-40 years. As a result, investments account for >60% of GDP, which is unusual for a large economy. In contrasts, the US and most other economies are >50% consumption based, with investments much lower. It’s the reverse in China.

GDP = Consumption + Investments + Government spend + (exports – imports)

This investment-led model successfully took China out of low-income status into a middle-income economy. That rapid growth was achieved by adding capacity in fixed assets like real estates and infrastructure. Initially it was much needed capacity, but after 30+ years, many pockets of excess investments have developed.

Residential real estate is the most well known malinvestment. It’s likely that infrastructure investments also dropped below positive RIO (return on investments) over the past decade. The first high-speed rail line between Beijing and Shanghai, completed in 2008/09 would have been high ROI. The current buildout between 3rd tier cities is likely to be negative return. High-speed rail is a central government project and not locally funded. We discuss local government debt below.

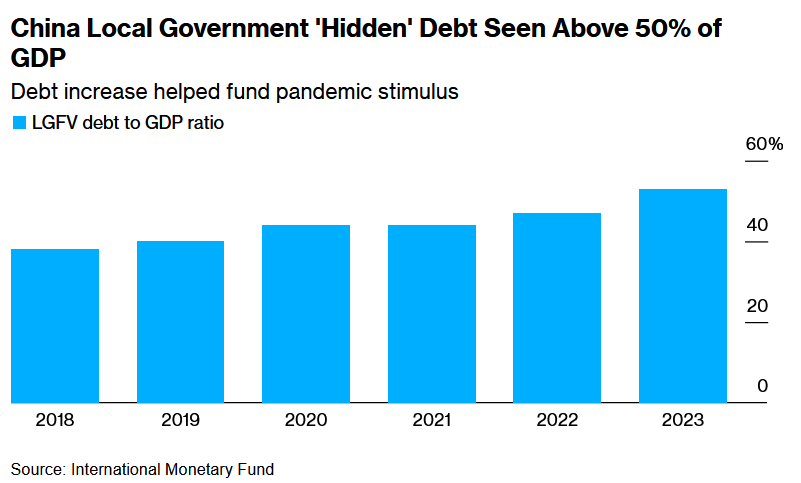

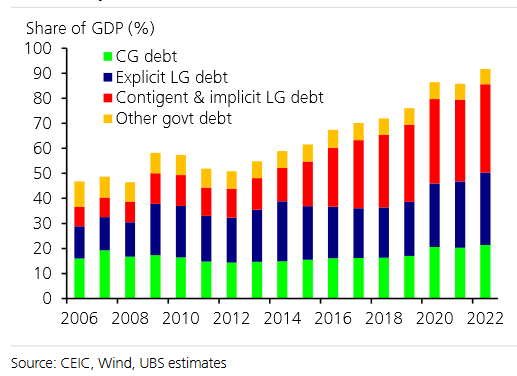

Excess debt at local governments

Over the past several decades each economic slowdown has been tackled with additional investment stimulus programs, much of it funded by local governments. This has created opaque, high-debt, local governments that are struggling service the debt. Local government debt (implicit central government liability) is much larger than the official state debt.

Source: Bloomberg

When you add the local government debt with implicit state backing, China’s debt load is a hefty 92% of GDP, according to UBS.

The largest source of local government revenue is land sales, which is how real estate ties into this mountain of debt. Falling property prices have dried up demand for land and, along with that, local government revenues. This August 2023 Bloomberg article provides details of how most LGFVs need constant financing to stay afloat because the assets aren’t generating enough cashflow. We would not be surprised to see policy-easing measures like allowing banks to lend to LGFVs to release pressure.

China is wedded to stimulating investments

It is disturbing to see Chinese leaders try to squeeze more out of the investment lemon once again. They have announced cuts to stock-trading taxes, lowered home mortgage downpayment requirements, lower minimum mortgage rates for second-time homebuyers and told banks to lower mortgage rates. It’s fine to stimulate demand for real estate, but as a middle-income economy China needs to pivot to increasing consumption broadly as it’s already overinvested in many areas.

Investment-led growth strategies aren’t bad in isolation. Countries like Korea and Taiwan have followed a similar investment-led growth trajectory, but they have managed to shift to high-value industries and maintained a high level of consumption. Geopolitics are making China’s shift to higher value industries more difficult, which makes the shift to consumption even more important.

Ideology and entrenched institutions prevent consumption pivot

This WSJ article provides excellent backdrop to why the Chinese Communist Party is unlikely to back a switch to consumption stimulus.

The quote below from the WSJ article is a good summary of the ideological opposition to consumption.

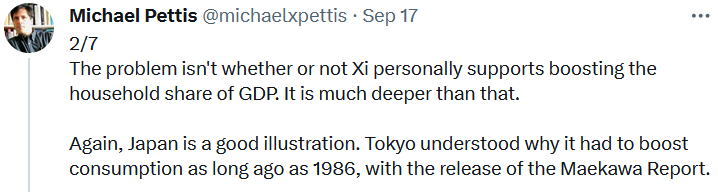

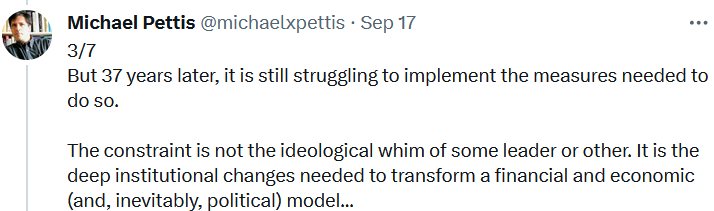

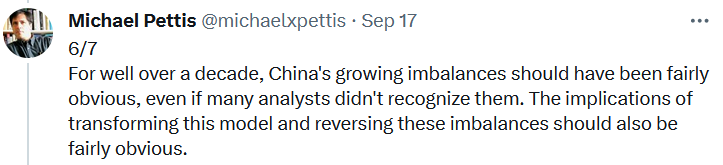

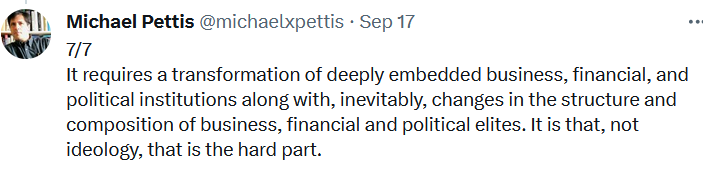

An equally stiff headwind will come from institutions that have entrenched roots to benefit from investment stimulus. These tweets from Prof. Michael Pettis (good follow on China & global economics) highlights the problem.

China’s central command of the economy is also proving to be an obstacle as another WSJ story highlights. President Xi’s consolidation of power has led to slow responses to the economic troubles as most decisions originate from a single person.

Source: WSJ

Yes, China has deep imbalances, but there’s no reason China can’t fling a bunch more money into the same over-invested sectors and goose growth and markets. That may provide short-term market upside, but is not a durable solution in our view.

China slowdown impact on US

The US relies on China for good imports, and our export exposure (outside of aircraft) to China is not significant. The excess investment in China could possibly allow the country to use lower prices to raise exports. This should be positive for CPI in economies importing from China. In addition, a weaker Chinese currency (a side effect of the sluggish economy/stimulus) could will help lower import prices. Chinese deflation is positive for US CPI ebbing. Plus a stronger Chinese economy may have driven energy and material prices meaningfully higher, which would have added inflationary pressure globally. While a China slowdown is not a positive for US growth, it’s unlikely to be a notable headwind either. Yes, there are bound to be second order effects like more China exposed economies like Germany slowing faster, which will then have a knock on impact on US growth.

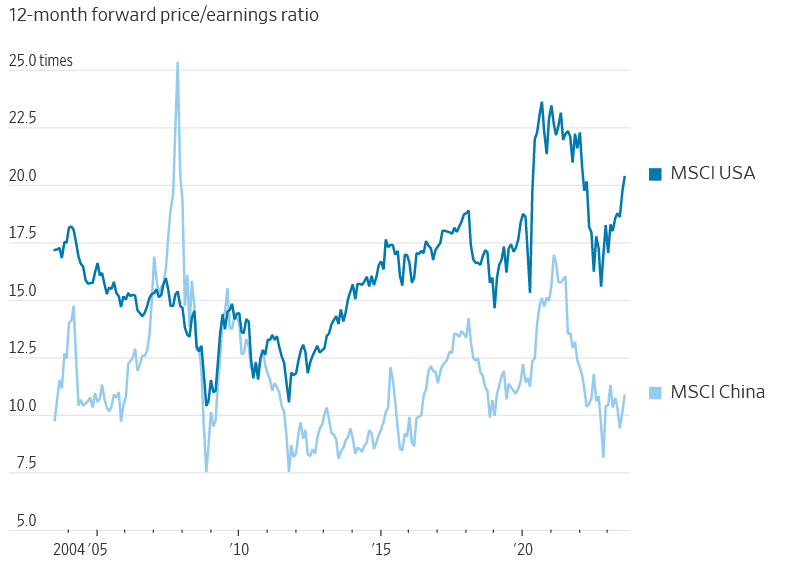

Valuation and positioning could support China equities

Valuation and positioning make Chinese markets attractive for our contrarian instincts. The current valuation gap is the widest in a decade.

Source: WSJ

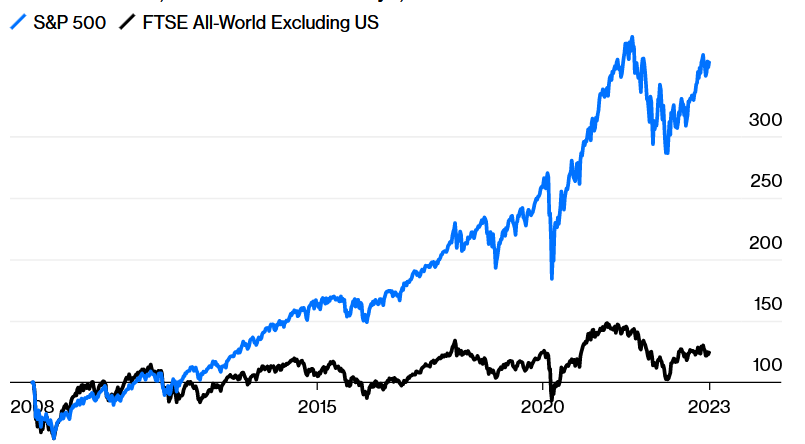

We do know that China and emerging markets overall have traded at a notable valuation discount to the US for over a decade. The valuation gaps have developed as a result of the US outperformance since the global financial crisis of 2008 when the Fed started its monetary expansion. Valuation are rarely a short-term performance signal.

Source: Bloomberg

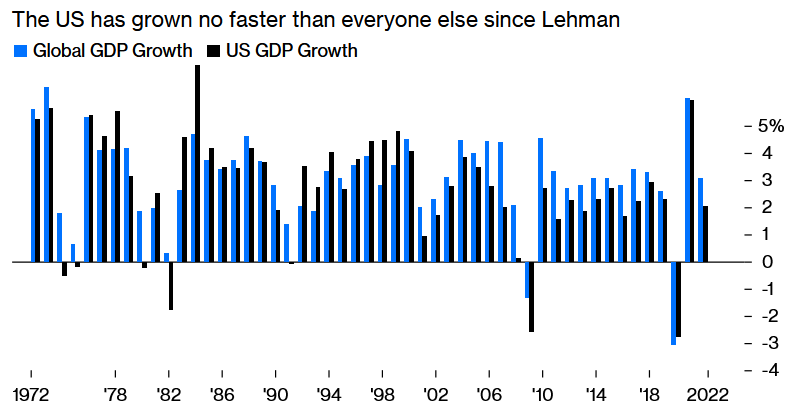

The superior US performance is not on the back of faster economic growth since 2008.

Source: Bloomberg

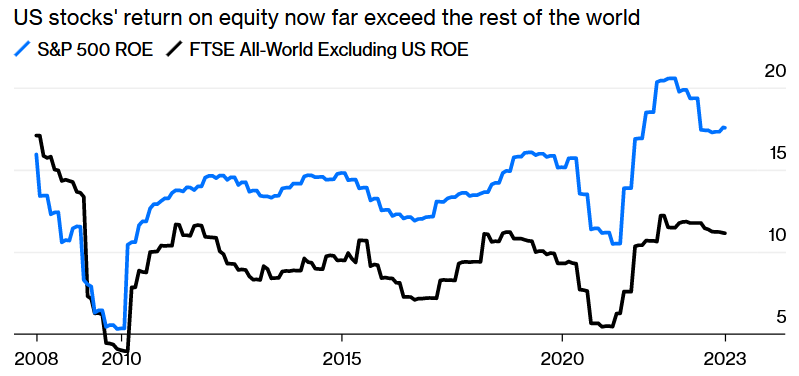

But ROE (return on equity) has sustained a large lead over non-US stocks. With interest rates higher and tax unlikely to fall further in the US, it’s fair to question if the gap can be sustained.

Source: Bloomberg

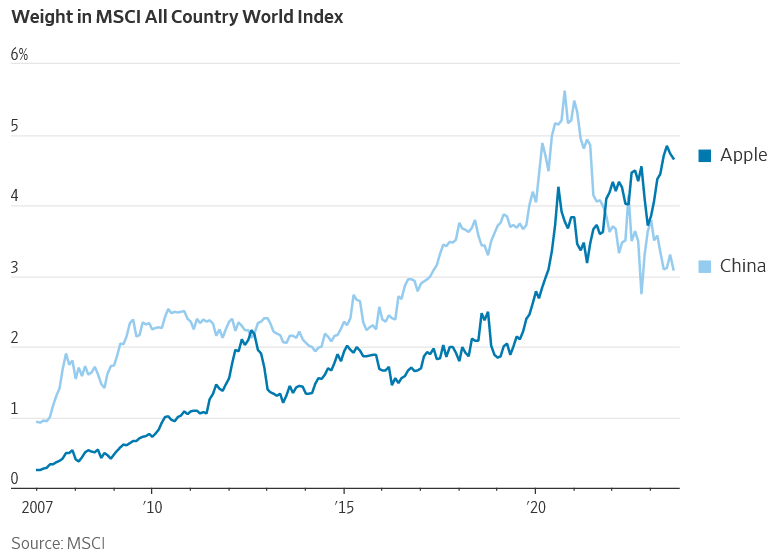

This simple, yet compelling chart may illustrate China’s valuation appeal: Apple has a larger weight in the widely followed MSCI all country stock index than China. More of each passive investment dollar goes into Apple than it goes into all Chinese stocks.

Source: WSJ

While there’s potential for tactical bullish moves in Chinese stocks, we would need to see attempts to stimulate consumption to get really excited about the long-term prospects. The odds are stacked against the latter outcome, in our view.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |