It is clear to us that inflation has peaked, but getting inflation down to the Fed’s 2% target will be a challenge. It’ll be a challenge for our overly indebted world to sustain 5-6% interest rates for a prolonged period, which is the Fed’s guidance. However, there’s plenty of financial liquidity sitting on the sidelines ready to deploy capital into risk assets. We are addicted to liquidity, and each sniff of a Fed pivot leads to stock and bond rallies with little discussion about longer-term constraints.

Over the past several months, Treasury Bond yields have dropped, which is pricing core CPI returning close to the Fed’s 2% target. However, the same bond market did not accurately predict the CPI surge, which shows that markets aren’t always accurate. When we started writing Dispatch #21, the markets were not overly focused on jobs. That changed this week with Chairman Powell’s puzzlingly dovish speech at the Brookings Institution, and then a strong job report that further added to volatility. Therefore, a discussion about the interaction between sticky CPI, jobs, murky statistics and recession is timely. The Fed needs many of these items to cool in order for core inflation to hit the 2% target.

Dispatch #21 completed November 30th, 2022, covers the inflation outlook.

Fed’s 2% Inflation Target

Over the past couple of weeks, markets have rallied on the heels of a positive CPI print. We saw October headline inflation rise 0.4% MoM (7.7% YoY), which was less than analysts had projected. We also saw core inflation, excluding food and energy prices, beat expectations as well, and only increasing 0.3% MoM (6.3%YoY). If this sounds familiar to you, it might be because markets faced a similar situation in the summer when we saw lower than expected CPI numbers in July.

That positive CPI print extended the summer stock market rally 0f about 16.5% before rising CPI numbers sent the market back to year-to-date lows. While we are confident that inflation has peaked, we are less confident that core inflation will quickly trend toward the Fed’s 2% target. However, we are vigilant and we discussion below our area of focus (hint – not just government statistics).

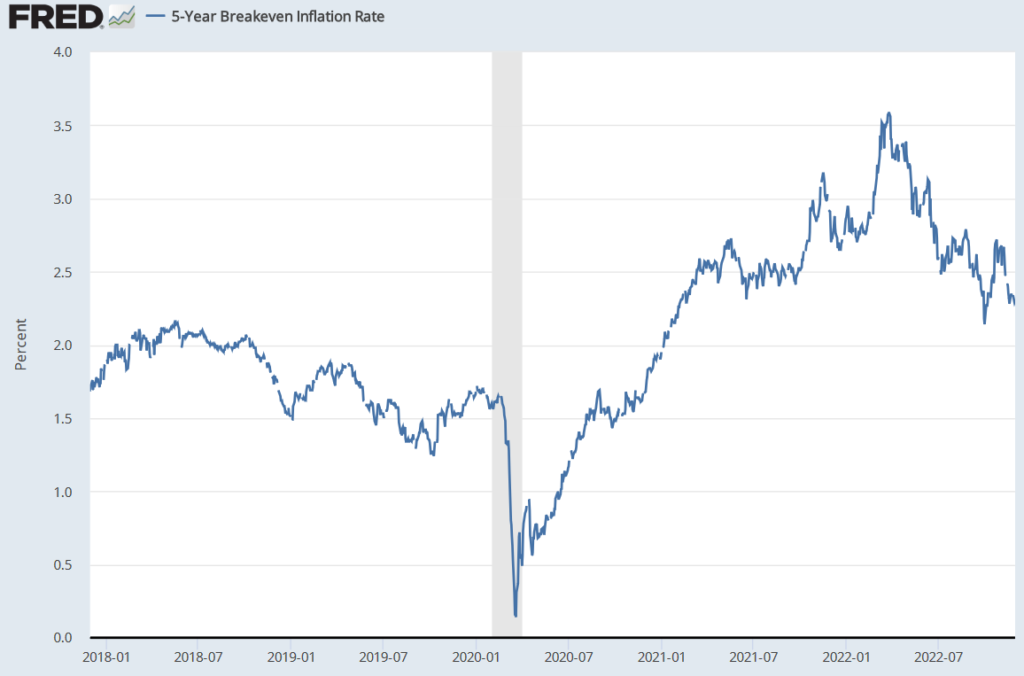

The Bond Market see inflation heading to 2%

The bond market is pricing inflation returning close to the Fed’s 2% target. The 5-year inflation breakeven rate peaked at ~3.6% in March 2022 and has since dropped to 2.3%.

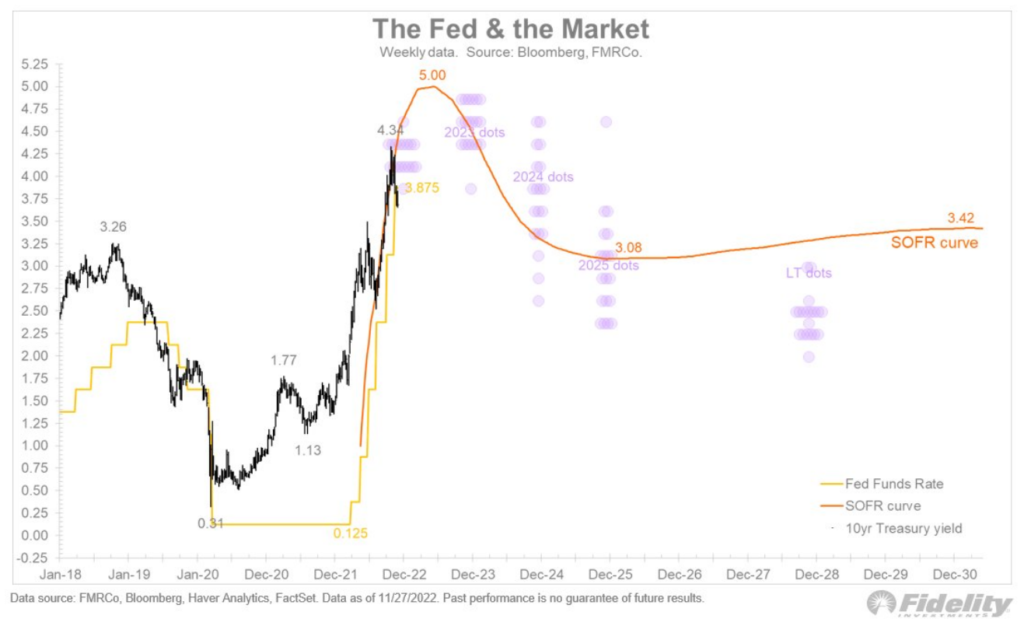

The SOFR (replaced LIBOR) forward curve that tracks expectations of the Fed Funds Rate also shows that the market sees lower inflation, allowing the Fed to cut rates soon it peaks ~5% in 1H2023. This is contrary to the Fed’s present narrative that rates will stay elevated for a prolonged period.

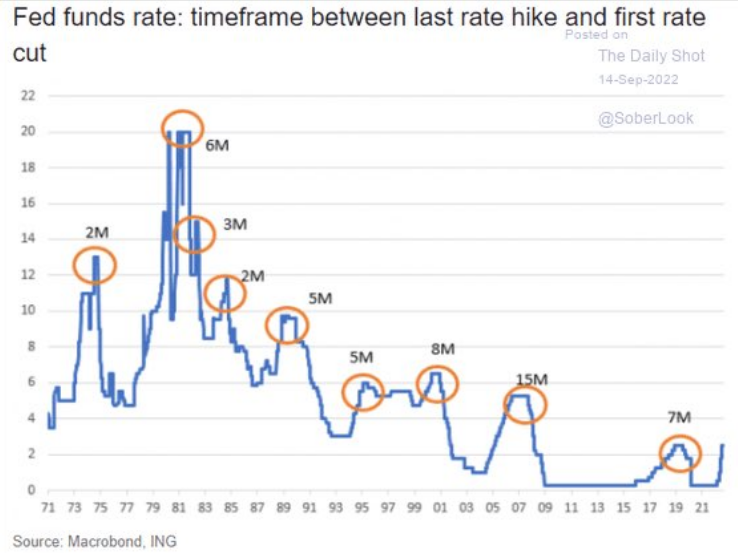

Pivot bulls will be aware that the Fed has not stayed very long at the terminal rate, as the chart below illustrates. However, the last time CPI got to the 8% range, interest rates were far more restrictive in the 1970s and 1980s. It’ll be a heck of a challenge to get inflation down to the Fed’s 2% target with real rates still negative and consumer spending strong.

Where does the decline come from?

Let’s evaluate the potential areas that need to improve for bond markets to be accurate.

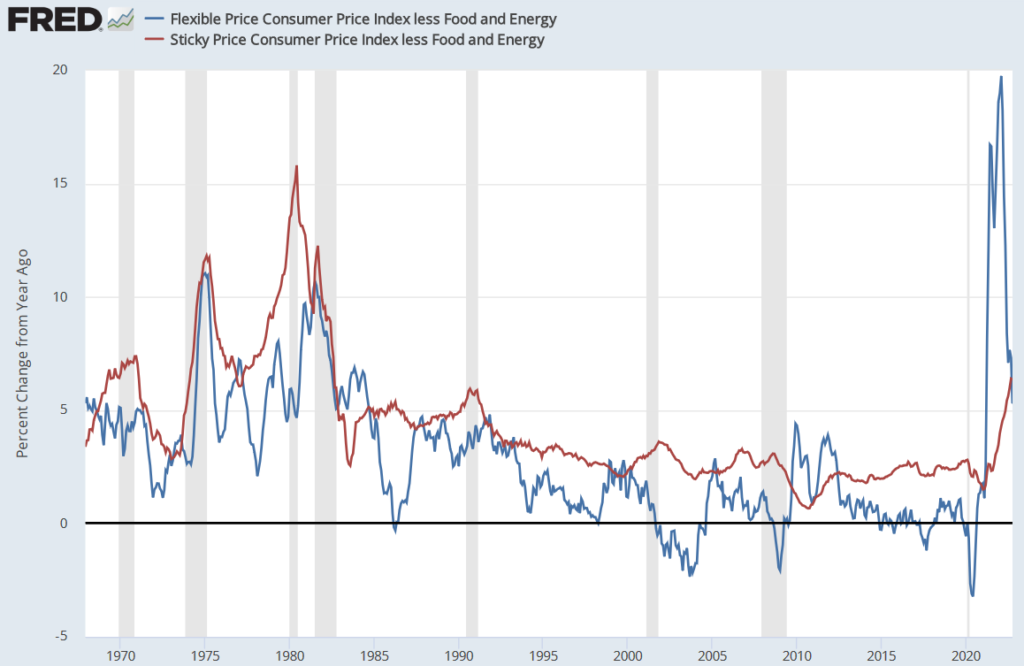

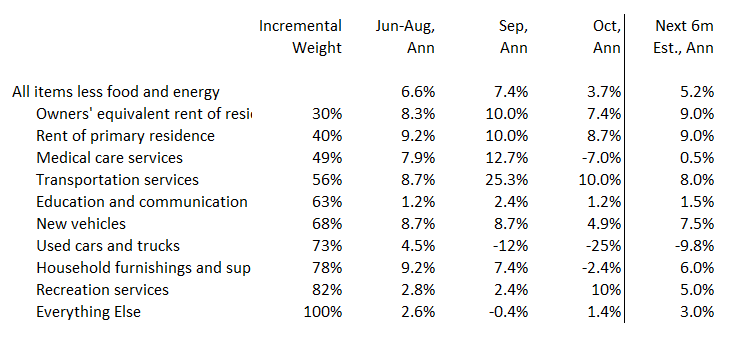

The sticky price CPI index published by the Atlanta Fed provides a picture of disinflation in 2022. The declines have been driven entirely by items with flexible prices while sticky prices remain elevated. It is probably premature to think we will see inflation drop to the Fed’s target level without seeing a meaningful decrease in sticky CPI. That, in turn, will require weakness in jobs that feeds into wages (further discussed at the bottom) and eventually to sticky service prices.

If we get even more granular, we can use the chart above to see that the biggest contributors to the October inflation deceleration was medical care services and used cars/trucks. When we look at used vehicle prices, we see they are coming down at a rapid 25% annualized rate. This seems unlikely to continue — at least not at its current pace. This means that for inflation to continue to dissipate at September’s pace, it will have to come from somewhere else and most likely one of the sticky sectors we discussed earlier.

Jobs data looks robust on the surface

Since workers are the largest cost for the sticky services categories, the market is likely to focus on wages and jobs as a leading inflation indicators. This week, Jay Powell said as much, and the strong non-farm payrolls report brought the subject into focus. Let’s drill beneath the headline data because government statistics are massaged heavily, which can distort the true trends.

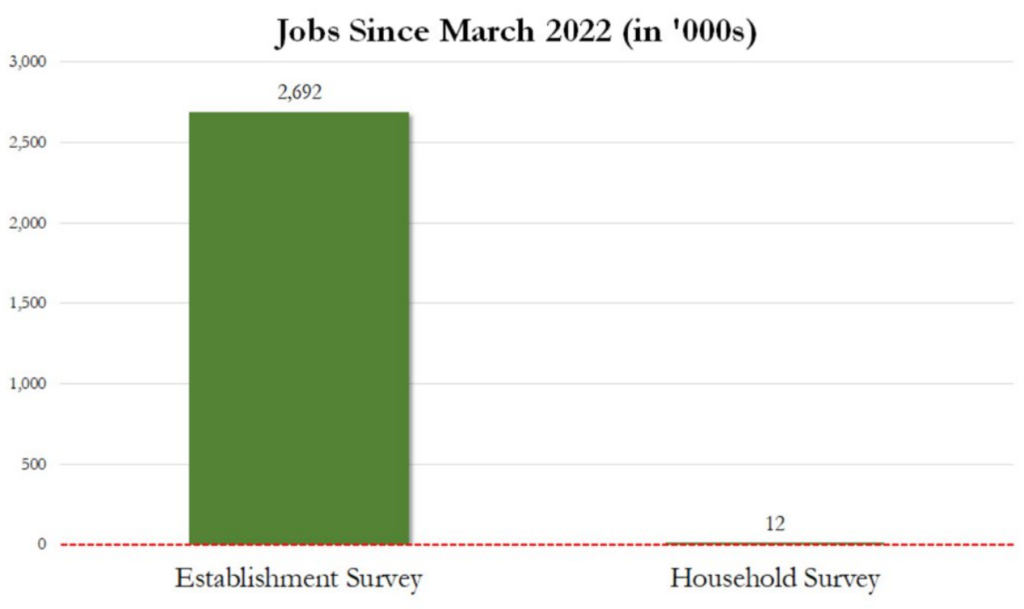

There’s a widening gap between the company survey (called establishment survey) and the household survey, which is the source of non-farm payrolls data. One source of divergence could come from the household survey counting one person holding two jobs as one employed person, whereas the establishment survey counts two. That divergence has been large in 2022, as shown below.

Statistical adjustments are distorting data

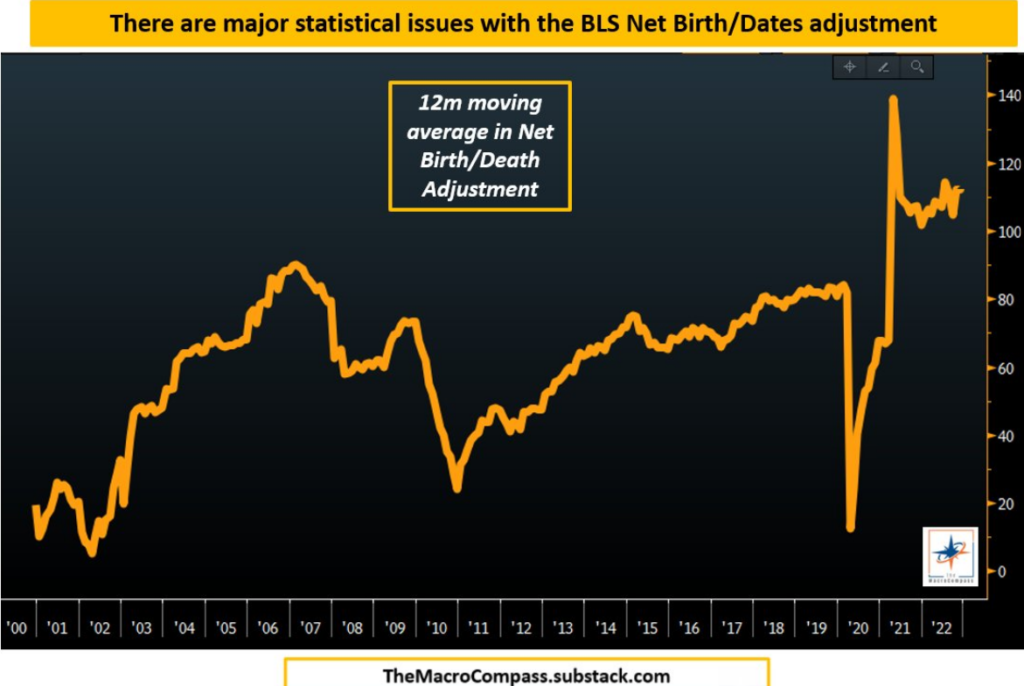

Another source of divergence comes from the government’s (BLS – Bureau of Labor Statistics) statistical adjustments. The BLS adjusts CPI for Hedonic Quality and we’ve highlighted the lags introduced by replacing home prices with OER in the CPI Index. For jobs, the BLS has introduced a birth/death model that tries to adjust for the creation and closure of companies. Those adjustments have jumped higher after Covid. We are open to the idea that these adjustments are distorting the true trend.

Sidebar: This is how bureaucracies become more powerful. Instead of collecting data and reporting it, they start making adjustments to “improve data quality”. Fast forward many years, and you need more than 1,000 economists. Your tax dollars at work!

Watch the NFIB data

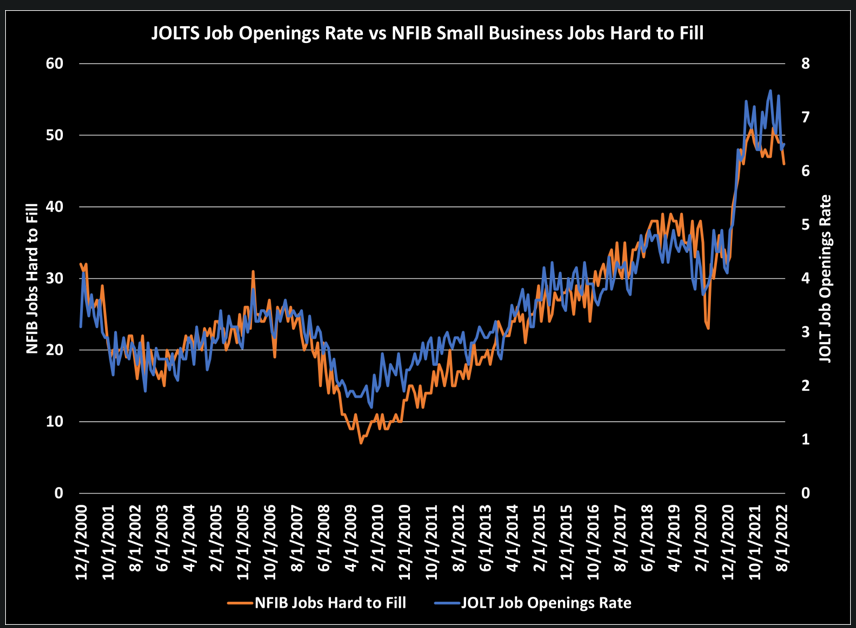

One of our research services, Tier-1 Alpha provides a more granular look at the distortion in the data. The National Federation of Independent Business (NFIB – aka small business) published a jobs survey. The Jobs Hard to Fill index is tightly correlated to the BLS’ JOLT job opening rate. The NFIB data softened this fall, but JOLTS job opening jumped back up in September.

The divergence was more evident when Tier-1 drilled into the data. They discovered that many of the openings were statistical adjustments driven by the birth/death model.

In September, a significant portion of the job openings jump came from the construction sector due to the birth/death adjustment. The rise does not make intuitive sense because property sector activity has collapsed as higher rates bite.

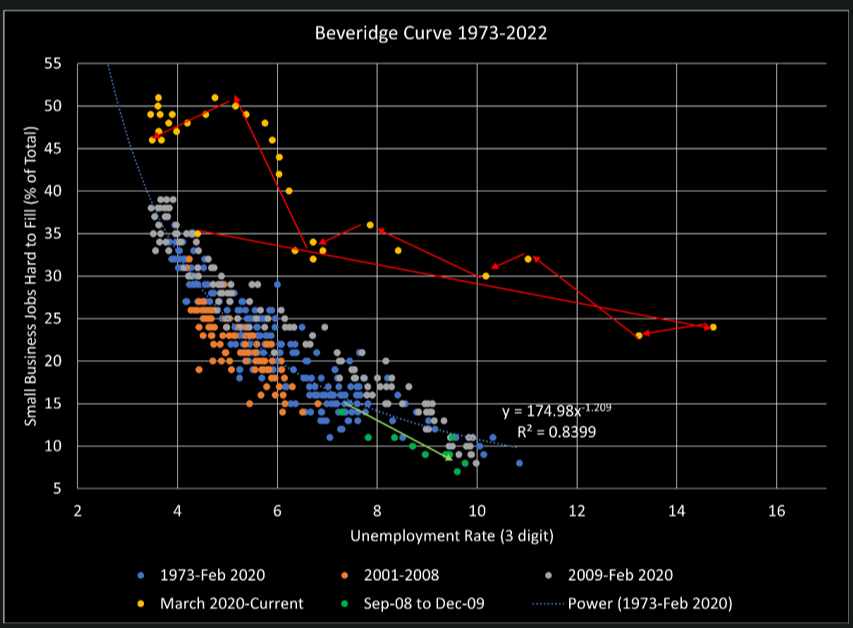

Tier-1 makes an astute observation that the NFIB Jobs Hard to Fill index needs to drop into the low 30s (Oct at 46%) before unemployment moves above 4%. As the chart below shows, the correlation between the NFIB index and the unemployment rate is a tight R2 of 0.84 over the 1973 to 2020 period. The post-Covid jobs surge has thrown the correlation into disarray (the yellow dots at the top of the chart).

We’ll be watching the NFIB data closely as the broader market gyrates to the heavily massaged government jobs data. This Friday, December 2nd, was a good example of this gyration. The October NFIB report is available here. This is further evidence that inflation dropping rapidly to the Fed’s 2% target will be a challenge.

The Yield Curve Points to Recessions

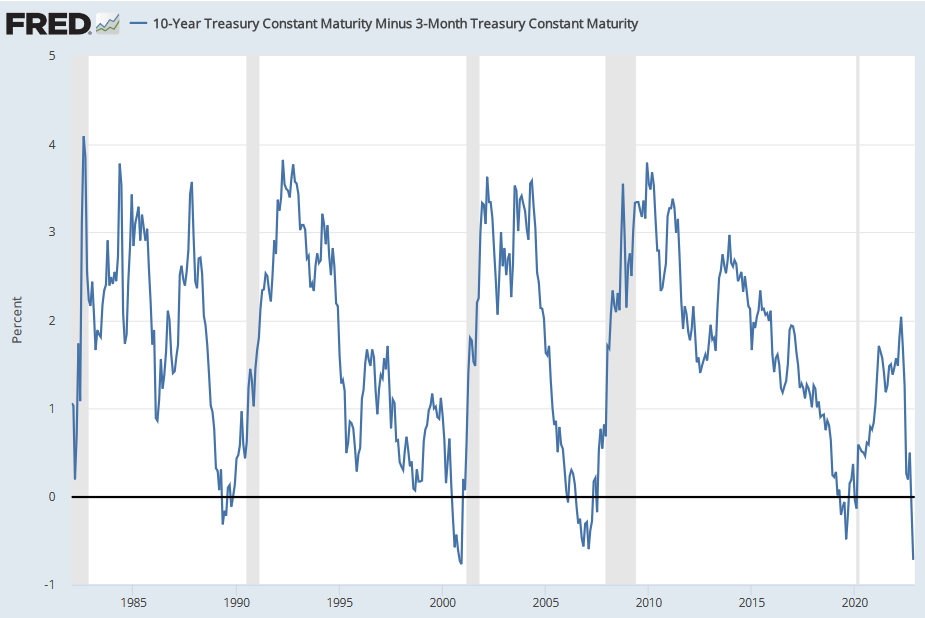

Finally, the yield curve has been terrific at sniffing out recessions, and there is no reason to suspect this time will be different. The 10-year to 3-month inversion is at a level that has reliably predicted recession in the past. A rapidly slowing economy will be a natural inflation dampener. It’s possible that this is what the bond market is sniffing out. While our main thesis is that core inflation will stay sticky, we are vigilant to that trend reversing if economic activity slows rapidly.

The inflation trajectory over the coming 6-12 months will significantly impact 2023 asset returns. If core CPI does not rapidly decelerate towards the Fed’s 2% target, rates will need to stay higher for longer, increasing recession risks. It’ll be a fine balancing act for both the Fed and markets. As we laid out last month (See Dispatch #19) we see more earnings downside, and the process has just started. For the moment, bad news is good news. We are positioning for a 2023 when bad news is indeed bad for markets.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |