We see a more balanced 2024 market outlook as the US economy has been resilient absorbing very high rates. Yes, the lagged impact of rates will continue to slow activity, but the consumer remains underleveraged and large companies have refinanced debt at low fixed rates. We are also conscious that we have never witnessed a post-pandemic economic cycle, which skews us to a more reactive, follow-the-data, approach, rather than a more proactive, predict the data approach. Let’s be honest, very few of us saw a pandemic coming, nor did we expect the Fed to print $6 trillion with a few months. The 2023 bank failures surprised most, as well. Forecast error could be high as we don’t know a prior playbook on how the economy will progress as we unwind the Covid stimulus.

That’s not to say we are flying blindly. We see the economy at the late stages of an up cycle rather than the start of a recovery. The bullish >11% 2024 earnings growth projection assumes an economic recovery, which leaves room for disappointment. On the bullish side, high levels of savings are invested in safe money markets, which leaves room for animal spirits to move capital up the risk spectrum. Cue the price action following the December 2023 Fed meeting. Furthermore, with the S&P up ~ 23% and bitcoin +150% year to date, some of those spirits have been unleashed already. This pushes us towards a diversified portfolio to reduce correlation to the economy. The range of outcomes is broad and the probability for each outcomes less certain.

We are also watching for signs of deeper problems. The US government and floating rate corporate borrowers are the most likely sources of unexpected trouble. The US is running a >7% fiscal deficit despite a strong economy. We’ve never done that previously, and funding that spending may pressure rates, as we already saw several times in 2023. We are also seeing credit conditions worsen among floating rate corporates and small businesses. In the near term, high deficits are stimulative, and the reserve currency allows the country to get further over the skis. An exact point of no return will be hard to time, but this risk is firmly in our asset allocation and risk management thinking.

The 2024 market outlook will cover the following:

- The robust consumer

- Rising delinquencies in floating rate debt

- Higher deficit and how this may impact bond yields

- Earnings expectations and positioning

- Housing and its impact on CPI

The robust consumer

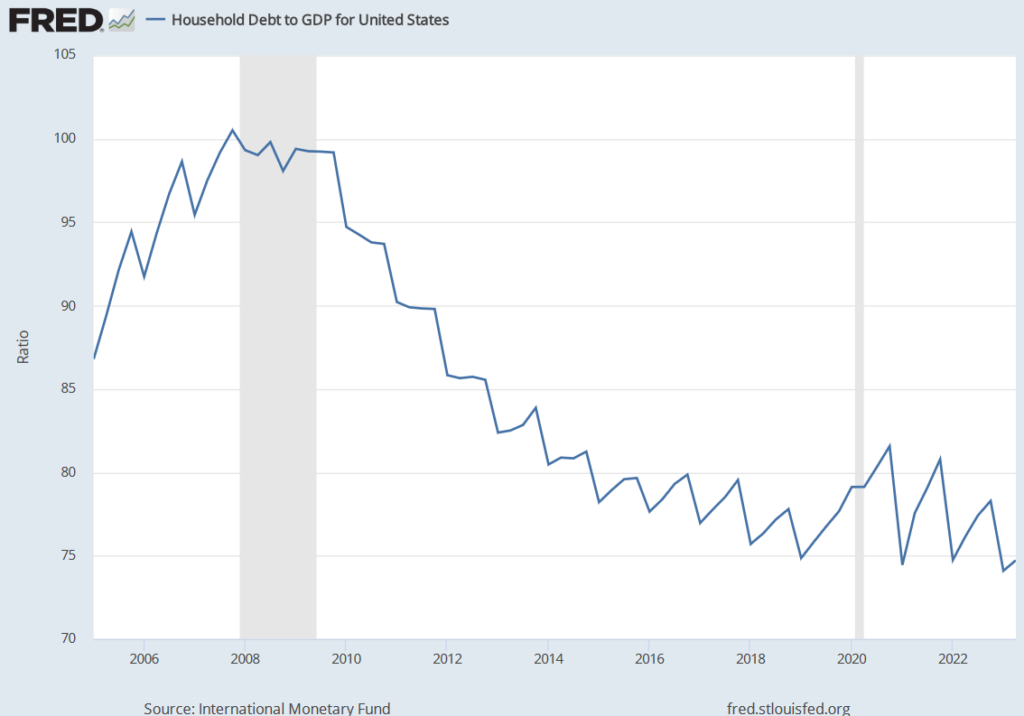

The consumer has lowered debt exposure since the 2008 global financial crisis (GFC).

Source: St Louis Federal Reserve

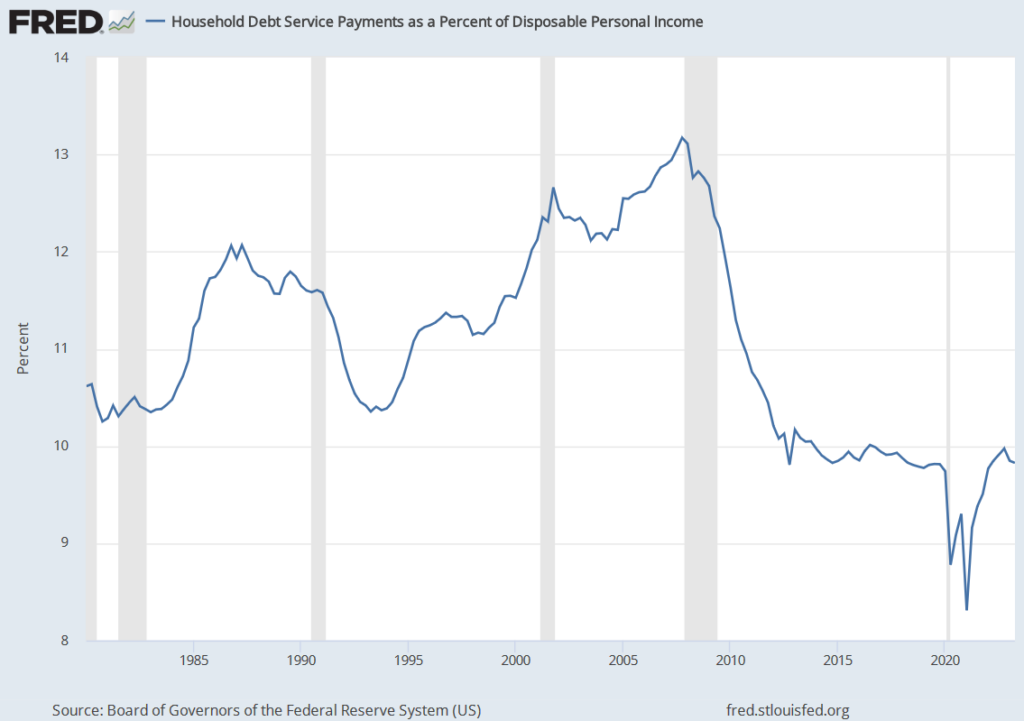

The amount of US household disposable income used to service debt has dropped sharply since the GFC because of low fixed-rate mortgages. Mortgages make up roughly 70% of $17.3tn consumer borrowing at the end of 3Q2023.

Source: St Louis Fed

But, non-mortgage interest costs are surging, which is what is likely causing the delinquency rise we highlight in the next section.

Don’t forget student loan payments started in October. The outlook for consumer spending should be tempered, which is at odds with 2024 earnings projects.

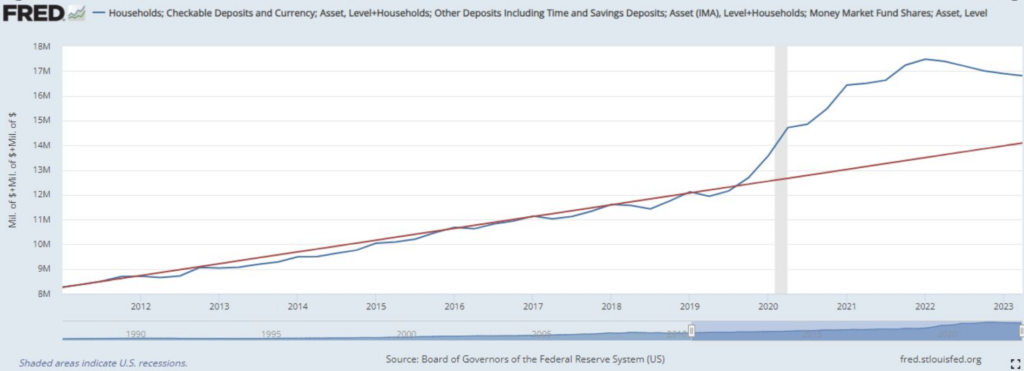

The second part of the robust consumer argument rests on high savings. The chart below shows that households’ liquid assets remain above long-run trend following the pandemic.

Source: Carson Group

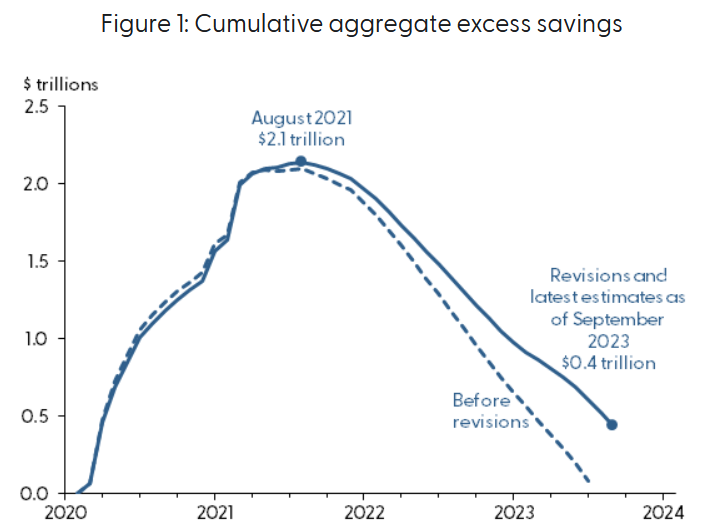

There’s little debate that most of that excess savings are with wealthy households where the marginal propensity to consume is low. For a majority of consumer, savings have already been depleted. The chart below shows the San Francisco Fed’s estimate of dwindling excess savings. The Fed adds, “Estimates of aggregate excess savings can be highly uncertain depending on both the methodology used and the assumptions made about the pre-pandemic trend. Moreover, further data revisions could materially alter our understanding of how households accumulate and spend savings.”

Rising delinquencies in floating rate debt

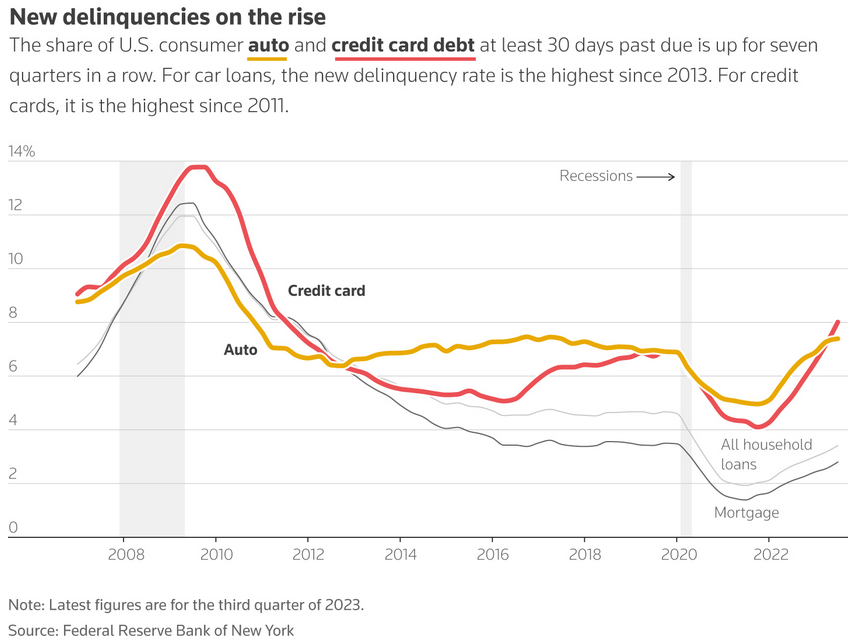

Despite the bullish talk above, there are signs of higher rates pinching some segments. Both auto and credit card payment quality has worsened to levels not seen in almost a decade.

Source: Reuters

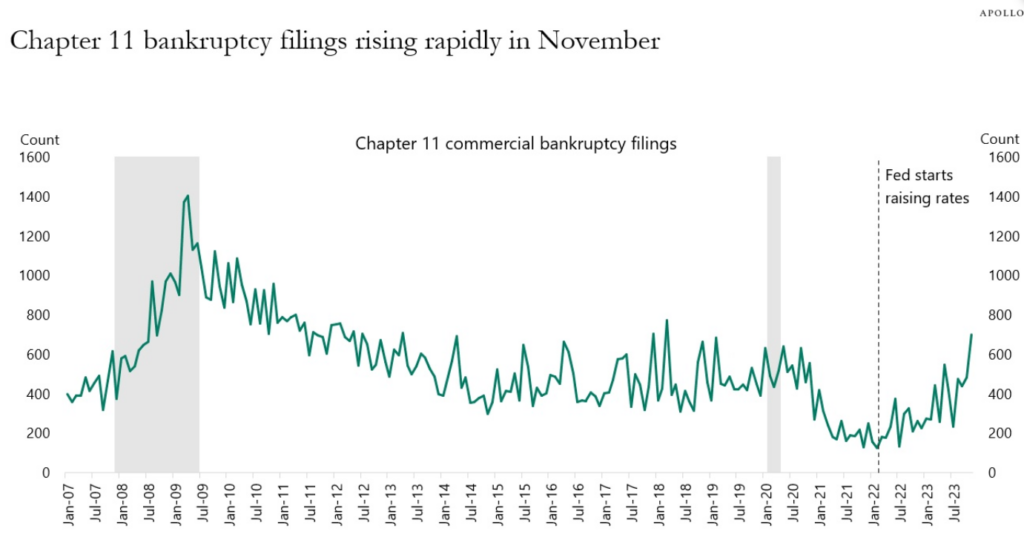

On the corporate front, bankruptcies have risen significantly and are now above pre-Covid levels. In the first nine months of 2023, small business filing rose 41% YoY & larger Chapter 11 filings rose 61% YoY according to American Bankruptcy Institute data.

Source: Apollo Global

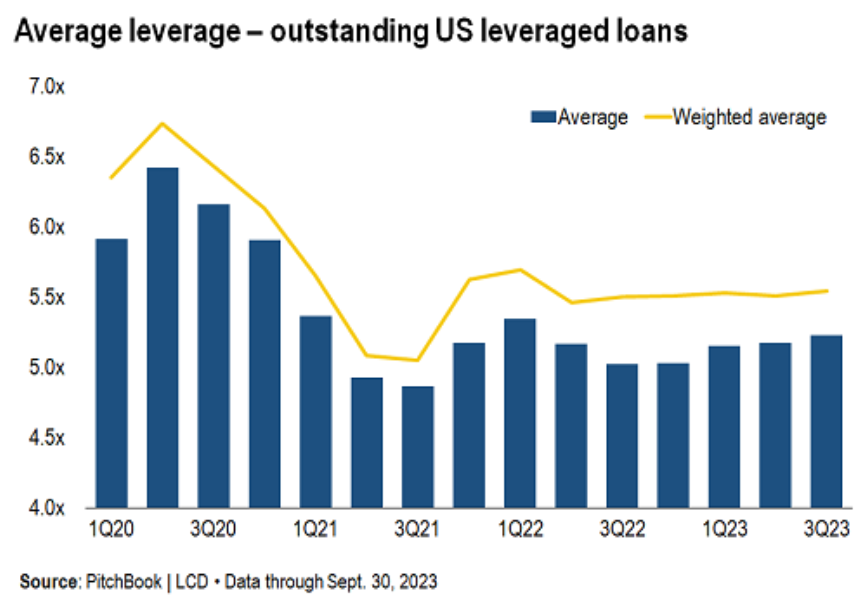

Leveraged Loan trends are softening.

Companies too small or with too much debt to access the bond market, are at the highest risk. There has been an explosion of floating rate debt issued in the private markets over the past decade. The financial media refers to this segment as “shadow banking” because there’s little oversight, capital rules and visibility, unlike banks, for the lending entities.

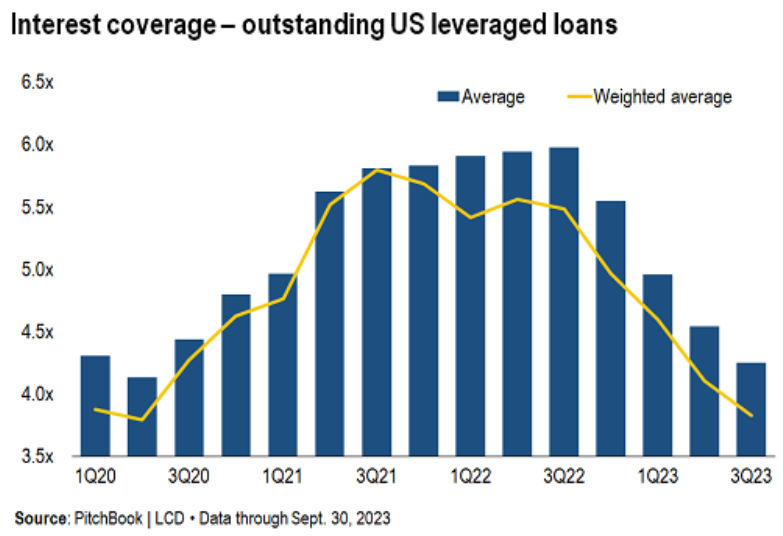

Credit quality in this segment is deteriorating, and some measures are down to Covid lows. This is worrying.

Source: Pitchbook

In a slightly more favorable trend, overall leverage of this cohort has worsened more modestly. It is back to pre-Covid level and well off the peaks seen during the brief Covid downturn.

We probably want to pay more attention to interest coverage for floating rate borrowers than overall leverage. For any given amount of borrowing (aka leverage), the interest burden today will be much higher than in 2019.

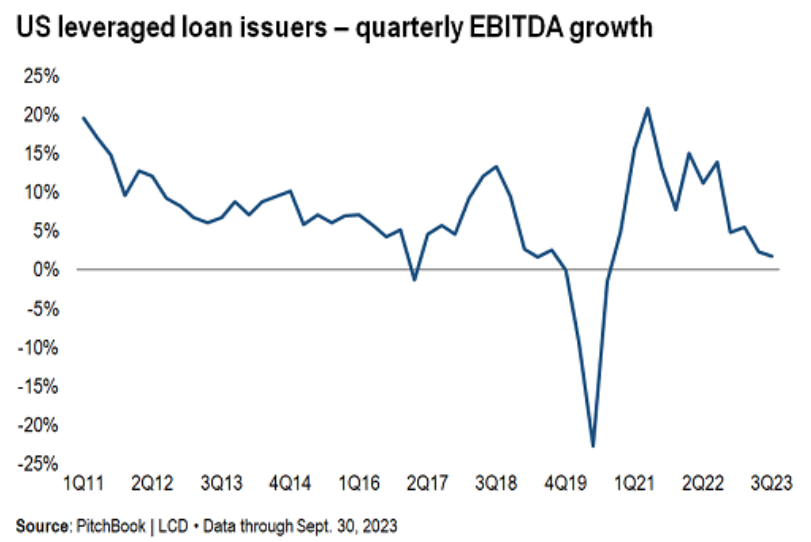

These borrowers will be helped by Fed rate cuts. However, if a faster than anticipated economic slowdown drives the Fed rate cuts, then the net impact will be harder to gauge. Cashflow (EBITDA accounting shown) growth has already slowed sharply, even before we enter an official slowdown.

The positive spin is that these trends reflect “normalizing” and the cautious view is “trouble ahead”. We skew to the middle that the consumer remains strong, but the marginal change is weaker. The consumer strength is offset by a more heavily indebted corporate sector and a government facing a historic high debt burden.

Deficits Stimulate until they can’t!

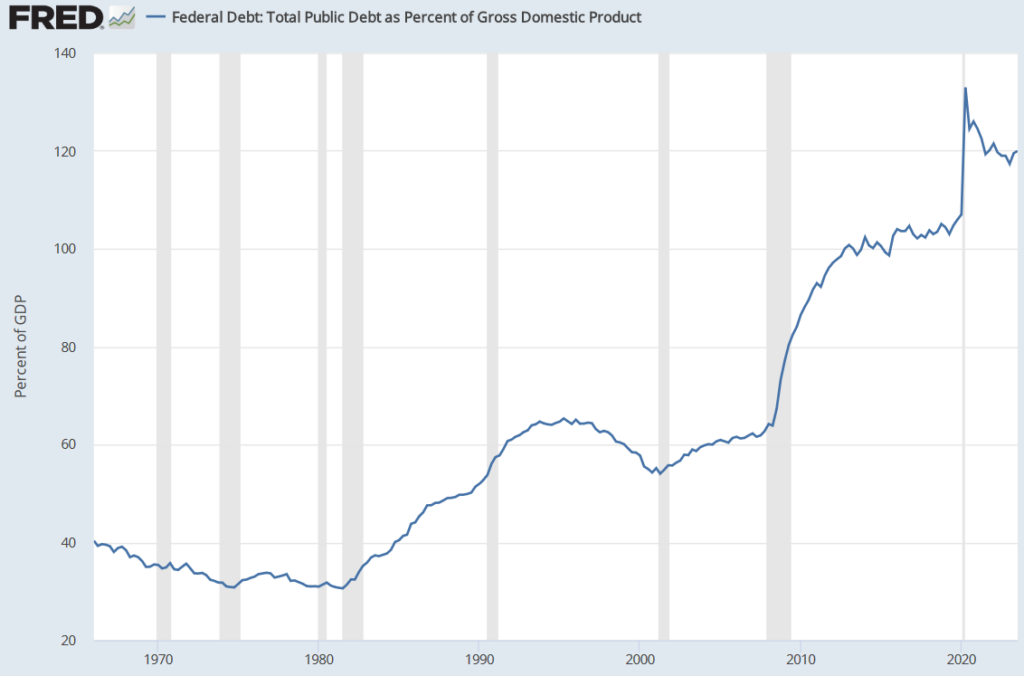

Most are aware that the US debt load is high in absolute terms and as a percentage of economic output (debt to GDP).

However, each dollar of deficit spending stimulates the economy. In fiscal 2024 (October 1, 2023, to September 30, 2024) the administration is projecting that it will spend ~ 36% more than it will receive from taxes. This translates to a 6.8% deficit to GDP ratio, which is unprecedented outside of a recession or pandemic. The actual 2023 deficit was even larger, and this Bloomberg article breaks down the increase from the year prior.

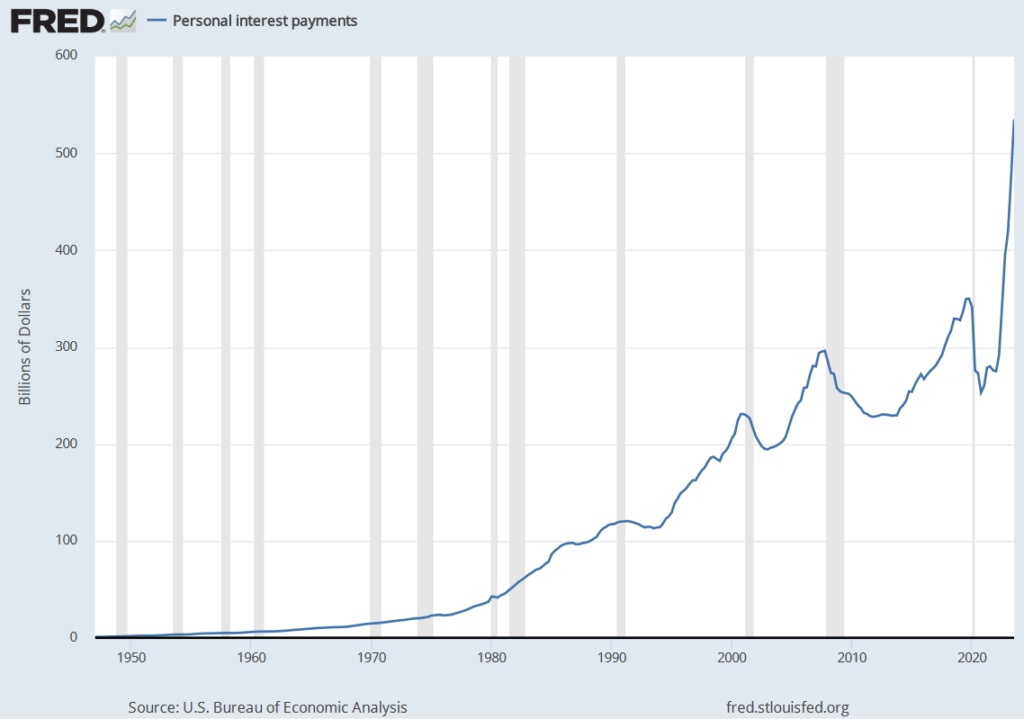

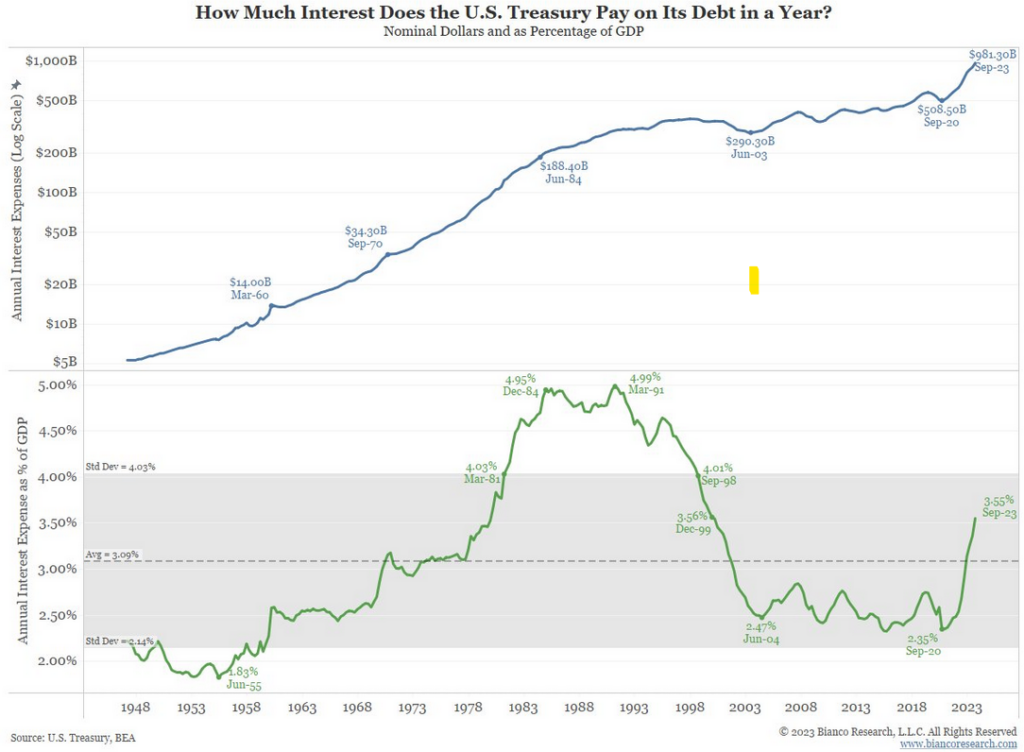

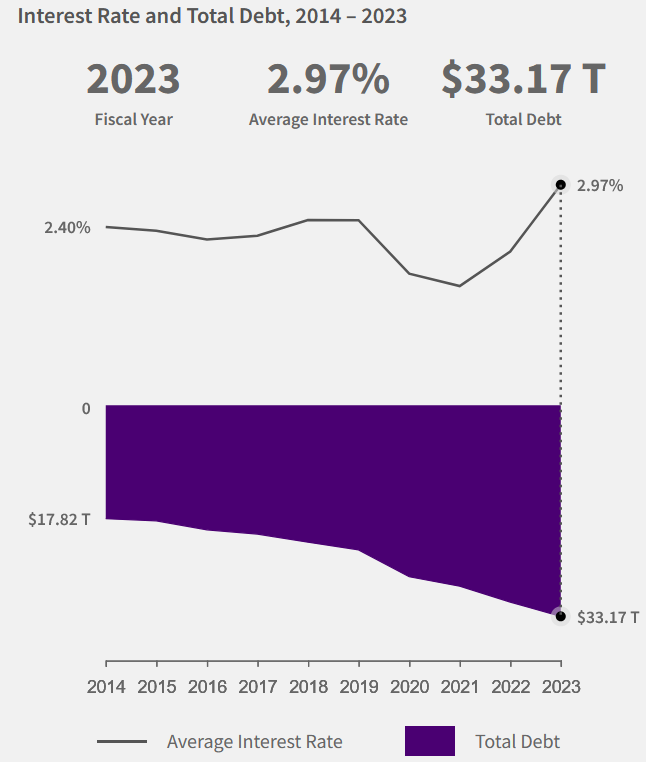

Interest payments are spiking because of the sustained deficit spending and higher rates.

Source: Bianco Research

The US government, unlike consumers and large companies, did not (couldn’t really) refinance its debt during the post-Covid zero-rate environment. You can see the rise in the average interest rate, which will continue in 2024.

In addition to issuing roughly $2tn of new debt to fund the deficit, the US will have to refinance a large amount of maturing debt. In 2024, the interest bill will be over $1tn, which is more than 20% of all US government revenue. This is not a sustainable trend.

Source: Apollo Global

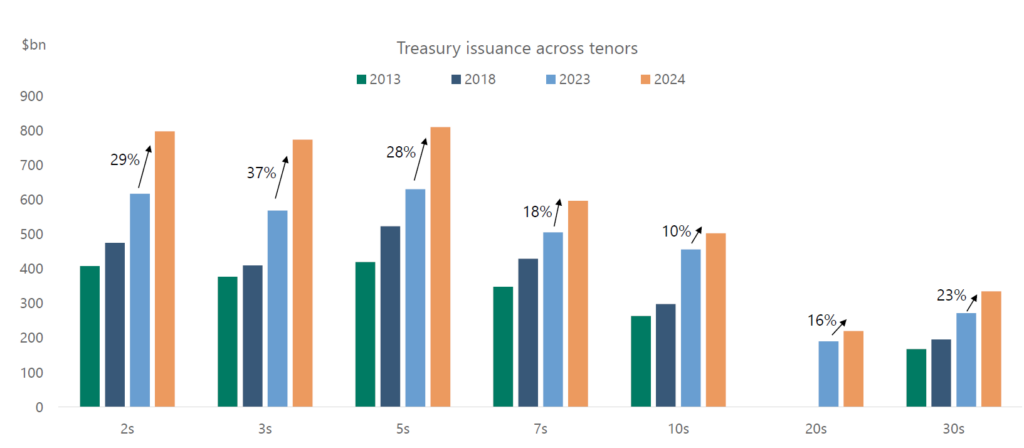

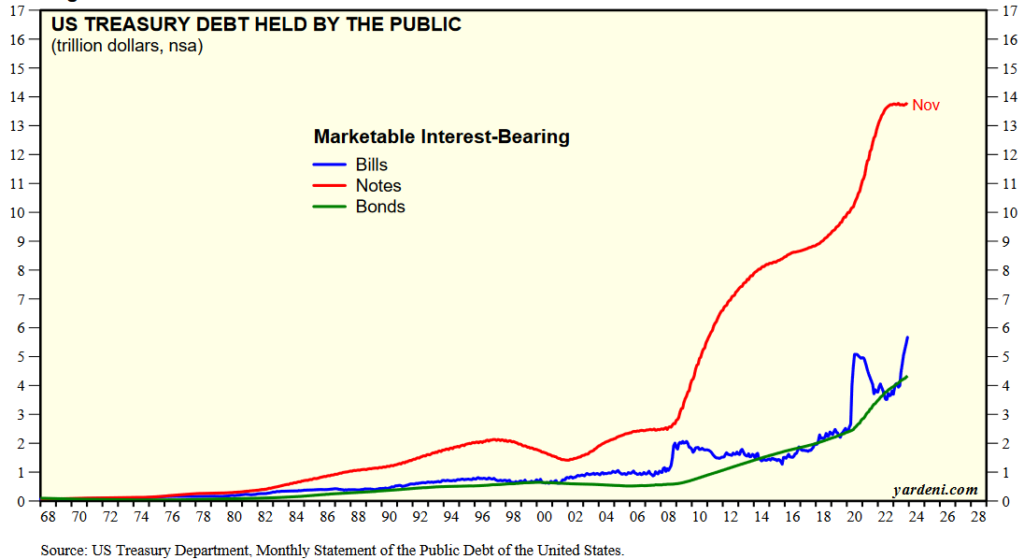

For the moment, the Treasury has decided to issue more short-term T-bills to fund the deficit, which has alleviated the pressure on long-term interest rates. This is because funds that owned the $1tn worth of Reverse Repo in November could invest directly in T-bills.

Source: Yardeni Research

Note: Bills mature in 12 months or less, Notes are securities that mature in 1 year to under 20 years and Bonds mature in 20 or more years.

We anticipate that 2024 could bring additional bond market volatility as the Treasury reverts to a normalized mix of securities issuance alongside rising issuance schedule. We remain convinced that Congress will not trim spending or raise taxes. The path of least resistance will be for Fed action to lower interest costs, which underpins our favorable view of precious metals and digital assets to hedge real-retirement income.

For the moment, market participants are giddy that the Fed is thinking about cutting rates. Markets are pricing 6 cuts (1.5%) in 2024, which is unlikely if growth stays firm. This bond market view also contradicts stock earnings assumptions as discussed below.

Earnings expectations and investor positioning

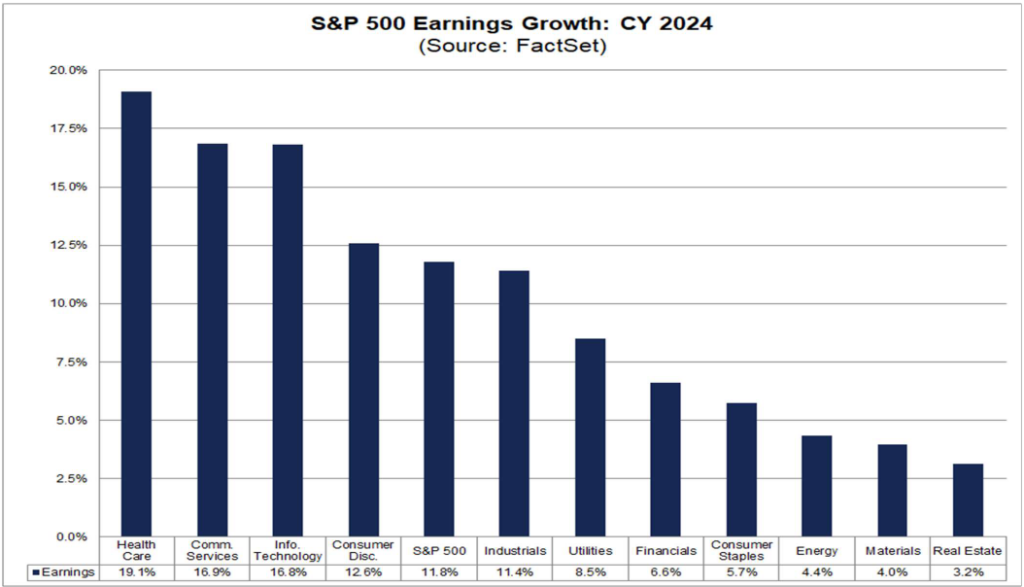

Wall Street is already projecting rapid earnings growth, which is one of the key risks to 2024 market outlook. After no growth in 2023, S&P 500 earnings are estimated to rise 11.8% in 2024. With nominal GDP set to drop (simply due to lower inflation), we see this aggressive set up as a market risk. Markets move on changes to expectations and not merely by hitting them.

Source: Factset

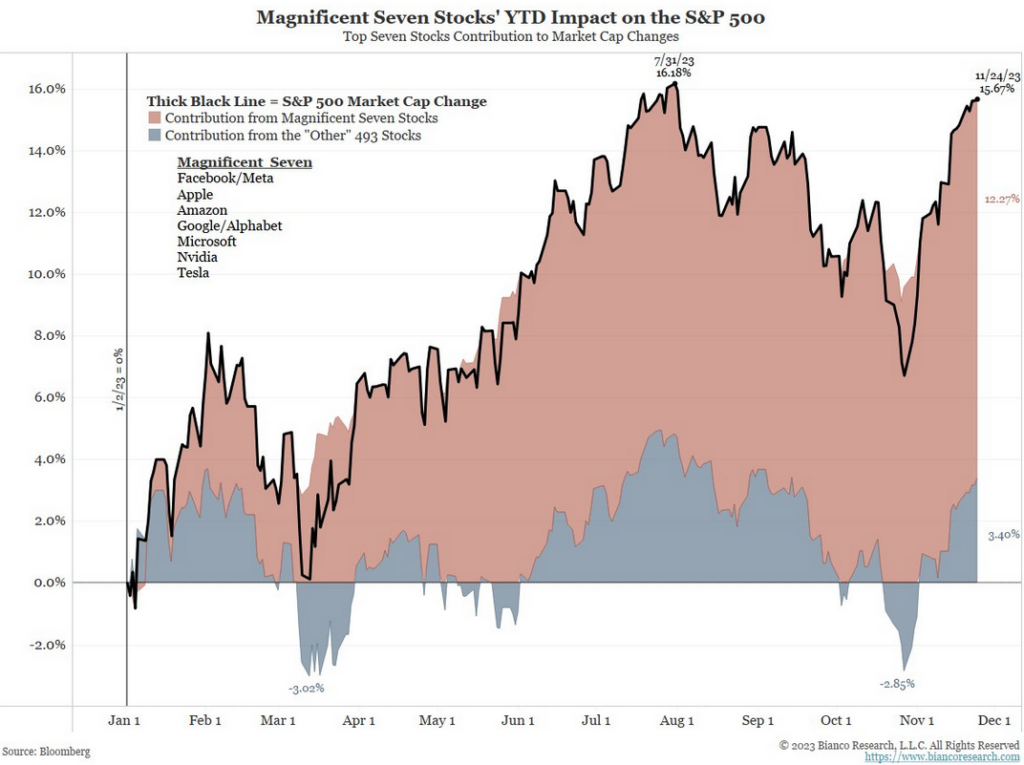

Most market participants are aware of the extremely narrow stock performance in 2023. This is rarely a good sign. This chart from Bianco Research conveys the story well. In this type of market environment, a well-diversified lower-risk portfolio will inevitably underperform headline stock performance.

Source: Bianco Research. Chart show Year to Nov 24th

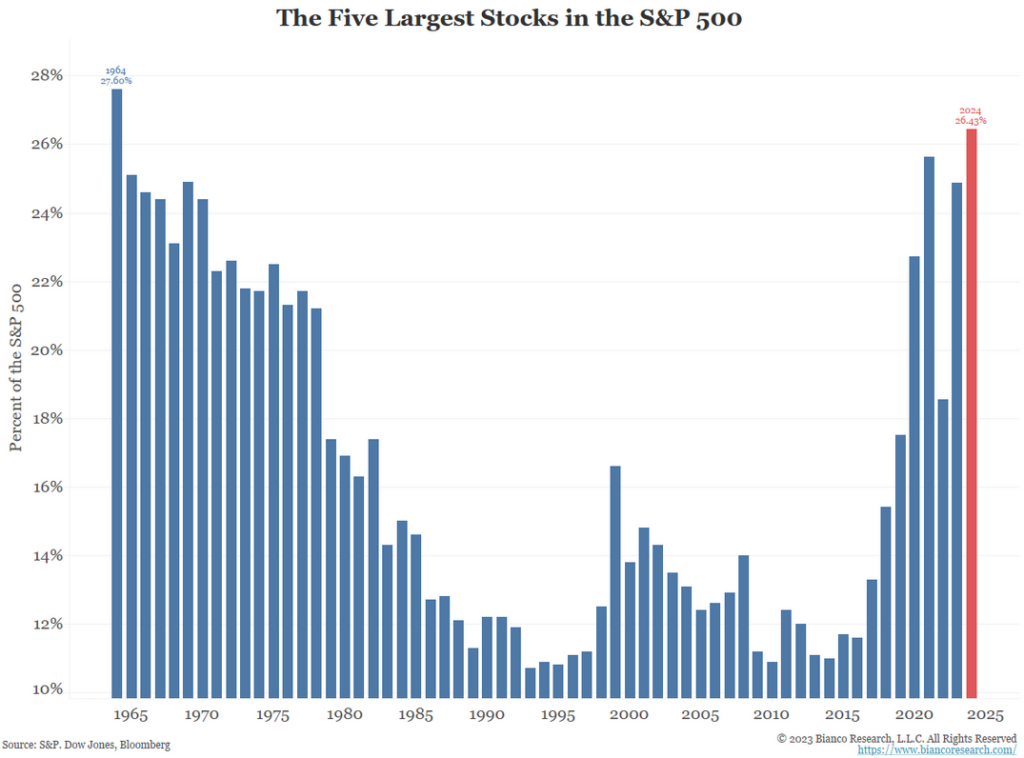

Top-5 stocks hitting levels from where prior darlings did poorly.

Source: Bianco Research

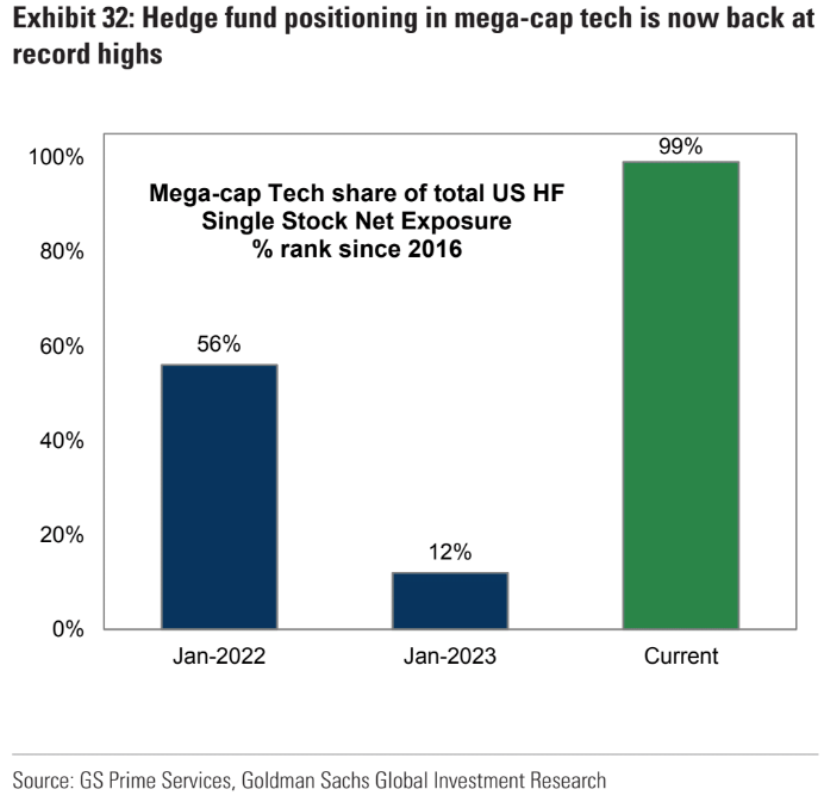

It is no surprise that positioning in megacap tech is high.

The same goes for technology stocks overall.

Source: Market Sentiment

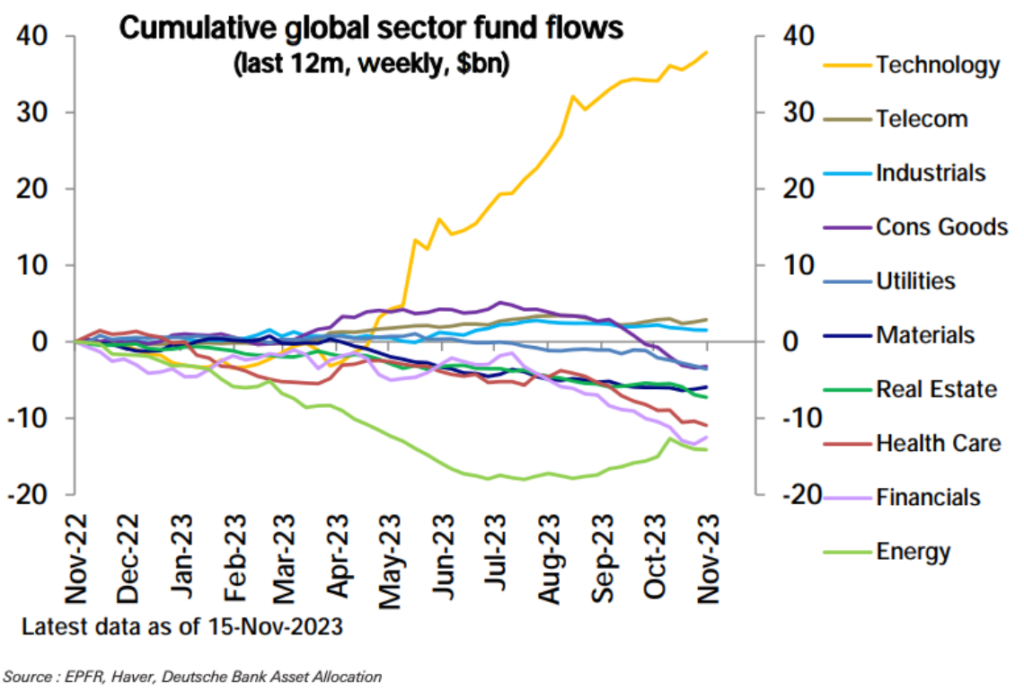

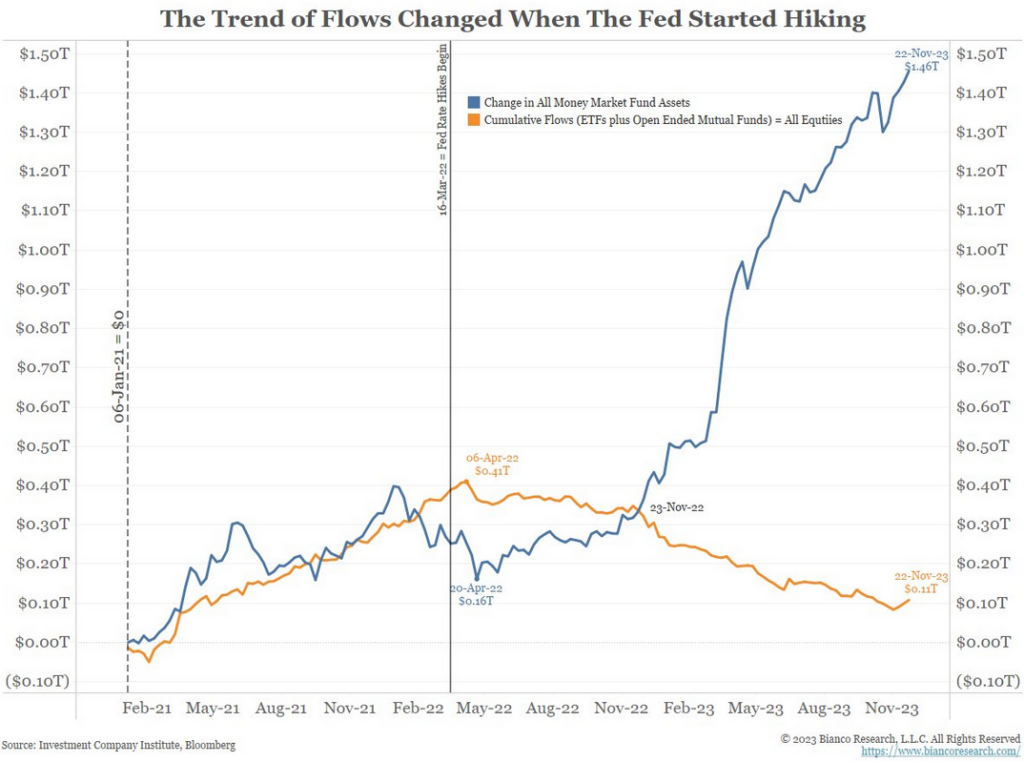

The flow-skew adds up, given soft inflows into the overall equity asset class.

Source: Bianco Research

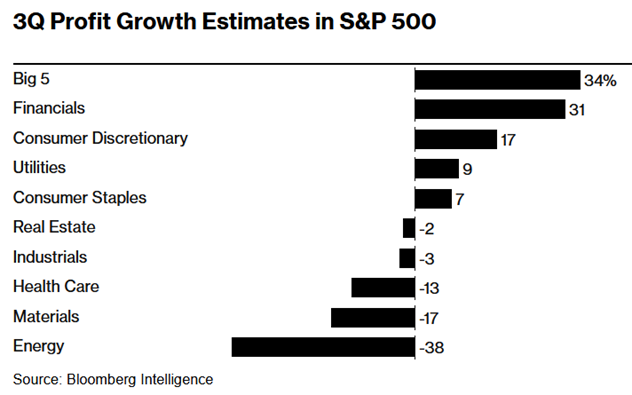

But, lets give the Magnificent-5 credit, as they have knocked 2023 earnings out of the park.

Many of the S&P 7 Mega caps have net cash and have benefited from higher rates. However, we should not be valuing earnings from interest at the same 40-50x multiple of core earnings. For the moment, all earnings might be valued equally.

We do agree that these large cap tech firms can easily absorb a modest economic slowdown without undue earnings pressure. We continue to maintain exposure via diversified indices.

Housing and its impact on inflation

The ease and speed of getting core inflation down to the Fed’s 2% target will be a key factor in determining economic activity and the 2024 market outlook. Housing in the form of rents accounts for over 40% of the core CPI basket. It is an overly complicated calculation, and you can read more about the Owner’s Equivalent Rent calculation.

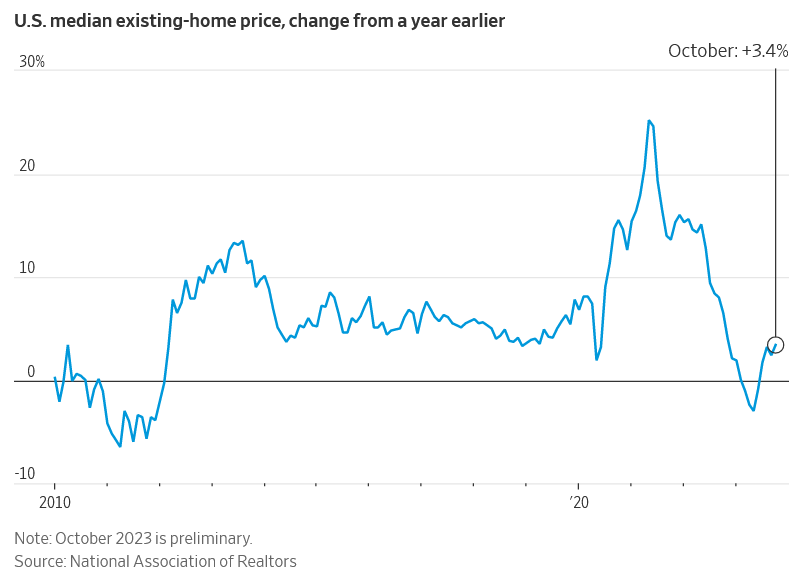

The basic idea is that the rents collected via a survey are equivalent to homes that are owner occupied. But existing home prices have been rising for several months now, so if equivalence holds, then “rent” price should rise in the future.

Source: WSJ

There is lots of debate in the market whether rising multi-family rental unit supply will swamp the impact of higher single-family prices. The bond market is clearly betting on the former effect as it is pricing six rates cuts in 2024.

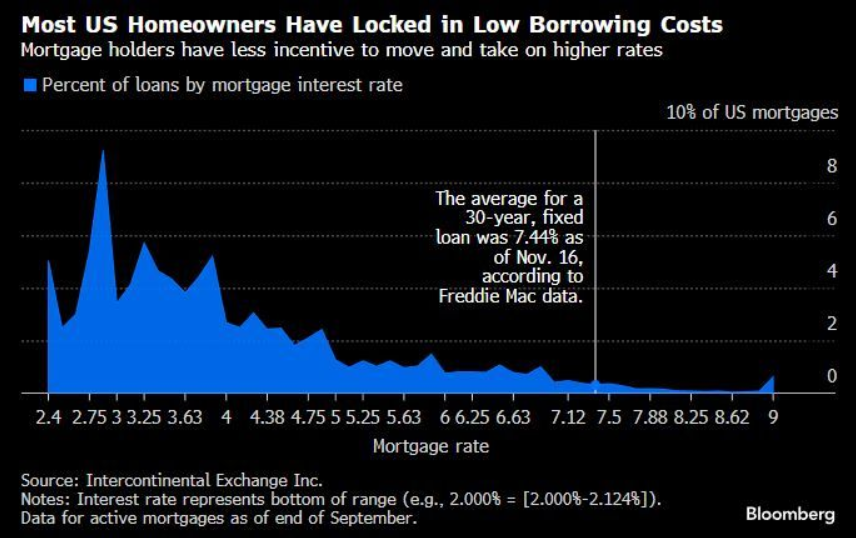

Lack of existing home inventory is a key factor behind rising price. Inventory is down because owners are tied to their existing low fixed-rate mortgages.

Households have locked in very low rates and won’t be willing to move because of payment shocks. This is all well as the economy stays robust, but could change if job losses accelerate. In any event, the consumer is the least of the worries and remains the most robust part of the economy. Too bad your government and leveraged corporates couldn’t do the same.

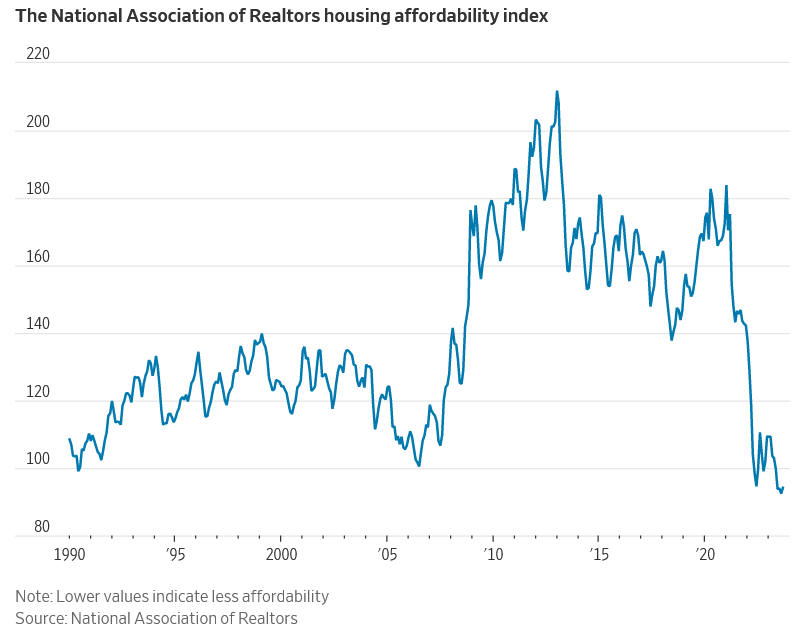

Rising prices and higher mortgage rates have crushed affordability, which sits at three-decade lows.

Source: WSJ

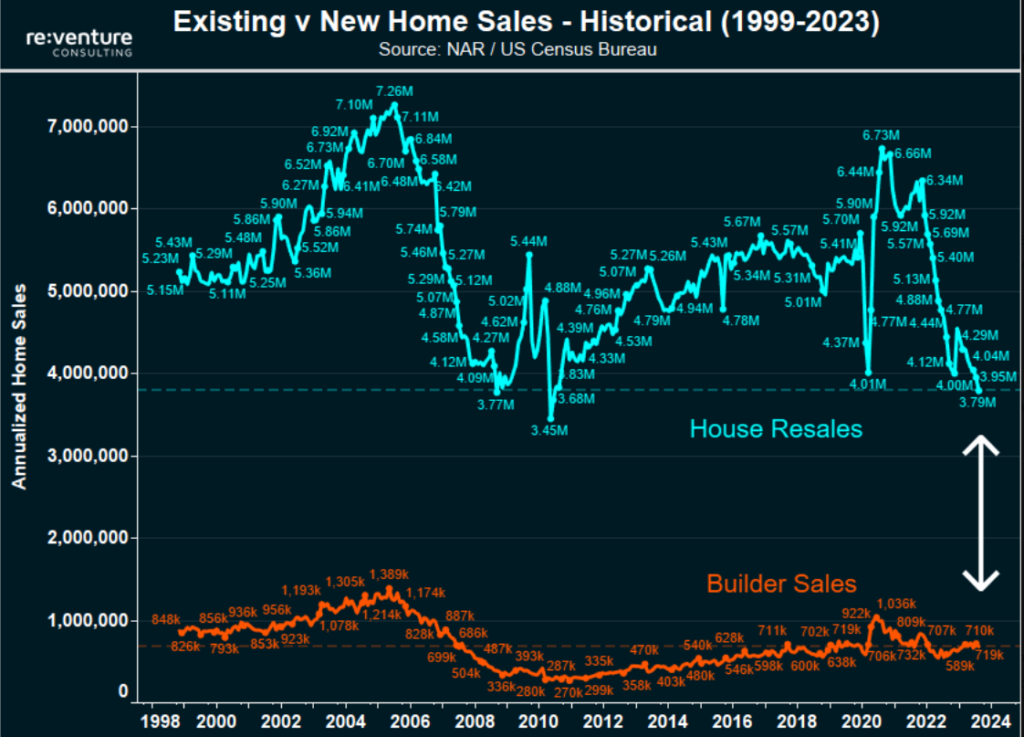

It is no surprise that sales activity has plummeted.

Source: Reventure Consulting

2024 market outlook conclusion

Today, the 2024 market outlook is mixed because stock and bond markets are pricing somewhat opposing outcomes, in our view. Stocks are pricing high growth, while bond yields have fallen in anticipation of rate cuts. Those rate cuts will only be possible if growth is soft, which support easing inflation. It is rare to see inflation falling when growth is accelerating. That’s betting on a unicorn sighting!

Given the uncertainty we will continue to employ buffered strategies and optionality to express upside exposure. We also continue to seek assets uncorrelated to economic activity. We think Uranium, which we continue to like even after the sharp run up, and carbon credit (ETS) despite a weak 2023, continue to offer such exposure.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |