The failures of Silvergate Bank and Silicon Valley Bank (SVB) this week highlight the economic risks from high interest rates. This should be a warning to the Fed and investors alike that the highly indebted US economy is already in financial stress, even as credit spreads remain normal. Historically, financial market participants have looked to credit spreads (the interest rate premium over Treasury Bonds of equivalent maturity) to gauge tightening financial conditions. This week’s events suggest that sharply higher rates in a heavily indebted economy can be equally damaging. The sharp rise in both junk bonds and leveraged loans are likely point to further trouble in the coming months. Our client portfolio remains cautiously positioned with a skew towards bonds as we laid out in our 2023 Market Outlook.

Dispatch #2 of 2023 completed on March 10th evaluates the risks from high interest rates.

Risks From High Interest Rates: Level matters as much as credit spreads

The failures of Silvergate Bank and Silicon Valley Bank (SVB) this week highlight the risk from high rates. The Fed, on the other hand, mostly focuses on financial conditions indices to monitor monetary policy transmissions, but that only captures credit spreads (the interest rate premium over Treasury Bonds of equivalent maturity). The analysis below looks at the surge in junk-rated debt (below investment grade) and Leveraged Loans during the zero-interest rate period (ZIRP) and how that might point to rising economic risks.

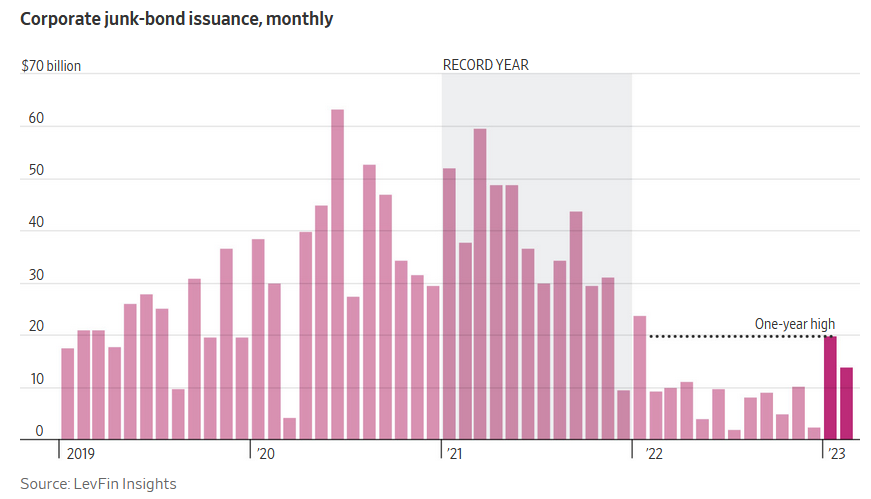

The following charts provide a summary of the heady issuances of junk (aka non-investment grade) bonds at historic low rates in the recent past. The market for junk bonds dried up in 2022, but showed a modest YTD 2023 pick up. The events of this week would have halted issuances.

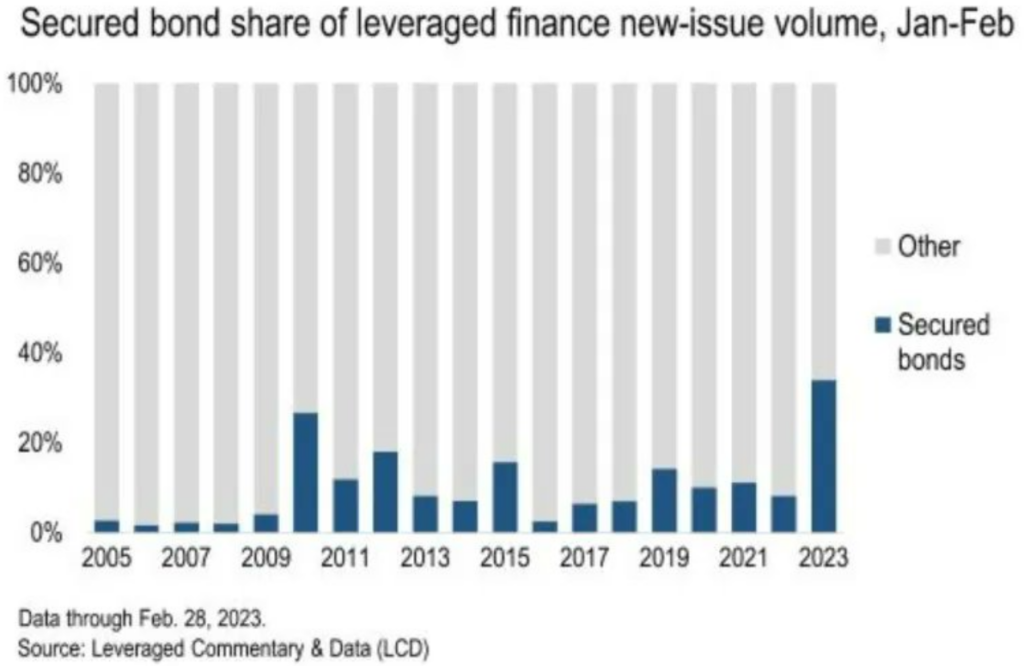

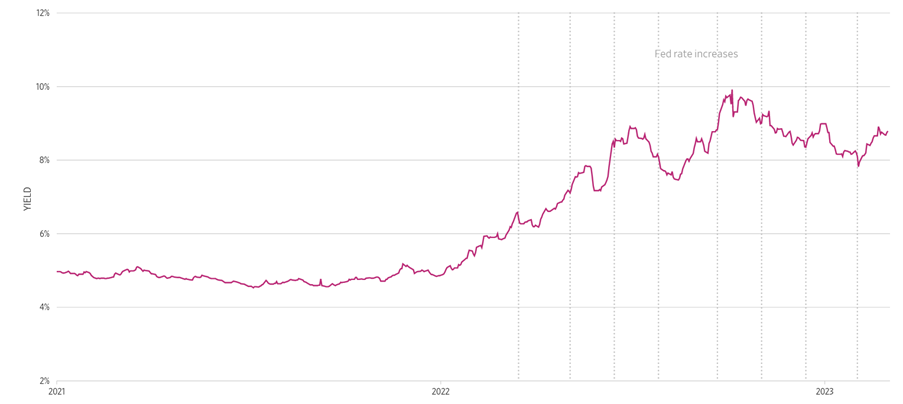

However, the 2023 issuance pick up has come with less favorable terms for issuing companies. The market has not really eased, as the chart above shows.

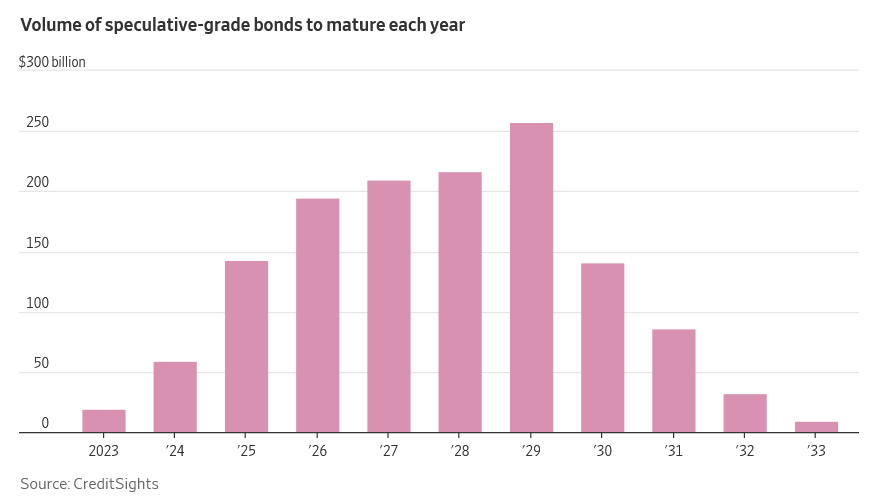

Junk bonds are fixed rate, therefore a positive interpretation of the chart below is that junk-rated companies have borrowed at cheap rates for longer. This lowers the risk to “low quality” large companies from the Fed’s rate hikes since March 2022.

That favorable interpretation can be seen in the maturity-profile chart below. Re-financing needs only really pick up from 2025.

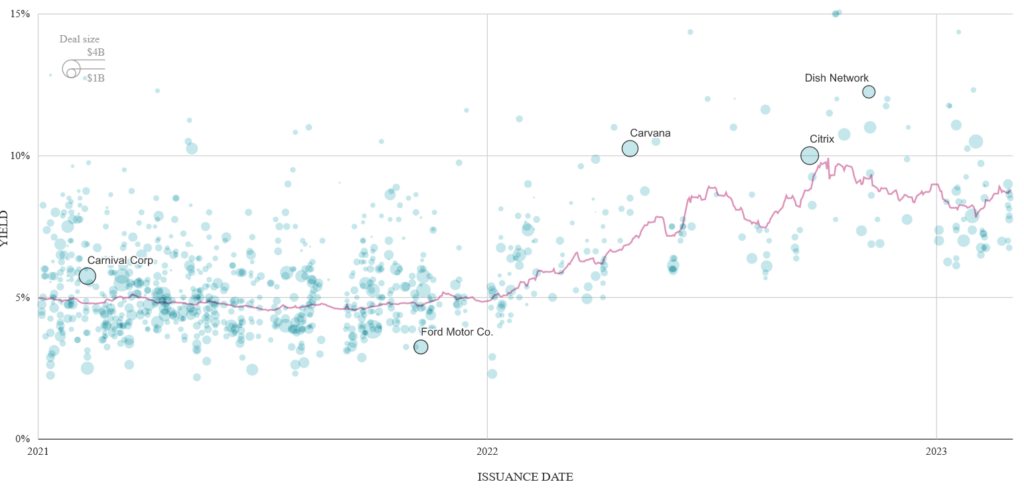

The average rate of junk bond issued has more than doubled since the lows of 2021. Refinancing could materially strain company finances if higher rates persist. This is not our view, but there are other signs that high rates are already impacting corporate solvency.

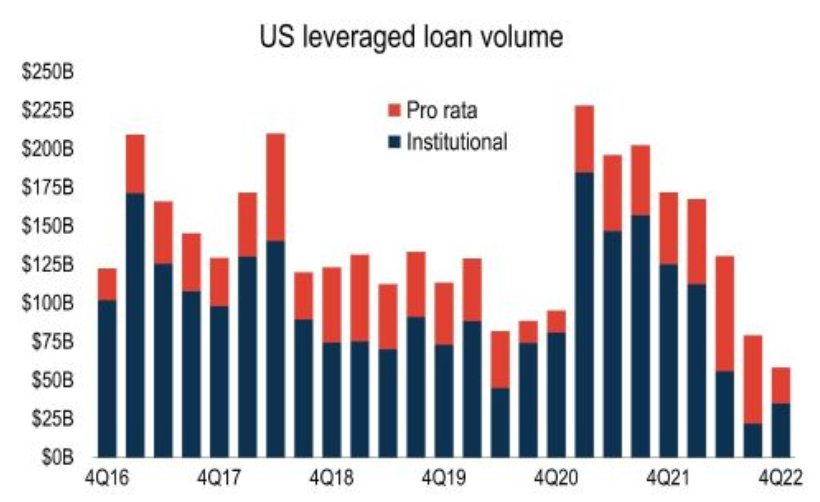

Floating rate loan defaults are already here

The floating-rate Leveraged Loan market has seen a cycle similar Junk Bonds. A spike in issuance during ZIRP and a sharp slowdown from 2022. Companies that aren’t large and financially strong to issue Junk Bonds issue Leveraged Loans. Private equity deals are some of the key Leverage Loan issuers.

We are now starting to see defaults of companies saddled with high floating rate debt as the headline below shows. This WSJ article highlights the failure of a large office portfolio that was leveraged through a private equity deal.

For the moment, real estate sectors hit by post-Pandemic change is showing financial distress. This WSJ article says, “as many as 10 hotel owners in the US filed for bankruptcy this January, compared with just two in January 2022”.

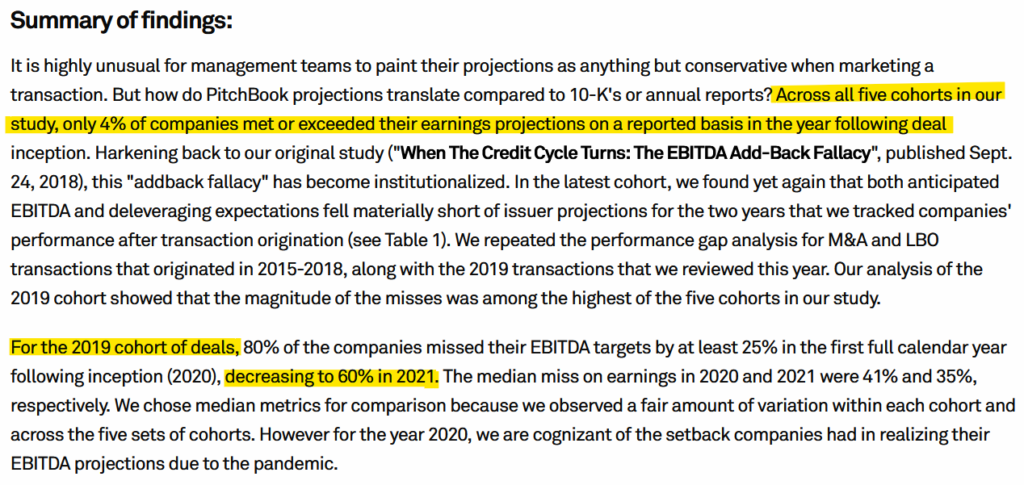

EBITDA over-estimation is rampant, says S&P

A similar fate may lie ahead for other sectors as industry-wide rosy assumptions are unable to service debt. This recent S&P Leveraged Finance Study raise our confidence that financial stresses are likely far more widespread. S&P reports a shocking level of missed EBITDA guidance from companies post M&As (merger and acquisitions) and LBOs (Leveraged Buy Out by Private Equity). Private equity is one of the primary users of the leverage loan market, because the companies are heavily indebted.

The report summary is shown below, with our highlights.

60% of 2019 M&A & LBO companies missed projection “by at least 25%” during the 2021 boom. This is worrying because what happens if the economy rolls into a recession? Also, remember that S&P is in the business of encouraging deals and activity. It’s not in their DNA to throw cold water on a sector that feeds the firm.

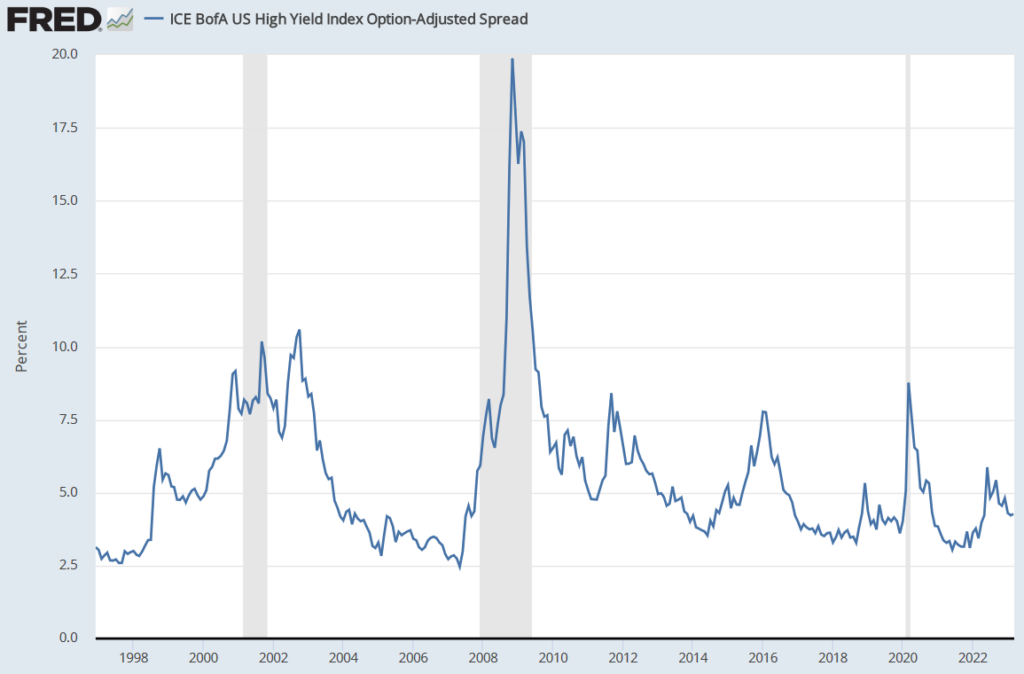

And, stress is visible even with credit spreads remarkably well behaved, which speak to the impact of high rates.

Credit spreads have not risen

Bank failures point to rate stress

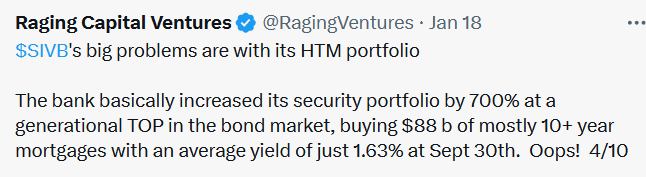

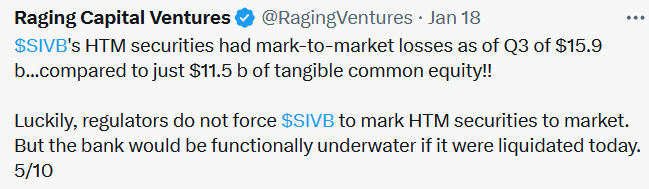

The failures of Silvergate Bank and Silicon Valley Bank this week are partly due to higher rates. Rising rates led to the bond portfolio losses at Silicon Valley Bank. A bank-run then forced SVB to realize those losses.

This twitter thread provides an excellent summary of how high rates (along with other factors) contributed to the collapse.

Additional insights on banking system risk and the SVB failure are available here, here and here. A few of the tweets are shown here.

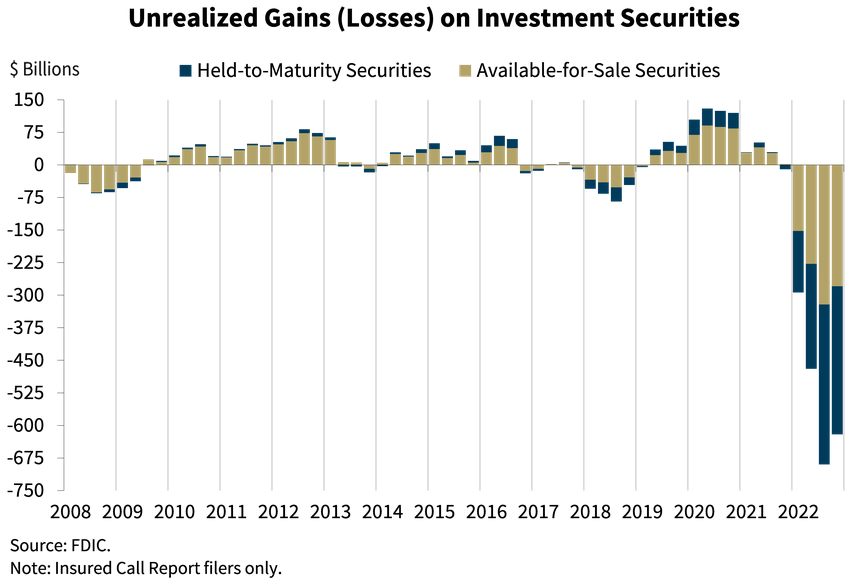

Yes, the bank run forced the bank to realize bonds losses, but let’s not forget that high rates created those losses. The unrealized bond losses of the entire US banking system is below. The losses are not small, but only catastrophic if there’s a systemic loss of confidence.

While the Fed’s monetary policy is guided by Financial Conditions indices, which don’t capture the level of interest rates, we think this week’s events will caution against the 50bp rate hike next week. The credit spread is the extra return that investors receive from corporate bonds over Treasury securities) and does not capture the level of rates.

We remain cautious

We continue to believe that a reckoning is in the wings for all the cheap money deals that investors gorged on over the past several years. Prior to this week, the rising financial stress was a subtle undercurrent. For us, reading increasing number of stories about defaults in the WSJ this year was reminiscent of 2006/07. That might have changed this week with the two bank failures, which has brought the stress to the surface. It’ll be important for Government action to this weekend to stop the SVB failure cascading to a broader loss of confidence.

RockDen client portfolios remain cautiously positions. Our preference for bonds (see 2023 Market Outlook) was a drag YTD as stocks rallied to start the year. That changed this week, but short-term bonds (2 year) are merely flat YTD, but portfolios have avoided volatility this week. We still see a higher probability of stocks hitting new lows in the coming year. We will monitor markets to adjust portfolio risks and only increase exposure to riskier assets like stocks when conditions are attractive. Our background in emerging market and digital assets provides comfort with riskier assets when the reward is appropriate. However, we do not believe our fiduciary duty is to buy and hold a static portfolio despite clear and rising economic/market risks.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |