We do not believe that the Fed expanding its balance sheet again will mirror the asset performance of 2020/21. The current expansion is to heal a wounded banking system scrambling for liquidity. This liquidity from the Fed will be used to repair balance sheets and has a very low probability of being loaned into the economy, which is the transmission mechanism into the real economy. Yes, it is technically QE (quantitative easing) , but not the QE of the past where the Fed created bank reserves (liquidity) into a healthy banking system and to underwrite federal stimulus checks. The events of the past week increases our confidence in a recessionary outcome as banks tighten lending further. We are evaluating already defensive client portfolios to incorporate our revised expectations.

Over the long term, expanding insurance and removing the stigma attached to borrowing from the Fed could have unintended consequences. Dispatch 3, though, will focus on explaining why we believe the current Fed balance sheet expansion won’t lead to bullish stock price outcomes similar to 2020/21. We will address the bullish reaction of gold and crypto in a separate post.

RockDen Dispatch #3 of 2023 was completed on March 17th.

Fed expanding balance sheet again. Will the result mirror 2020/21?

The Fed introduced the Bank Term Funding Program (BTFP) last weekend to stem deposit outflows from smaller banks. Program details are available on the Fed’s BTFP website.

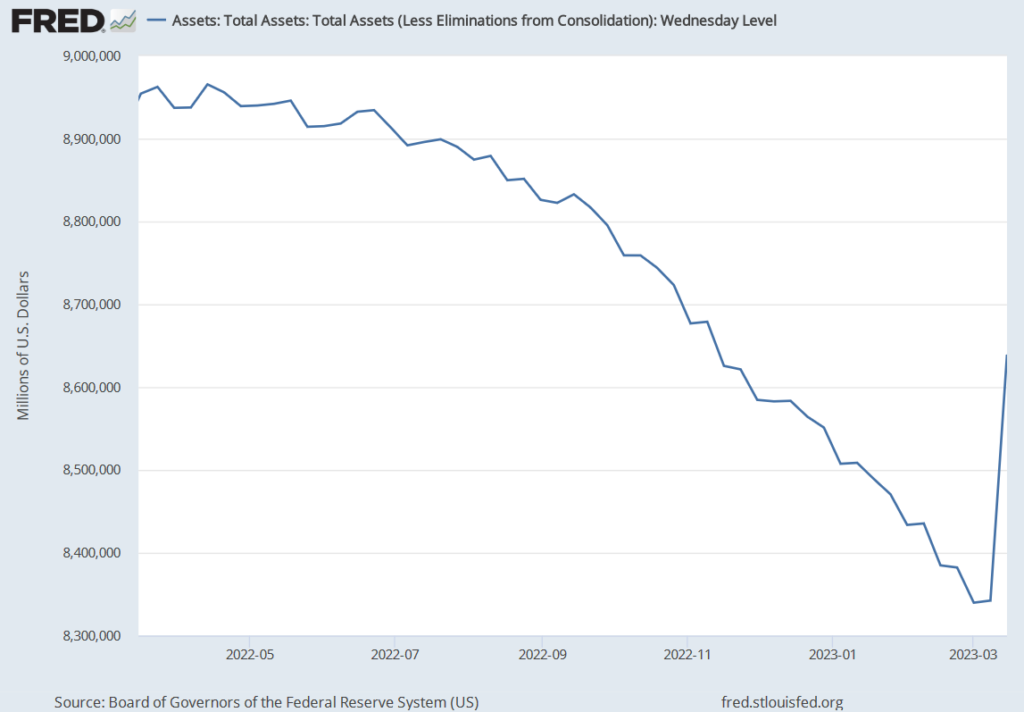

Fed expanded balance sheet substantially last week

In one week, the Fed unwound four months of QT (quantitative tightening), as this chart shows.

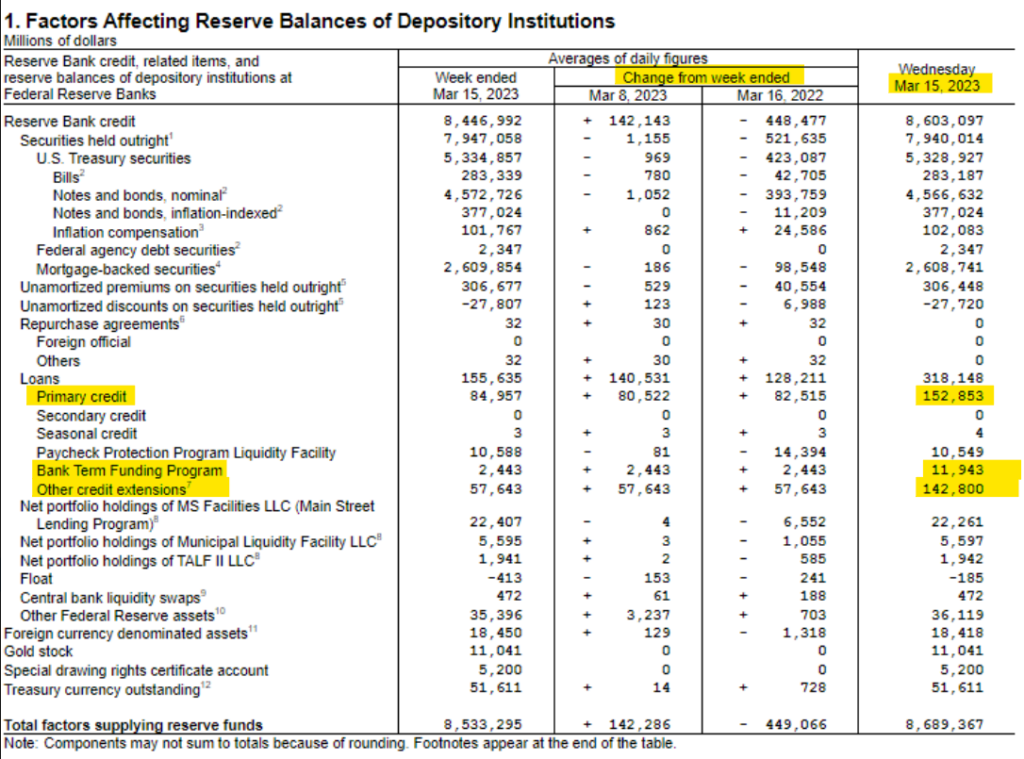

The balance sheet growth came via the discount window and other loans, not the Bank Term Funding Program (BTFP). We anticipate that the discount window lines will be converted/moved to the BTFP.

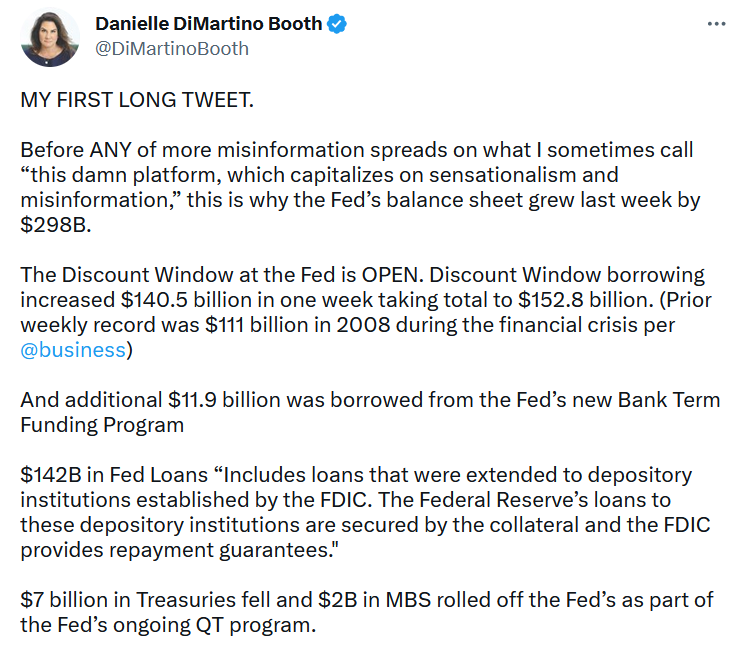

Source: Michael Derby @Reuters

Former Fed advisor’s breaks down the Fed balance sheet expansion in this tweet.

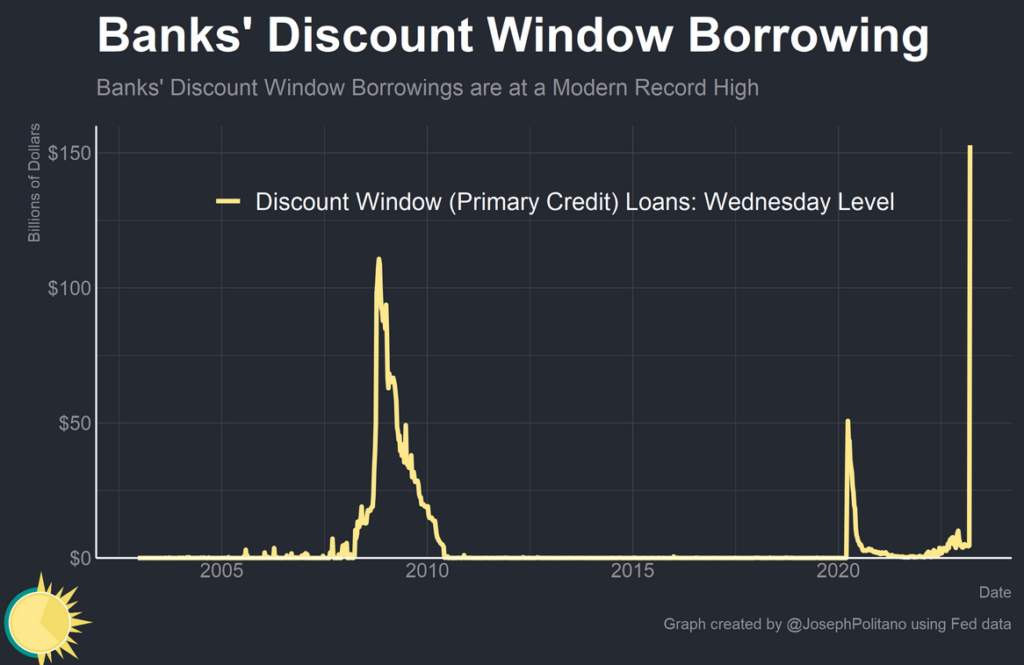

The chart below puts the current discount window borrowing in historical context. Keep in mind that the loans might be converted to BTFP lending later.

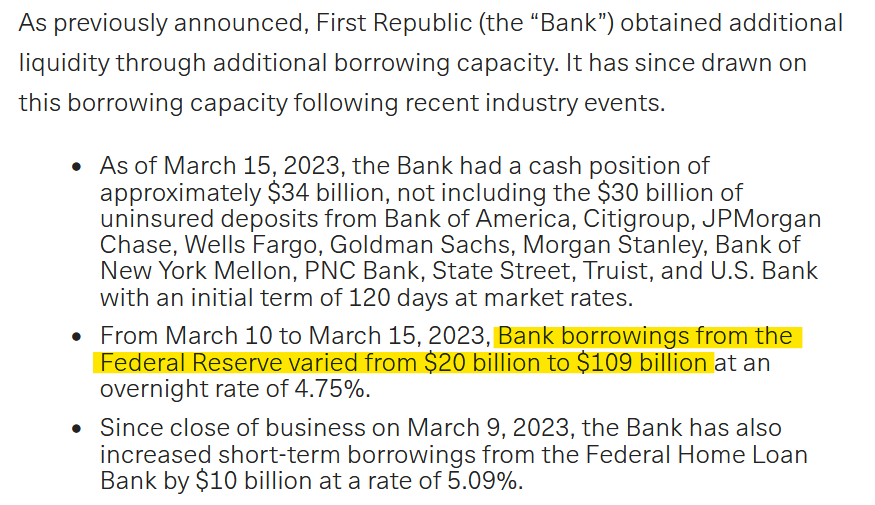

We know from First Republic Bank that they had already borrowed from the Fed before the BFTP lifeline was in place. Even after the BFTP was established, First Republic has to seek additional deposits from large banks to stave off liquidity pressure. This remain an area to watch for continued bank liquidity pressure.

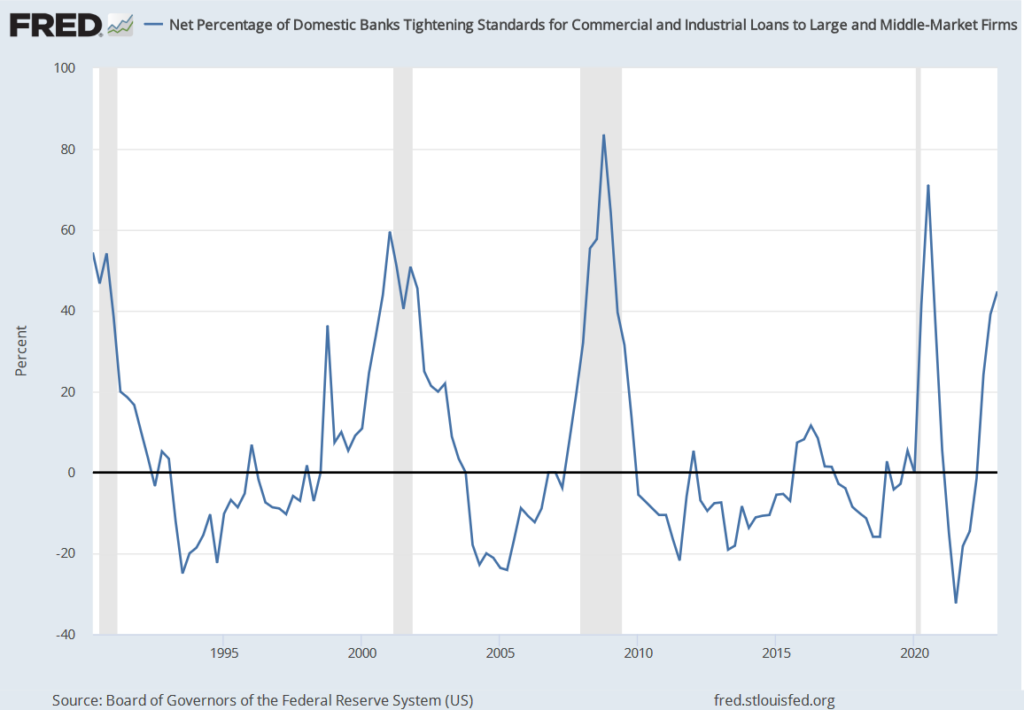

Bank credit and economic growth are tightly correlated

The chart of the Fed’s Senior Loan Office survey shows tighter lending standards for some time now, and it illustrates how tighter standards often precede recessions. The bank failures of the last week are highly likely to further crimp bank lending. It makes common sense that banks are unlikely to seek to increase lending as deposits flee.

Kicking the “moral hazard can” down the road

The US had a set of bank insurance rules, and those were quickly made irrelevant by multiple bank failures. The benefits of blanket insurance for the three failed banks will accrue to large depositors like companies, CEOs and millionaires that didn’t monitor the banks’ health. All US depositors will foot the bill for the special assessment to cover losses, if you assume banks pass on higher costs. However, in a highly indebted and financialized economy, it would have been suicidal to allow bank runs to linger. Having to expanding insurance coverage is a feature of this system.

Another feature of the US system is lobbying, and the saving “small business” and “jobs” were excellent points to use. Yes, the bank failures would have put thousands out of work. This ycombinator petion is an example of the bailout pitch.

SVB’s entire behavior can be ascribed to moral hazard (or next level ineptitude) and the same can be said of a tech companies that kept large deposits in a single bank. Operating companies should have swept excess cash into a money market fund for better protection and higher yield. Yes, there were SVB specific conditions that required start-up firms to keep all their cash with the bank, but what was Roku’s CFO thinking?

Expanding deposit insurance will increase future costs

We will discover with time if banks’ duration risk management stays poor with the BTFP providing an easy out. The program claims to have a one year life, but government backstops rarely end as planned. The system adapts to that backstop, which then makes it risky to remove the temporary program. In addition, expanding insurance coverage is unlikely to make depositors more discerning over the long term.

We will leave you with this line from the WSJ Streetwise column: “Too big to fail is in the process of being extended to a whole new set of banks”. Perhaps it is this increased future risk that gold and bitcoin are sniffing out currently. We’ll have more to say on this last point.

Important Disclosures

| This is not an offer or solicitation for the purchase or sale of any security or asset. Nothing in this post should be considered investment advice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning its accuracy. The views expressed are those of RockDen Advisors LLC and are subject to change at any time based on market and other conditions. Past performance may not be indicative of future results. At the time of publication, RockDen and/or its affiliates may hold positions in the instruments mentioned in this newsletter and may stand to realize gains in the event that the prices of the instruments change in the direction of RockDen’s positions. The newsletter expresses the opinions of RockDen. Unless otherwise indicated, RockDen has no business relationship with any instrument mentioned in the newsletter. Following publication, RockDen may transact in any instrument, and may be long, short or neutral at any time. RockDen has obtained all information contained herein from sources believed to be accurate and reliable. RockDen makes no representation, express or implied, as to the accuracy, timeliness or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and RockDen does not undertake to update or supplement its newsletter or any of the information contained therein. |