Dispatch #6 shares excerpts of our thoughts on the SEC vs. Coinbase lawsuit, and its implications for the broader ecosystem, from a letter to investors of the RockDen Digital Assets Fund last week. The document was finalized on June 16th, and some of the charts will be dated as a result. The Bitcoin price is meaningfully higher today than when the SEC brought its suits against industry giants Binance and Coinbase. We think the market has spoken on the impact of the SEC’s action upon the broader crypto asset class.

Last week also brought the news that BlackRock has filed to launch a spot Bitcoin ETF. This led Wisdom Tree, Invesco and Bitwise, who had previously filed applications that were rejected or expired, to re-file to launch bitcoin ETFs. This Decrypt article provides more background. Finally, a consortium of Citadel Securities, Fidelity and Schwab announced the official launch of EDX Markets, an institutional crypto exchange. This further illustrates mainstream finance’s embrace of digital asset and the ineffectiveness of the SEC’s regulatory enforcement actions. If you think that bitcoin and the broader crypt ecosystem have no staying power, the announcements this week may warrant a reevauation. That said, we’d bet that the SEC does not approve any bitcoin ETFs in 2023 and that EDX markets see limited activity!

Following are the excerpts letter to RockDen Digital Asset Fund investors.

Markets have mostly shrugged off the SEC vs. Coinbase litigation

The recent SEC vs. Coinbase lawsuits, while not a surprise to us, is another headwind for digital assets. The US has the largest pool of capital and the SEC’s actions will limit the number of venues offering access as many exchanges leave the US and others de-list tokens that the SEC deems “securities”. However, we were not surprised by the action as the SEC had already filed a Wells notice against Coinbase, indicating charges were forthcoming. The legal action is disappointing because the SEC had vetted the Coinbase IPO in 2021 and the core business model – crypto exchange – has not changed since.

The market appears to be taking – correctly in our view – a divergent view. The Bitcoin and Ethereum prices have remained essentially unchanged since the SEC announcement, whereas tokens deemed “securities” by the SEC have been impacted sharply. The sharper weakness, in our view, is due primarily to liquidity collapsing as US based firms have pulled market-making activity for these tokens. Many exchanges, although not Coinbase, have announced plans to de-list those tokens. Our discussion below will focus almost entirely on Coinbase, as we address how and if SEC charges impact our outlook on the asset class and our use of Coinbase as a trading/custody venue.

Crypto “securities” have been hit hard since the SEC lawsuits against Binance & Coinbase

Source: TradingView on June 16th, 2023

We continue to view Coinbase as the safest and strongest centralized crypto exchange. Coinbase is publicly listed (SEC oversight, hmmm!), audited by a big 3 accounting firm and has several billion dollars of capital. Despite the SEC action, we see Coinbase as the best-of-breed centralized digital asset trading and custody offering. We are evaluating self-custody solutions as a downside contingency.

SEC approved the Coinbase IPO

All companies seeking a public listing must disclose financial data and business risks. The #1 risk to a company should be the business model, and in Coinbase’s case their business model (securities exchange) is overseen by the SEC. The SEC approved the Coinbase business model ahead of the April 2021 IPO, but now says that Coinbase is an illegal unregistered exchange. This is stated prominently on the SEC release, as shown below.

We bet the SEC will claim that approval of IPO does not preclude the current lawsuit. But, if Coinbase was an illegal exchange, and exchanges are overseen by the SEC, why was the IPO approved? Where is the investor protection (The SEC mandate) for consumers who have purchased Coinbase shares since IPO? This WSJ article offers both side of the argument.

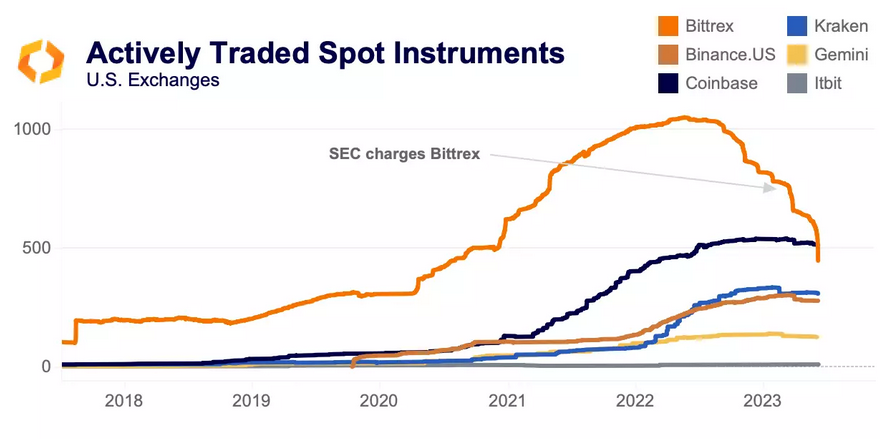

The SEC’s additional allegations that some tokens available for trading are securities and staking service is a security, may have more weight. There are many more tokens traded on Coinbase today than at IPO.

Source: Kaiko Research

Like Coinbase, we are looking forward to regulatory clarity on digital assets. Here’s Coinbase CEO Armstrong via Twitter articulating the current regulatory uncertainty.

Source: CEO Armstrong via Twitter

SEC Chair Gary Gensler has repeated that the current laws are clear and that crypto has failed to come into compliance. He repeated those same points during this interview with Bloomberg following the lawsuits.

Court verdict could take years

We expect the courts to decide the outcome, which should take many years. The SEC case against Ripple (the issuer of the XRP token/blockchain), which was filed in December 2020, will provide some clues regarding prevailing winds in the courts. The Ripple case will be important, as this crypto lawyer lays out in a thread.

In a more recent case, the judge overseeing the Voyager Digital bankruptcy case was critical of the SEC’s objections to a sale based on SEC speculation that some tokens might be securities. The courts have pushed back against the SEC’s broad interpretation in the handful of cases that are ongoing. These more advanced cases should provide plenty of insights into the direction US courts will take when it comes to the SEC’s assertions and the crypto industry’s pushback that regulations are opaque.

Securities to start, but something else later?

We agree that many protocol tokens have security-like features at the onset. Blockchains are generally launched by a person or a group who then raise capital via token sales at many points. With our tradifi background, it’s hard to argue otherwise. However, once a protocol is mature (which can take anywhere from a few months to a few years), the running of that open-sourced software code is handed over to the community. At this point, the Howey Test to determine if a token is an investment contract (aka security) becomes more opaque. A decentralized blockchain protocol has no management, articles of association, and shareholders aren’t a liability of the company. There is simply no contract at all between a decentralized blockchain and token holders. The entire functioning of the blockchain is in the code, and the community at large can decide governance.

We’ll be watching how the courts make this nuanced judgement. Will judges be up to speed on blockchain protocols to properly adjudicate the issues? The bankrupty judges have a narrow task but the judge presiding over the Ripple case seems to be on top of the technology nuances. Bloomberg columnist Matt Levine’s recent article does an excellent job of sifting through the complicated debate between securities and crypto.

Congressional legislation can remove the uncertainty

All of this uncertainty can be removed if Congress provides some clarity to crypto assets. The key issue we see is that most protocols start as securities (investment contracts), but then evolve into something else – commodities perhaps. The initial token sale from builder to investor has an expectation of a common enterprise, but does the subsequent secondary sale have the same rights? Wait – there are no rights, no contract or agreement unlike a stock certificate or the contract between Mr. Howey and buyers of orange groves in the Howey case. Congressional legislation can regulate the initial token sales (securities) and allow a fully decentralized protocols to thrive with less regulation. Several bipartisan proposals are attempting to provide this regulation, and we would be delighted to see consumer protection against initial coin offerings and the subsequent sale from VC insiders to the broader investing public.

There has been a raft of crypto bills tabled in the past. Forbes says 35 crypto-focused bills were introduced in 2021! The Responsible Financial Innovation Act and Digital Commodities Consumer Protection Act were strong bipartisan efforts in 2022, but the FTX fraud scuttled all of the momentum. This Bipartisan Policy Center article provides background. The current push for crypto legislation appears to be very much a Republican-led effort, and we’ll be surprised by any meaningful Democratic support to turn it into law. In the meantime, crypto innovation will leave for jurisdictions like the EU, Dubai or Singapore that have clearer regulatory regimes, and US consumers will have less investment choice.

As we told fund investors, we are always happy to discuss, debate and educate on Digital Assets. Feel free to reach out.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |